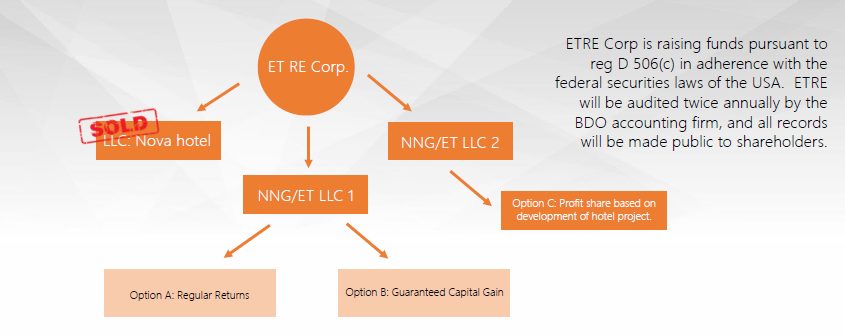

New Nordic Group and Emerging Trends RE Corp have “teamed up” to offer a range of unregulated investments (structured as redeemable convertible preference shares):

- Option A Guaranteed Regular Returns – The Secondary Income Investment: 7% “rental guarantee” paid monthly (quarterly for investments under $10,000, under 3.5 million thai baht [about £80,000], or “foreign payments”) for a term of 15 years

- Option B Guaranteed Capital Gain – The Long Term Income Investment:

- Option 1: 5% simple interest rolled up and paid out after 3 years (equivalent to 4.8%pa compound interest)

- Option 2: 7% simple interest rolled up and paid out after 5 years (6.2%pa compound interest)

- Option 3: 10% simple interest rolled up and paid out after 10 years (7.1%pa compound interest)

- Option 4: 12% simple interest rolled up and paid out after 15 years (7.1% compound interest)

- Option C: Capital Gain based on Profit Share: The Short Term Investment – preference shares in a company (NNG/ET LLC 2) developing a hotel project in Pratamnak Hill, Thailand.

All three options are structured as preference shares, issued by two companies owned by Emerging Trends RE Corp:

- NNG/ET LLC 1, which is the issuer of the preference shares under Options A and B

- and NNG/ET LLC 2, which is the issuer of the preference shares under Option C.

Unlike options A and B, returns from option C are variable and presumably depend on the price the development can be sold for on completion of construction. We have seen two brochures (one for all three options, one covering Option C only) which provide different projections for Option C. The first describes the term as “Approximately 2 years from construction commencement. Anticipated to begin July 2018” and says “anticipated project profits to be at 30%-60% (based on construction price, re-sale value and Hotel Brand long term operational forecasts)”. (“Hotel Brand” appears to be placeholder text.)

The second brochure states “Estimated term: 2-4 years” and “Estimated return: 42%”.

Details on the exit route for the Option C investment in the literature are somewhat vague. The second brochure says “We are developing a hotel project in Pratamnak Hill together with one of the world’s biggest hotel chains” – presumably, in order to return investors’ capital, the hotel chain in question is to pay NNG/ET LLC 2 on completion. However, the identity of this buyer is not clear. On page 16 of the second brochure, under “Operations” the page is blank except for the text “Will add details of hotel brand”.

Who are New Nordic Group?

No information is provided on New Nordic’s website as to who controls the business. A number of “country managers” and other members of middle management are shown, but no Chief Executive Officer / Managing Director / Chairperson is named, or any other information or who the directors or owners of the company are.

There are a number of “New Nordic” companies registered in various countries, including the UK. I was not able to establish who the ultimate owners or controllers of New Nordic Group are.

New Nordic has been in business since 2009.

Who are Emerging Trends RE Corp?

Emerging Trends RE Corporation was incorporated in the State of Delaware, USA on 26 May 2017.

According to Emerging Trends RE’s website, the Chief Executive Officer is David Jules Simpson, a former Trainee Adviser at Co-operative Insurance (now Royal London). According to the FCA Register David Simpson left Royal London in 2005. Prior to returning to the world of finance, Simpson ran lovepattayathailand.com, a website providing news and classifieds for the Thai resort city of Pattaya.

The other directors are Senior Executive Bob Pritchard, a marketing consultant and author of books including “Kick Ass Business and Marketing Secrets”, and Head of Design & Technology Tommy Wiberg.

The company describes itself as “a modern day alternative to a high street bank”. As the company offers only capital-at-risk investments, the company is clearly not an alternative to a high street bank offering regulated deposits.

How safe are New Nordic / Emerging Trends RE’s investments?

These investments are unregulated preference shares and if the issuer defaults you risk losing up to 100% of your money.

The investments are described as “redeemable convertible preference shares”. The purpose of raising money via preference shares under all three options is to allow New Nordic Group to develop residential and commercial property.

Under options A and B, if New Nordic Group fails to make sufficient profits from its property developments, or for any other reason Grove Developments has insufficient money to pay the promised coupons, and redeem the preference shares at the promised date, there is a risk that they may default on payments of interest and capital to investors.

Under option C, if New Nordic Group is for any reason unable to complete and sell the hotel development, the company is wound up, and there are insufficient funds in NNG/ET LLP 2 to compensate preference shareholders, there is again a risk that preference shareholders’ money may be lost.

Investors’ money is secured on property and cash owned by the LLPs (NNG/ET LLP 1 in the case of Options A and B, and and NNG/ET LLP 2 in the case of option C).

Before relying on this security, it is essential that investors undertake professional due diligence on NNH/ET LLP 1 and/or 2 to ensure that in the event of a default, the assets owned by the company would raise enough money to compensate investors, as well as any other debtors.

Investors should not assume that because the loans are asset-backed, they are guaranteed to get at least some of their money back through sale of the collateral if the company defaults. If the companies have insufficient assets to compensate all investors after meeting liabities to the insolvency administrator (who always stands first in the queue) and any other creditors who rank above the preference shareholders, they can still potentially lose up to 100% of their money.

The literature states “All investment options offered by ET in conjunction with NNG are fully secured by property or cash meaning that these are the safest types of investment available.” This is a highly misleading statement. As discussed above, preference shares secured on the assets of the company have potential for up to 100% loss if the assets of the company are insufficient to pay preference shareholders, after paying the insolvency administrator and any higher-ranking creditors.

Conventionally speaking, the safest type of investment available is a deposit account protected by a depositor compensation scheme, which carries virtually zero default risk. A portfolio of stocks and shares diversified across thousands of individual securities is riskier than a deposit account, but carries virtually no risk of permanent and total loss, and is therefore lower risk than an individual preference shares (secured on assets or not).

Are New Nordic / Emerging Trends RE’s investments “regulated”?

The first brochure describes the investments as “fully regulated and protected by US Law”. However, the second brochure states that “ETRE Corp is raising funds pursuant to reg D 506(c) in adherence with the federal securities laws of the USA”. Emerging Trends RE Corp also states that the firm relies on Regulation D 506.

Reg D 506(c) allows investments to be exempt from the stringent registration requirements of US securities law, providing that the investment is only sold to accredited investors – investors with more than $200,000 annual income or $1 million in assets excluding their house. Firms relying on Regulation D 506(c) must take reasonable steps to ensure investors qualify as accredited “which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like.” (SEC.gov)

As the entire point of Regulation D 506(c) is to exempt certain securities offerings from SEC regulation, an investment relying on Regulation D 506(c) is for all practical purposes unregulated. They are not required to file with the SEC beyond a very short “Form D” notice.

A search for “New Nordic” and “Emerging Trends” on the SEC’s EDGAR database for their Form D notices returned no results at time of writing.

Should I invest with New Nordic Group / Emerging Trends RE Corp?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Although all three options are structured as individual preference shares, Options A and B are essentially loans, with a fixed coupon and the promise to return capital at the end of a fixed term. Option C is an equity investment, with the term depending on the progress of construction, and the return depending on how much the property is sold for at the end of construction; although NNG gives a projected return, no promises are made as to how much the return will be.

Both individual loans and individual equity securities are only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

As discussed above, New Nordic / Emerging Trends RE’s investments are higher risk than a diversified portfolio of mainstream stockmarket funds, despite their claims to offer the “safest types of investment available”.

These investments are described as asset-backed. Before relying on the security backing the investments, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees and any other borrowers are paid.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

- Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for the “safest types of investment available”, you should not invest in unregulated products with a risk of 100% capital loss.