The Care Home Group Ltd (part of Carlauren Group Ltd, previously Corporate Land Solutions Ltd) is offering unregulated investment in care home rooms.

Investors pay up to £69,950 to purchase the leaseholds of individual care rooms, at what is described as a 30% discount to market price, in dilapidated care properties which The Care Home Group plans to renovate. They then receive returns in one of three ways:

- Option 1: Investor as Landlord: Investors receive variable rental income, initially based on the market rate of the room, with a 3% “developer’s cash back” on completion of refurbishment. They then receive rental income when the room is occupied (with no income if the room is vacant).

- Option 2: Managed Service: Investors receive a fixed income of 10% each year, paid monthly, regardless of whether the room is occupied or not. 2.25% developer’s cash back is paid on completion of refurbishment (3% minus a one-off 25% charged by the managing agent).

- Option 3: Self Occupancy: The investor may choose to use the room for themselves or a family member.

Investors may swap between the three options at six months’ notice. If they change their option within the first year, a penalty fee of 25% of the annual rent is payable. An investor switching from option 1 or 2 to option 3 must pay the difference between the discounted purchase price and the full market price.

The Care Home Group undertakes that investors will be able to sell their investment via a buy-back option and receive 110% of their investment back in years 5-6, 115% in years 7-8, 120% in year 9 and 125% in year 10. It says in the FAQ section that this buyback option applies “when [the room] is permanently vacated”.

Who are The Care Home Group?

The operator of the care homes is described as Carlauren Care Limited (formerly Caring Communities Limited), while the developer is Carlauren Devleopments Limited.

Carlauren Care Limited is 100% owned by Carlauren Lifestyle Resorts Limited (formerly The Care Home Group Limited), which is in turn 100% owned by Carlauren Group Limited (formerly Corporate Land Solutions Ltd). Carlauren Group Limited is 99% owned by Sean Murray with the remaining 1% held by Nicola Mason.

Carlauren Developments Limited is 100% owned by Sean Murray.

Carlauren Group Limited had net assets of minus £142k according to its last accounts (December 2016), which were filed under the small companies regime and therefore exempt from auditing. Carlauren Developments has yet to file accounts as an active company.

How safe is the investment?

These are unregulated investments in individual units of a care home and you risk losing up to 100% of your money if the yield dries up and a buyer cannot be found for your units.

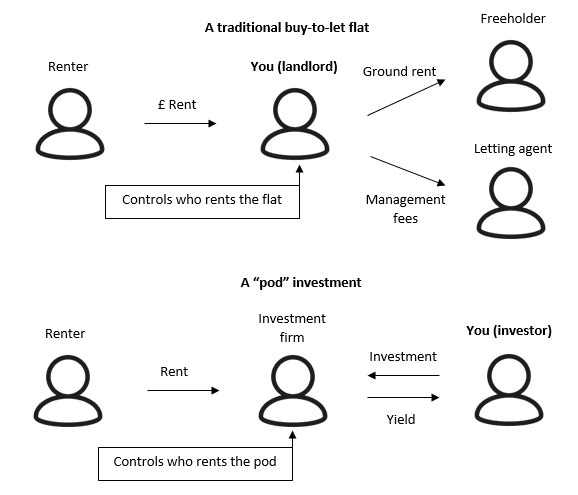

This investment follows the “pod” model, where an investment firm divides its property into units (or “pods”), and then sells those units to investors in return for a fixed yield (in the case of option 2), or variable payments based on income from the investor’s individual unit (option 1).

The difference between a “buy-to-let” flat and a pod investment is that with buy-to-let, the investor has full control over who they rent their property to. A buy-to-let investor may employ letting agents to do the job for them, but they can hire and fire the letting agent at will. They may also have to pay ground rent to the freeholder of a block of flats, but the freeholder does not have the right to stop the leaseholder letting out their flat.

In the case of this investment, The Care Home Group retains control over who uses the care home’s rooms. Individual investors have no ability to fire The Care Home Group if they fail to keep their room occupied.

This means that investors must satisfy themselves that The Care Home Group will not fill up its own rooms before it fills up those belonging to investors receiving rental income. At a minimum, The Care Home Group will hold rooms (and the income thereof) which it has not yet sold to investors, or from investors who exercised their buyback option.

The promise to pay investors a fixed return of 10% per annum is only as good as the company backing it. If The Care Home Group fails to make sufficient income from its care homes to pay a fixed return of 10% per annum, it may default on payments of income to investors.

If The Care Home Group becomes unable to meet the payments of 10% per annum, this would leave investors relying on The Care Home Group keeping their room occupied and generating sufficient rental income from it.

Likewise, the promise to buy back investors’ units at up to 125% of the purchase price (once the room is permanently vacated) is also dependent on The Care Home Group having sufficient liquid funds to do so. If The Care Home Group is unable or unwilling to buy back the units, investors will be relying on selling to third parties on the secondary market if they want to get their money out.

In the extreme, investors in pod-type investments have been known to lose all their money (e.g. Store First) when:

- the investment firm stopped paying the promised fixed returns and refused to buy the units back

- it became clear that there was no realistic prospect of the investor’s individual pod being occupied by a renter and generating any yield

- and as the units generated no yield, this made them effectively worthless on the secondary market.

We are not implying that the same will happen to The Care Home Group’s units, but this example illustrates the risk that is inherent in investing in individual units within a larger investment property. Investors should not assume that as a care hoom room is a physical property, it must have some value. The value of a room in a care home to which someone else controls access depends entirely on what yield can be expected.

“30% discount” and market price

The Care Home Group states in its literature that investors can purchase care rooms for a 30% discount on their full market price.

There is virtually no recognised secondary market for buying and selling individual rooms in a care home. The “market price” is therefore likely to be based on the opinion of a valuer hired by The Care Group, rather than actual purchases and sales.

Investors should therefore undertake their own due diligence on the purchase price to ensure it is fair. Just as when buying a house, you would hire your own valuer and not just accept the valuation of the estate agent (who works for the seller).

It is highly unlikely that anyone would buy a second-hand care room in one of The Care Home Group’s properties, when they could get one direct from The Care Home Group with a 30% discount and the promise of a guaranteed 10% yield.

This means that for as long as The Care Home Group is making this offer, investors wishing to exit their investment will be reliant on The Care Home Group having sufficient funds to exercise the buyback option.

Should I invest in The Care Home Group?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated investment, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of 10% per annum should be considered very high risk. As an individual security with a risk of total and permanent loss, The Care Home Group’s care units are higher risk than a mainstream stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the Care Home Group became unable to pay fixed returns or to buy the units back, the care room generated no rental income, there was no secondary market for my care room and I lost up to 100% of my money?

- Do I have a sufficiently large and well-diversified portfolio that the loss of 100% of my investment in The Care Home Group would not damage me financially?

If you are looking for a “secure” investment, you should not invest in unregulated investments with a risk of 100% capital loss.

Good advice! Hope people took it…