Just ISA is offering five year bonds paying interest of 8% per year.

Money invested in Just ISA (a trading name of Just ISA Bond Co 1 Limited) will be loaned to an operating company in Jersey, which in turn will finance litigation funding, specifically in the area of professional negligence.

Just ISA is not to be confused with Just Group plc (a much larger FTSE-listed provider of annuities and other retirement products).

Who is Just?

Just ISA Bond Co 1 Limited is 100% owned by Creative Litigation Funding Solutions Limited, which is in turn 100% owned by Robert Rutter. Both companies were incorporated in early 2018 and are yet to file accounts with Companies House due to their young age.

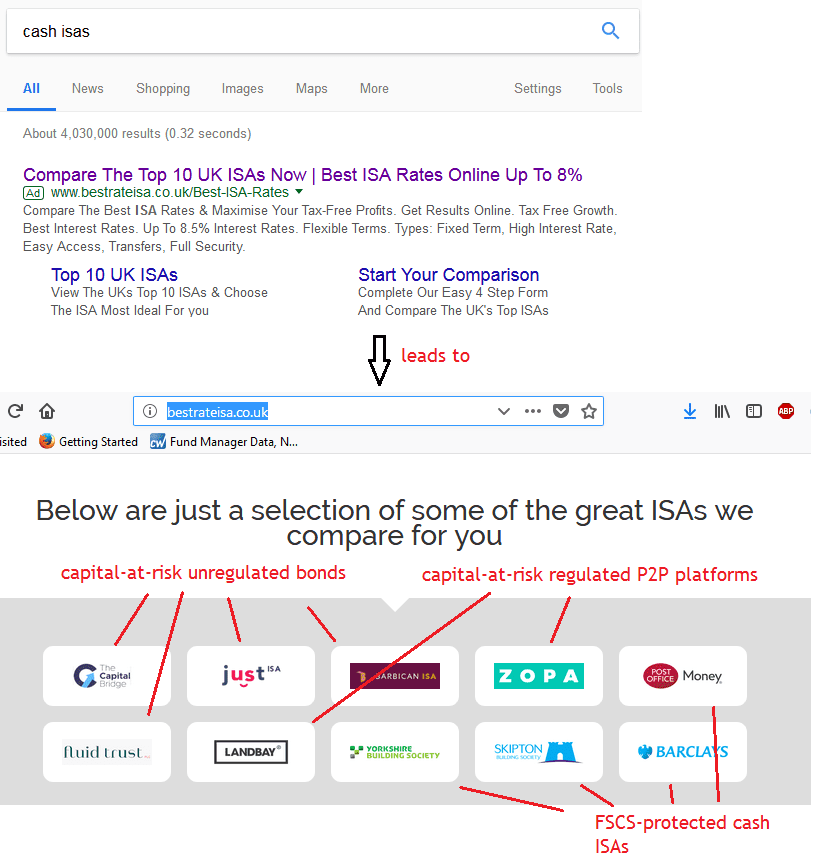

Investors can access Just ISA’s bond via an IFISA wrapper provided by Northern Provident Investments Limited. Northern Provident Investments provides ISA wrappers for a number of IFISA bond investments under its umbrella; according to the FCA Register, its current trading names include Northern Provident Investments Limited, Barbican ISA, Capital Bridge ISA, Choices ISA, Fluid ISA, Just ISA and Prime ISA.

While Northern Provident Investments Limited is regulated by the Financial Conduct Authority as an ISA manager, Just ISA Bond Co 1 Limited and its associated companies are not regulated by the FCA.

How safe is the investment?

Just ISA, along with other capital-at-risk IFISA bonds under the Northern Provident Financial umbrella, is currently being promoted by unregulated introducers to UK investors searching on Google for cash ISAs.

These adverts are taken out by introducers independent of Just ISA and Just ISA cannot be held responsible for misleading promotions such as this one.

It is very important that investors understand that these investments are corporate loans and if Just ISA defaults you risk losing up to 100% of your money. They are not like regulated cash ISAs (e.g. those offered by the Post Office, Skipton and Barclays) which are covered by the FSCS up to £85,000 if the authorised deposit-taker defaults, and are virtually free of investment risk if you remain within the £85,000 limit.

The purpose of Just ISA’s bonds is to allow its sister company in Jersey to fund litigation in professional negligience cases.

If Just ISA fails to make sufficient returns from their litigation funding, or for any other reason Just ISA runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

After The Event Insurance

Just ISA aims to mitigate risk by only funding cases that it believes are likely to succeed and have a strong possibility of being settled within 24 months. It will also only fund cases where After The Event insurance can be obtained, which means that if the case fails in court, Just ISA should receive its investment back from the insurer.

Investors should not assume that because Just ISA’s cases are covered by After The Event insurance in place, there is no risk of losing money.

By putting ATE insurance in place, Just ISA aims to mitigate the risk of losing money where its cases fail in court. However, merely not losing money is not sufficient for this investment to succeed. Just ISA needs to make enough money from its lending business to meet its set-up costs, salaries and other overheads, and then pay investors 8% each year, in order to be able to pay investors’ interest and capital on time.

There is also a risk that the insurer may not pay out (although Just aims to insure across AA, A+ and A- rated insurers).

Just ISA’s literature boasts of a “case win rate of 90%”. Given that Just ISA and its associated companies have only been running for about half a year at time of writing, and court cases are not short affairs (Just ISA says elsewhere that it targets cases that are likely to be settled within 24 months), this statistic seems somewhat meaningless. Even if Just ISA has managed to already conclude some of its cases in such a short space of time, it seems too premature to publicise their success rates as representative.

Should I invest in Just ISA?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of 8% a year should be considered high risk. As an individual, illiquid security with a risk of total and permanent loss, The Capital Bridge’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

The investment may be suitable for high net worth and sophisticated investors who will already be well aware of all of the above risks, are looking to invest a small part of their assets in corporate lending, and feel that the return on offer (8% over five years) is sufficient for the risks involved in lending to a small unlisted company.

If you are looking for a “capital protected” investment, you should not invest in corporate loans with a risk of 100% loss.

How do you get in touch????? Got a phone number???

There’s a contact link at the top of every page.