And the Security did not have any mechanism to enable the Security Trustee to prevent SEB from disposing of secured property which was a fundamental flaw. It meant the Security Trustee could not prevent SEB from paying most of the money raised for investing in solar projects in the UK to its parent in Australia – who then went bust.

What would be interesting to me would be to learn of example paragraphs in loan documentation that would have secured against this particular risk.

The short answer is that I don’t believe there is any way you can secure against this particular risk on an individual loan note basis, and certainly not by inserting paragraphs in the Information Memorandum.

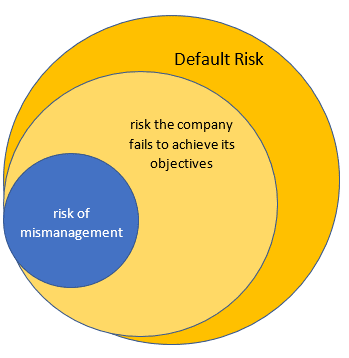

When you hand over money to a company to be invested on your behalf, there is always a risk that they won’t do with it what they said they would.

Once your money is in the hands of a company, the default position is that the directors can do with it as they see fit. What is there to stop them misusing it? There is no regulator or bondholder-appointed governess looking over their shoulder. The answer is mainly the threat of legal action against the company or the directors themselves if misuse results in a loss.

However, legal action is expensive and difficult, and the possibility of an investor recovering their money from the company or its directors may be slim. And, of course, legal action can only take place after the fact.

Let us say that back in 2013 the Secured Energy Bonds documentation included the line “Investor funds will be invested solely for the purposes described in this Information Memorandum and will not be invested in the parent company or any other third party”. SEB then goes ahead and transfers money to the Australian parent anyway. What can investors or the Security Trustee do about it? Not a lot. They probably wouldn’t have even found out until SEB went bust.

It is important to bear in mind that the risk of the company not doing what they said they would is only a small subset of a much larger risk – default risk. A company can do exactly what it said it would with investors’ money, and still fail to make sufficient returns to pay bondholders, because it does it badly, or has sheer bad luck. Any loan note is subject to default risk.

If you’re worried about the blue circle, you might be missing the bigger picture.

The vast majority of investors secure their investments against default risk by diversifying across hundreds or thousands of companies listed on regulated exchanges worldwide. The risk of any one company on a regulated exchange going bust is small, and diversification ensures that even though a small number inevitably will go bust during the course of a long-term investment, it will only have a negligible effect on the investor’s portfolio.

Some of those busts will be due to mismanagement, some incompetence, some bad luck and often a combination of all three. The investor doesn’t have any reason to care why a company went bust if it only means an imperceptible blip in their portfolio of less than 1%.

If I have a diversified basket of investments, I’m not going to be up all night worrying about any blue circle in particular.

The vast majority of investors should not be put in a position where they have to worry about such things.

Have a question about investments? Worried about risk? Problems in the bedroom? Send your questions to the usual address, unless they’re about the last one.

According to a filing with Companies House, MJS Capital plc has changed its name to Colarb Capital plc.

Over the past year, a number of investors have complained via comments on this blog and other online forums about MJS Capital failing to repay their bonds when they fell due. A common theme is MJS Capital negotiating a payment plan for the repayment of matured investments, which MJS then also fails to meet.

In June 2018 MJS / Colarb disclosed in its September 2017 accounts that it had experienced banking issues, with banks either freezing its accounts or refusing to allow it to open new ones.

Non-executive director Lord Razzall CBE resigned from the company in March 2018, saying in his resignation letter that he hoped his removal from the board would resolve MJS Capital’s banking problems.

MJS also disclosed in their accounts that they used a company set up by a former director (Martin Westney), imaginatively named MJS Cap Limited, in another attempt at resolving its banking issues.

From the ongoing complaints by investors, it does not appear that either measure has achieved much.

In June and July 2018 there was a brief flurry of promotional activity by MJS on Medium and Twitter but the company has since appeared to fall silent.

MJS / Colarb Capital managing director and owner Shaun Prince previously incorporated a company under the name Colarb Holdings Limited in December 2017. Exactly what Colarb is supposed to mean is unclear, although “arb” may relate to MJS’ underlying investment in arbitrage, while “col” could refer to “collective” or “collateral”.

At time of writing MJS Capital’s previous website (mjs.capital) is down. A search on Google for an official Colarb-branded website produced no results.

Legend Lane is offering various unregulated investments which include:

Legend Lane FX Trading Platform – investment in forex paying fixed interest of 24% for a one year investment

Legend Lane Gold Product – investment in gold paying fixed interest of 24% for a one year investment

Legend Lane 1314 – investment in property paying fixed interest of 9% per year

Silver Sun Living – investment into Senior Housing paying 6-8% returns

Investment into a “Film Production Fund” paying 10% per year for 2 years (described on the website as “release summer 2018”)

Investment into Loco Energy Drinks paying 9% per year for 2 years

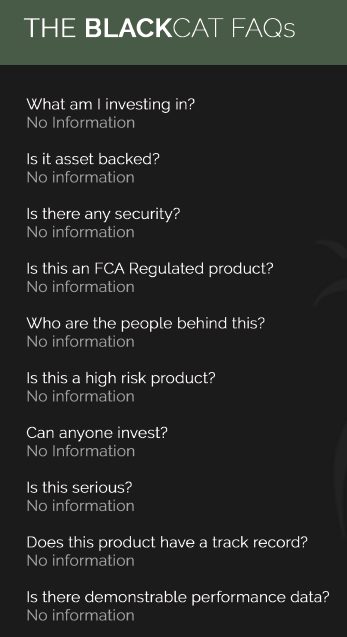

Investment into “Black Cat”, an “anonymous, daring, adventurous, prestigious, defining, liberating, dynamic, mystical” investment into something undisclosed paying 30% over one year

Who are Legend Lane?

Legend Lane has two UK registered companies: Legend Lane Limited and Legend Lane Group Limited (previously known as Legend Lane (Glasgow) Limited and still referred to by its old name on the website).

Legend Lane is jointly owned by its directors, Gregory (Greg) Paul Heywood and Christopher (Chris) Glendinning Miller.

At the time of its last filings, both Legend Lane Group Limited and Legend Lane Limited were shell companies holding only £100 and £80 share capital respectively.

Both Greg Heywood and Chris Miller were previously directors of The Step Properties Holdings plc, which ceased operating in 2008 and was dissolved in 2010. A related company owned by Heywood, Heywood Property Investments, collapsed as a consequence owing £3.6 million to HSBC Bank. Only £1.27 million was recovered from the company.

Another former The Step director, Leigh Heywood, is currently CEO (though non-shareholder) of Aston Darby, an unregulated investment into airport car parks.

How safe is the investment?

Legend Lane’s investments are all unregulated capital-at-risk investments and if Legend Lane defaults you risk losing up to 100% of your money.

Most of Legend Lane’s investments (forex, gold, property) consist of fixed interest investments. If Legend Lane fails to make sufficient returns from its underlying activities, there is a risk that it may run out of money to pay investors’ interest and capital.

Legend Lane also offers investment in senior care suites with promises of a fixed return and an “assured buyback” after 15 years. For more details of how these investments work in theory, and the risks involved, see my general guide to investing on hotel rooms (this involves senior living suites rather than hotel rooms, but the investment structure is the same).

For the sake of brevity, I will not analyse every single one of Legend Lane’s offered investments in detail. There are however a number of red flags which immediately jump out.

1)Lack of FCA authorisation

A number of Legend Lane’s activities require authorisation from the Financial Conduct Authority, such as its claim to run an FX platform and a film production fund.

Legend Lane’s website also constitutes a clear financial promotion which induces investors to invest in its products.

Carrying out regulated activities and issuing financial promotions in the UK without FCA authorisation is a criminal offence.

2) Misleading claims

Legend Lane refers on its website to making £500,000 in charitable contributions “since we began in 2012″. There is no evidence that Legend Lane existed prior to 2016, when its Companies House registration began.

Legend Lane literature refers to the company “formerly trading via two consultancy companies that have amalgamated into Legend Lane Limited”. No details of these companies are provided and Legend Lane Limited’s last accounts (May 2018) show it to be a shell company holding £80 in assets.

Legend Lane did not exist prior to 2016 and there is no evidence that any older trading company has been merged into it whose history Legend Lane can lay claim to.

Legend Lane also displays an Investors In People logo on its website. Investors In People has confirmed that Legend Lane is not accredited by them.

3) Nonsensical investments

Legend Lane’s forex bond (paying 24% in one year) claims that only 10% of investors’ money will be put at risk. If Legend Lane loses 10%, it will give investors the option to withdraw with their remaining 90%.

6. How is my capital protected?

The Legend lane FX Platform offers capital protection ensuring only 10% of the invested amount is ever at risk. Only 5% – 10% of client’s monies are traded at any one time. The remaining balance of 90% remains secured with the liquidity provider. All trading will cease in the event that the client account loses 10%. In this scenario the client will be given the option to exit the investment and receive 90% of their capital back within 14 days.

Why exactly investors would want to give Legend Lane 90% of their money so they can just sit on it I have no idea. If I want to put only 10% of my capital at risk, then I am quite capable of investing 10% and keeping 90% in my own bank account, where I will get more interest, more tax-efficiently than Legend Lane can achieve as a business.

Moreover, in order to generate returns of 24% per annum on the total investment while only trading 10% of investors’ money, Legend Lane effectively has to generate annualised returns of 240% per annum from forex trading, plus costs, on the amount put at risk. (At current cash interest rates, the 90% not at risk can be safely assumed to earn almost nothing.)

If Legend Lane is capable of consistently generating 240% annualised returns, why bother soliciting investment over the Internet when they could keep their method to themselves and be billionaires within a few years?

While it is possible to generate very high returns from forex trading in the short term, in the long term forex trading is a zero sum game, and Legend Lane’s claim to be able to generate 240% per year returns from forex in order to generate 24% per year for investors while only putting 10% of their money at risk is a screaming red flag.

As this is an unregulated investment, investors will have virtually no protection if Legend Lane fails to keep 90% in cash as promised and defaults on its promise to return at least 90% to investors if its forex trading fails.

Its gold bond paying 24% per year makes little more sense. Gold is a highly volatile commodity. Similar to forex, while it is possible to make short-term profits in the gold market, nowhere in Legend Lane’s investment literature does it adequately explain how they expect to make a predictable 24% return in one year from buying and selling gold.

And we will finish with my favourite investment of all, the Black Cat investment paying 30% in one year.

Shut up and take my money!

How does Legend Lane intend to generate this 30%? No idea. According to the literature, “no information is all the information you need”. The Black Cat investment literature contains a load of specious waffle, irrelevant quotes, and a series of FAQs which are all answered “No information”.

Essentially, Legend Lane’s Black Cat is a modern updating of a famous investment from the South Sea bubble of the 18th century, which advertised “a company for carrying out an undertaking of great advantage, but nobody to know what it is“.

Next morning, at nine o’clock, this great man opened an office in Cornhill. Crowds of people beset his door, and when he shut up at three o’clock, he found that no less than one thousand shares had been subscribed for, and the deposits paid. He was thus, in five hours, the winner of 2,000 pounds. He was philosopher enough to be contented with his venture, and set off the same evening for the Continent. He was never heard of again.

– Charles Mackay, Extraordinary Popular Delusions and the Madness of Crowds, 1841

Between Legend Lane’s illegal financial promotions and regulated activity, implausible returns and nonsensical investments, and its false claim to have Investors in People accreditation, it is clear that investors should not hand over their money unless they are content with the risk that its directors will do exactly the same.

Should I invest with Legend Lane?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Notwithstanding the regulatory issues raised above, there is nothing illegal in running an unregulated investment by itself. Even if Legend Lane defaults on its various bonds and investors lose all their money, that, by itself, will not mean it has done anything wrong.

Any investment in a single company is high risk. Any investment offering returns of 24-30% per annum has an extremely high chance of loss.

Do not proceed unless you are prepared for total losses.

Blueprint Industrial Engineering PLC is offering four year bonds (maturing 30 June 2022) paying interest of 6% per year.

Blueprint Industrial Engineering PLC is a holding company for one wholly-owned subsidiary, B.I.E. Sweden AB, which in turn wholly owns AMAB Arvika Montage AB.

Money raised from investors is to be used to meet Blueprint’s overdue payments to the sellers of Arvika Montage (see below), and more generally to enable the company to acquire further Nordic engineering businesses.

Who is Blueprint Industrial Engineering?

Blueprint Industrial Engineering is headed by group CEO Jan Lindholm, who also holds a 25-50% shareholding according to Companies House.

Blueprint Industrial Engineering has been loss-making since the 2015/2016 accounting period, with its most recent results (April 2018) showing a £586,000 net loss in 2017/18, a slight improvement from a £590,000 net loss in 2016/17.

As at the April 2018 accounting date, the company’s liabilities exceeded its assets by £2.7 million (£6.3 million total liabilities vs. £3.6 million total assets).

According to the April 2018 accounts, the company is dependent on raising further money from investors (e.g. via these bonds) in order to complete its acquisition of Arvika Montage AB, currently its only subsidiary. Blueprint has already failed to meet the original payment schedule and has negotiated a payment plan to complete the acquisition by December 2018.

However, the directors are confident that they will raise the funds needed and thereby continue to run the business as a going concern.

Going concern

At 30 April 2018 the Group had a net working capital deficit of £2.1 million which included deferred consideration of £1.3 million due to the vendors of Arvika Montage AB. Since the end of the year the Group has received over £0.5 million from the issue of bonds and the directors are confident that bonds will continue to be issued to provide sufficient funds to meet the Group’s obligation to pay the deferred consideration and to finance working capital. However, there is no guarantee that the Group will have access to future debt finance or the ability to generate positive cash flows and this represents a material uncertainty which casts significant doubt upon the Group’s continued ability to operate as a going concern, such that it may be unable to realise its assets and discharge its liabilities in the normal course of business. The financial statements have been prepared on a going concern basis which assumes that the Group will be able to realise its assets and settle its obligations in the normal course of business.

How safe is the investment?

These investments are corporate loans and if Blueprint defaults you risk losing up to 100% of your money.

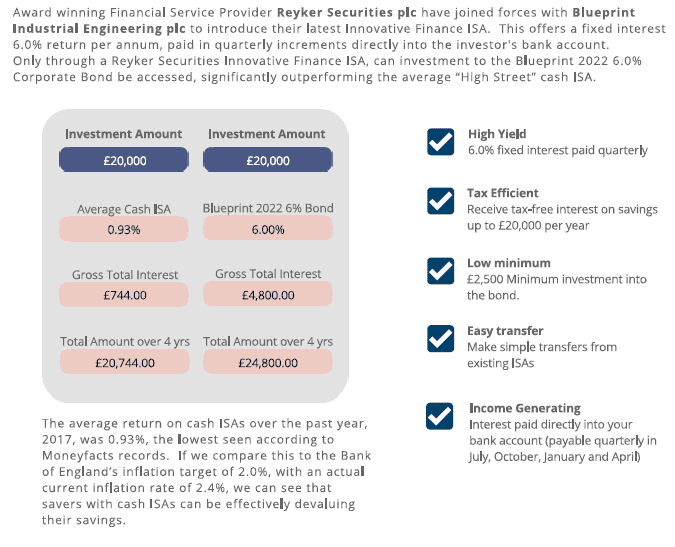

A brochure prepared and issued by Blueprint and approved by City One Securities (a firm authorised by the FCA, but permitted to conduct corporate finance business only) compares the 6% offered by Blueprint bonds with the 0.93% offered by an average cash ISA.

Source: Blueprint Brochure

This is a totally misleading and irrelevant comparison, as cash ISAs have no material risk of loss as they are covered by the Financial Services Compensation Scheme, which Blueprint’s bonds are not.

With recent rulings from the Ombudsman emphasising that FCA-authorised firms who approve marketing material for unregulated investments can be held responsible for those promotions, it is disappointing that some are not taking their responsibilities seriously.

The fact that this marketing material predates the recent Ombudsman rulings against Independent Portfolio Managers is not an excuse – the financial promotion rules have been in place for years and comparing a cash ISA with a capital-at-risk corporate bond has never been anything other than misleading.

If Blueprint fails to make sufficient returns from its engineering investments, or for any other reason Blueprint runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Should I invest in Blueprint Industrial Engineering plc?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

As an individual security with a risk of total and permanent loss, Blueprint’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment in Blueprint would not damage me financially?

If you are looking for cash ISAs, you should not invest in capital-at-risk corporate bonds with a risk of 100% loss.

The investment may be suitable for high net worth and sophisticated investors who will already be well aware of all of the above risks, are looking to invest a small part of their assets in corporate lending, and feel that the return on offer (6%) is sufficient for the risks involved in lending to a small company listed in Cyprus.

The directors of Munio Capital, which in 2016 offered five-year unregulated bonds paying 9.8% per annum, have applied to strike the company off the register.

Munio is six months overdue with its accounts and recently survived a compulsory strike-off in July 2018. That strike-off attempt was launched by Companies House due to the company’s failure to file a confirmation statement; this latest strike-off has been requested by the directors themselves, specifically director and joint-owner Gary Williamson.

Munio Capital’s website is down and its phone number goes straight to an answering machine.

The stated aim of the company was to provide liquidity to a payday lender in the US. Investors have alleged that Munio invested investors’ money in Privilege Wealth, which is in administration.

How much was invested in Munio Capital is not known as the company has failed to file accounts since its bond raise.

If no objection is received to the striking off, the company will be dissolved and all Munio Capital’s assets, if any, will become property of the UK Government (though creditors could apply to have this reversed). UK law requires that all Munio’s creditors must be notified of the striking off application.

The strike-off application suggests the directors believe Munio Capital – and by extension its bonds – to be worthless.

How do I get my money back from Munio Capital?

Munio Capital was promoted to at least some investors by regulated financial advisors. If you were advised to invest by an FCA-regulated adviser, you may be able to recover your money by making a formal complaint that the bonds (which were suitable only for sophisticated and high net worth investors investing a small part of their assets) were unsuitable.

If the adviser refuses to provide compensation, the complaint can be taken to the Financial Ombudsman, which can order compensation of up to £150,000 per person. If the adviser is unable to pay, you would be covered by the Financial Services Compensation Scheme up to £50,000 per person.

Investors should avoid Claims Management Companies (CMCs) as they are unnecessary (the FOS and FSCS process is slow but straightforward), often have a lower success rate than direct complaints, and charge eye-watering fees (often 30% of monies recovered).

If you invested in Munio Capital, you should be on your guard against anyone contacting you and telling you that they can recover your money. It is highly likely that you will be targeted by fraud recovery fraud. If anyone asks you to pay “legal fees” or “liquidation fees” to release your money it is almost certainly a scam.

Shenton International Bonds plc launched in March 2016 and issued two-year and four-year bonds paying 9% per year and 10% per year respectively. Shenton provides bridging finance to property developers, principally in Brazil.

Last month it belatedly filed its December 2017 accounts, three months overdue, a delay which led to Companies House briefly applying to strike the company off the register (strike-off filed 28 August and suspended on 1 September).

£2.38 million was raised from the 2016 2-year bonds, with a further £1.264 million raised from the 2016 4-year bonds.

In April 2018 (just as the 2016 2-year bonds were coming up for repayment), Shenton launched a further unregulated bond issue, this time paying a higher rate of 10% over two years (12% to Shenton’s previous investors).

Investors holding just over 70% of the capital which was due for repayment in March 2018 rolled their investments into the new 2-year minibonds.

[page 2]

Future Developments

On 5 April 2018 the Company launched a third two year Mini Bond to coincide with the repayment date of 29 April 2018 for the 2-year Mini Bond launched on 27 January 2016. Investment amounting to £675,000 was repaid and £1,704,500 was invested in the New Mini Bond.

This means that Shenton successfully repaid the capital falling due in early 2018, and the next big test of its business will be when both the 2016 4-year bonds and the 2018 2-year bonds fall due in 2020.

As at the balance sheet date of 31 December 2017, the company had £177,000 in net assets, comprising £3.9 million of assets (predominantly £3.4 million loans to developers, plus some cash and trade debtors) minus £3.75m of liabilities (predominantly £3.6 million in investor loans).

The loans to developers are valued on the effective interest rate basis, with no impairment provision against bad debts. This is on the basis that Shenton’s loans to developers are asset-backed (i.e. in theory, if the borrower defaulted, Shenton would be able to recover its money from the security).

Shenton will include an impairment provision if either a loan is underperforming (i.e. interest is not being paid), or the value of Shenton’s loan exceeds the value of the property it is secured on (note 14b). As the December 2017 accounts do not include any impairment provision (note 9), presumably this did not apply to any of Shenton’s loans.

The next accounts are due to be filed in June 2019.

Update 3.10.19: At the time of this review Northbridge was known as The Capital Bridge. It has since renamed to First Northbridge Limited and changed its web address to northbridgeinvest.co.uk.

Northbridge continues to offer IFISA bonds paying 9% per year. The original review follows.

The Capital Bridge is offering three year bonds paying interest of 9% per year.

Money invested in The Capital Bridge (a trading name of Capital Bridge BondCo 1 Limited) will be loaned to Capital Bridging Finance Solutions Limited, which in turn will lend the money to property developers.

Who is The Capital Bridge?

Capital Bridge BondCo 1 Limited is 100% owned by Capital Bridging Finance Solutions Limited, which is in turn 100% owned by Paul Dalton.

Capital Bridging Finance Solutions was incorporated in January 2012. According to its last accounts (January 2017) it had net assets of £179k. The accounts were exempt from auditing due to Capital Bridging Finance Solutions’ small size.

Its subsidiary Capital Bridge BondCo 1 Limited (which is the company actually issuing the bonds) is more recent, incorporated in July 2018. Due to its young age it is yet to file accounts.

Capital Bridge BondCo 1’s other director is Mark Roberts.

Investors can access The Capital Bridge’s bond via an IFISA wrapper provided by Northern Provident Investments Limited. Northern Provident Investments provides ISA wrappers for a number of IFISA bond investments under its umbrella; according to the FCA Register, its current trading names include Northern Provident Investments Limited, Barbican ISA, Capital Bridge ISA, Choices ISA, Fluid ISA, Just ISA and Prime ISA.

How safe is the investment?

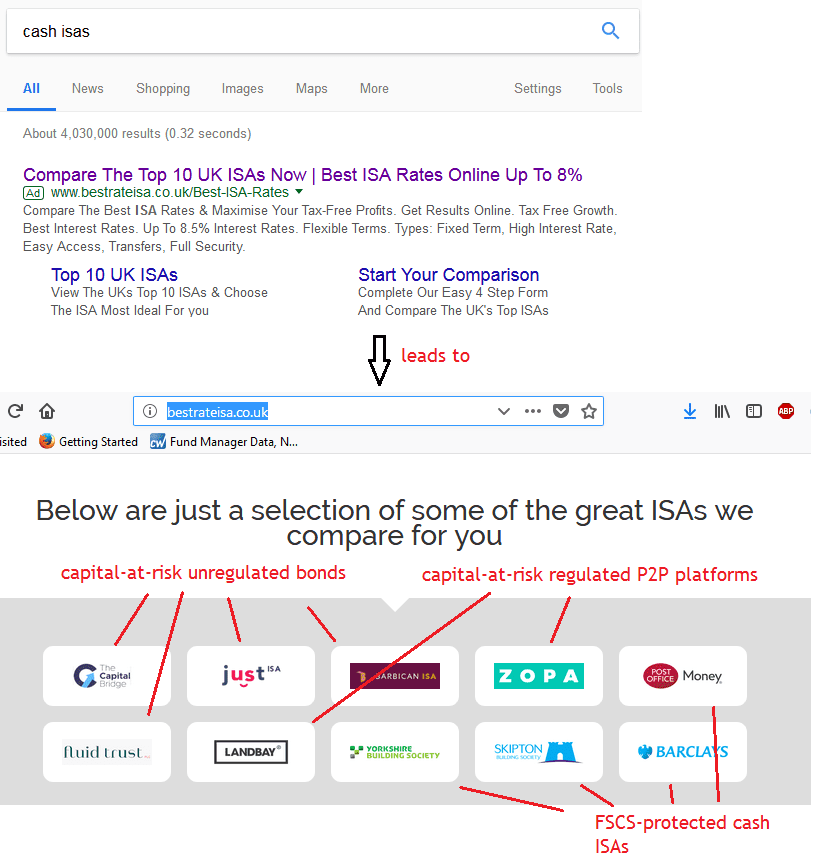

Capital Bridge, along with other capital-at-risk IFISA bonds under the Northern Provident Financial umbrella, is currently being promoted by unregulated introducers to UK investors searching on Google for cash ISAs.

Top: Google search result for “cash ISAs”. Bottom: Screenshot of the top sponsored result, bestrateisa.co.uk. No risk warnings are included anywhere on this website.

These adverts are taken out by introducers independent of The Capital Bridge and the Capital Bridge cannot be held responsible for misleading promotions such as this one.

It is very important that investors understand that these investments are corporate loans and if The Capital Bridge defaults you risk losing up to 100% of your money. Unlike regulated cash ISAs (e.g. those offered by the Post Office, Skipton and Barclays) which are covered by the FSCS up to £85,000 if the authorised deposit-taker defaults.

The purpose of the bonds is to allow The Capital Bridge to lend money to Capital Bridging Finance Solutions, which will in turn use the money to lend to property developers.

If the Capital Bridge companies fail to make sufficient returns from their property loans, or for any other reason The Capital Bridge runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Asset backed investment

The Capital Bridge aims to mitigate risk by lending money to property companies and ensuring that the underlying loans are secured on the property being developed.

Investors should not assume that because the underlying loans are secured on property, there is no risk of losing money. It is still possible to lose money on secured loans if, for example, the property cannot be sold for enough money to repay the borrower in full or the borrower cannot enforce the security over the asset.

By investing in secured loans, The Capital Bridge aims to reduce the risk of losing money in its underlying business (property development lending). However, merely not losing money is not sufficient for this investment to succeed. The Capital Bridge needs to make enough money from its lending business to meet its set-up costs, salaries and other overheads, and then pay investors 9% each year, in order to be able to pay investors’ interest and capital on time.

Note that investors are investing in Capital Bridge BondCo 1, which in turn lends money to Capital Bridging Finance Solutions. It is Capital Bridging Finance Solutions which holds the security over properties in respect of its loans to developers, not Capital Bridge BondCo 1 itself.

This is a crucial distinction because if Capital Bridging Financial Solutions is unable to meet its obligations to Capital Bridge BondCo 1, the only security that investors will have is the assets of Capital Bridge BondCo 1 itself. In turn the only security that Capital Bridge BondCo 1 has is the assets of Capital Bridging Financial Solutions – some of which may be secured loans.

Long story short, any corporate loan note inherently has a risk of loss, even if it is secured and asset-backed. This is why they pay higher rates than FSCS-protected deposits.

Should I invest in The Capital Bridge ISA?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of 9% a year should be considered high risk. As an individual, illiquid security with a risk of total and permanent loss, The Capital Bridge’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

The investment may be suitable for high net worth and sophisticated investors who will already be well aware of all of the above risks, are looking to invest a small part of their assets in corporate lending, and feel that the return on offer (9% over three years) is sufficient for the risks involved in lending to a small unlisted company.

Betteridge’s Law of Headlines: Any headline that ends in a question mark can be answered with the word “No”.

As I noted earlier this week, in July and August Independent Portfolio Managers had what is bound to be the first of many Financial Ombudsman complaints awarded against it, for its role in approving the literature for the collapsed Secured Energy Bond investment.

It looks highly likely that similar awards against it will follow for its role in Providence Bonds.

In June 2018, the Financial Conduct Authority cancelled IPM’s permissions over an unpaid regulatory fee of £1,660 and 23 pence. The chance of IPM being able to meet the slew of claims against it, which could run into the millions, appears minimal.

At time of writing, the two test case investors have accepted the ruling, so IPM has now been ordered to pay. IPM is no longer an FCA-regulated company. If it fails to pay, investors have to go to the Financial Services Compensation Scheme. More delays, but eventually I should see my money back.

I hate to be ‘that guy’ towards investors who have suffered enough already, but if the FSCS compensates Secured Energy investors for their unregulated, ultra high risk investment, it will effectively turn the entire UK financial system on its head and mean that any unregulated capital-at-risk investment can be rendered risk-free for any investment below £50,000 (£100,000 for couples).

(This point appears to have been missed by the Guardian and other outlets which have covered this story; understandably, they have focused on the long emotional struggle of investors and not the detail of financial services regulation.)

How to make an unregulated investment risk-free (if the FSCS pays out over IPM)

I launch Company X offering unregulated bonds offering returns of 8% per year for investing in whatever (let’s say crypto mining).

Simultaneously my friend sets up Company Y and applies for FCA authorisation to conduct whatever regulated activity is the easiest to get FCA authorisation for.

Once FCA registration is secured, my friend rubber-stamps my investment literature with the words “approved for the purposes of Section 21 of the FSMA by Company Y, which is authorised and regulated by etc etc”.

Both of us ensure we are careless enough that there is a clear error in the investment literature – such as overegging “security features” to make the bonds appear less risky than they are (as with IPM).

A few years later Company X goes bust. Investors complain to the Financial Ombudsman that the literature was misleading and Company Y should have spotted it.

The Ombudsman upholds the complaints and awards redress against Company Y. Company Y goes bust.

Investors claim to the Financial Services Compensation Scheme and get their money back (up to £50,000 per person).

There are, of course, already a total of three ways in which you can transfer liability for an investment scheme to the FSCS.

Set up an authorised deposit-taker and issue retail deposits or cash ISAs (which are FSCS-protected). Problem: getting authorised as a deposit-taker involves extremely stringent regulation and capital adequacy requirements. Difficulty: Extreme.

Set up a SIPP (Self Invested Personal Pension) firm and have investors invest in Company X via Company Y SIPPs, while failing to do adequate due diligence. (Note: rulings from the Ombudsman have been contradictory, but the recent direction of travel seems to be that the SIPP provider can be held liable.) Problem: getting authorisation to run a SIPP provider also involves stringent regulation and capital adequacy. Difficulty: Extreme.

Set up a financial adviser and have it advise investors to invest in Company X. Problem: Getting authorisation to give advice requires passing a series of exams and obtaining professional indemnity insurance. Difficulty: Much lower than setting up a bank or a SIPP provider, but still high enough to prove a deterrent.

The crucial difference between these three types of firm and Independent Portfolio Managers is that they all involve a specific type of FCA permission that is quite hard to get.

However, any FCA authorised firm, regardless of what it is authorised to do, is permitted by the Financial Services And Markets Act to authorise financial promotions. There is no specific FCA permission for “authorising financial promotions”. If you’ve got any other FCA authorisation, you get that one chucked in as a freebie.

In turn, following the recent precedent, any FCA-authorised firm can be ordered by the Ombudsman to pay for authorising promotions that they shouldn’t have.

Lowering the bar

There are FCA permissions that are really not that difficult to acquire – for example, insurance mediation (which has been a favourite of firms illegally holding themselves out as financial advisers when they don’t have the specific authorisation) or debt counselling.

You still have to wait six months to a year for the FCA to consider your application, but if you are in the unregulated investment bond business, a waiting period of six months to a year is not much of a problem.

According to the FCA’s website, “positive indicators” which would make authorisation more likely include:

reading information on our website

making enquiries of the contact centre

seeking legal/compliance advice

being able to clearly articulate their regulatory obligations

This sounds not dissimilar to the basic requirements for passing a job interview.

You get the point. Getting FCA authorisation is not difficult as long as you pick the right kind of authorisation. The authorisation of firms like Independent Portfolio Managers rather proves as much.

This means that allowing any FCA-authorised firm to effectively transfer the liability of an unregulated investment to the Financial Services Compensation Scheme, by way of authorising a misleading or flawed promotion on its behalf which investors could then complain about, would represent an astonishing lowering of the bar to obtain FSCS coverage.

It is such a low bar that I can’t see why you wouldn’t do it, and make your investment far more attractive by lowering the risk at no cost to yourself. Hence my rather clickbaity headline.

Protected claims

But is it even likely? By my reading of the Financial Services Compensation Scheme rules, the answer is no.

As I have banged on aboutbefore, the liability of the Financial Services Compensation Scheme is strictly defined by the definition of a “protected claim”. All FSCS claims involve FCA-authorised firms but not all claims against FCA-authorised firms are covered by the FSCS. If I run an FCA-authorised company and commission my friend’s company to build me a £1 million solid gold swimming pool on the roof, and go bust without paying, my friend’s company has a claim against an FCA-authorised firm but not against the FSCS.

A complaint about a regulated adviser’s bad advice is a protected claim. So is a deposit-taker or a SIPP provider going bust. A claim arising from a complaint over the authorisation of investment literature is, as far as I can see, not included anywhere in the list of protected claims.

At this point of course, this is just my interpretation. It will be the Financial Services Compensation Scheme that decides when/if Independent Portfolio Managers eventually goes to the wall.

The regulated financial industry has long chafed against the cost of FSCS levies, on the grounds that the good guys have to pay for the bad. Making it much easier to get unregulated investments covered by the FSCS would inevitably lead to higher FSCS levies, and increase costs for the vast majority of consumers who use mainstream regulated financial services (who always pay in the end when investors in unregulated investments are bailed out).

If the FSCS does pay out over Secured Energy Bonds and Providence Bonds – even where no SIPPs were involved and no financial advice was involved – we can expect a huge backlash from the regulated world.

More likely is that the FSCS will reject the claims, and the Secured Energy and Providence investors will finally be allowed to come to terms with the loss of their investments.

Krono Partners launched in 2013 and offered unregulated seven-year bonds paying interest of 8% per year, plus variable payments of 20% of the company’s assets. Krono Partners aimed to generate returns by investing in distressed real estate in the United States and Europe.

In 2017, with the distressed asset bonds approaching their five year anniversary, Krono Partners issued a further series of bonds, this time offering 10% per year over five years. This time investors’ money was to be used to invest in bridging finance for small and medium enterprises.

According to an investor on Moneysavingexpert.com, Krono Partners stopped paying interest in the beginning of 2018, still two years shy of the repayment date of its 2013 bonds.

A Companies House filing yesterday reveals that Krono Partners has gone into administration.

More to follow when the administrator’s report has been made available.

How do I get my money back from Krono Partners?

If you invested in Krono Partners, you should be on your guard against anyone contacting you and telling you that they can recover your money. It is highly likely that you will be targeted by fraud recovery fraud. If anyone asks you to pay “legal fees” or “liquidation fees” to release your money it is almost certainly a scam. The administrators will not collect any fees directly from investors; the administrators always stand first in the queue and will collect their fees before any money is paid to investors (if any).

Whether there is any prospect of recovery from Krono Partners itself is in the hands of the administrators.

Independent Portfolio Managers played a crucial role in the collapse of two unregulated bonds, Secured Energy Bonds and Providence Bonds.

Independent Portfolio Managers was an FCA-regulated company that issued financial promotions on behalf of Secured Energy and Providence. Without those FCA-regulated promotions, Secured Energy and Providence could not have been promoted to UK investors.

After those two bonds collapsed with total losses, investors in both Secured Energy and Providence made formal complaints to first Independent Portfolio Managers and then the Financial Ombudsman.

Just over a year and a quarter since it accepted the cases, The Financial Ombudsman has now began issuing rulings.

In three separate cases published in June and August, all three of them regarding IPM’s production of literature for Secured Energy Bonds, it has deemed that IPM was at fault for approving the promotion, and that it is responsible for investors’ losses, as they would not have invested if IPM’s promotion had not misled them into thinking that Secured Energy Bonds were “relatively safe”.

IPM must therefore repay their full investment (minus any interest received before Secured Energy’s collapse), plus interest.

Given that the FOS initially refused to even consider the cases on the basis that Secured Energy Bond investors were not customers of Independent Portfolio Managers, the FOS decisions represent an impressive victory for Secured Energy investors.

It seems nearly inevitable that the Ombudsman will also rule in favour of Providence Bond investors, assuming they also have complaints making their way through the system, as the circumstances were very similar.

However, I suspect that this may well turn out to be a Pyrrhic victory. I have previously noted that Independent Portfolio Managers’ last accounts (March 2016) state that it has net assets of £128k. Losses in Secured Energy and Providence total £15 million. Despite exercising its right to a six-month extension, Independent Portfolio Managers is now three months overdue with its accounts and there is an active proposal to strike off the company as a consequence.

Whether Independent Portfolio Managers has actually paid any of the Ombudsman’s awards against it is unknown.

The full ruling in the latest decision DRN0142726 is worth reading for anyone involved in the unregulated bond sector. In particular, the Ombudsman castigates IPM for portraying the “security features” of the bond, including the appointment of a Security Trustee and the fact that the bond was backed by SEB’s parent, CBD Energy in Australia, as if it made the bond less risky.

The invitation document did say there was a risk the security given to the Security Trustee and the guarantee given by CBD Energy might not be sufficient to repay the bondholders.

But the Invitation Document also gave the clear impression to potential investors that the Secured Energy Bond was a relatively safe investment in which investors had the protection of additional security measures making the investment less risky than other mini-bonds.

However CBD Energy was not, according to the information in the Invitation Document, in a strong enough financial position to be able to repay bondholders on demand if called to do so under the guarantee it gave.

And the Security did not have any mechanism to enable the Security Trustee to prevent SEB from disposing of secured property which was a fundamental flaw. It meant the Security Trustee could not prevent SEB from paying most of the money raised for investing in solar projects in the UK to its parent in Australia – who then went bust.

[…] The Security system was not fit for purpose. The SEB bonds were no more secure, or less risky, than other non-secured mini-bonds.

Other issuers and promoters of unregulated bonds who heavily feature “security features” such as asset-backing and Security Trustees in their literature should take note.