Christianson Property Capital was founded in 2014 and offers unregulated bonds paying 10% per annum for ten years. (Or previously offered; it is unclear whether the company is accepting new investment.)

If Christianson continues to fail to file accounts, and nobody makes a valid objection to the striking off, all the assets of Christianson Property Capital Limited will be forfeited to the UK Government. This would include its subsidiaries, Victory House Group Limited, Victory House 1 Limited, Victory House 2 Limited and Victory House 3 Limited.

This naturally will be of serious concern to any investors in Christianson Property Capital. Assuming Christianson was accepting investment in its bonds from 2014, investors have at least 6 years of their investment left to run.

The good news is that Companies House will often suspend a strike-off if creditors object, which they can do by emailing [email protected] with supporting evidence. However, if Christianson continues to fail to file accounts, the strike-off process will likely be resumed at a later date. Christianson’s directors also risk a criminal prosecution.

Update 18/04/2018: Christianson Property Capital Limited finally filed accounts on 17 April, and the strike-off has been suspended.

Apex Algorithms offers investment in sports betting arbitrage. Previously, according to a February 2018 Daily Mail article, the company was offering unregulated bonds paying 16% per annum. However, recent promotions from the company make no mention of a 16% per annum return and instead offer a “profit share” arrangement.

Profits are shared between Apex Algorithms and the investor according to how much they invest, as follows:

Foundation £2,500-£5,000 40% / 60%

Silver £5,000-£25,000 50% / 50%

Gold £25,000-£50,000 55% / 45%

Platinum £50,000+ 60% / 40% plus profits paid quarterly

Who are Apex Algorithms?

No details are provided on the Apex Algorithms website as to who is behind the business.

Nathan Burgoyne, Apex Algorithms owner and director

Apex Algorithms is a trading name of Apex Incorporated, although the registered company name is not mentioned anywhere on the website. Apex Incorporated is wholly owned by Nathan Burgoyne, the sole director.

Apex Incorporated was incorporated in July 2013, struck off the register in November 2014, and re-admitted to the register in April 2015. Its latest accounts (July 2016) show net assets of £641 and current assets of just under £19,000.

How safe is Apex Algorithms?

This is an unregulated investment and investors risk losing 100% of their money.

Apex Algorithms use investors’ money to invest in sports betting arbitrage. In betting arbitrage, investors look for two opposing bets on different exchanges that are priced in such a way that if they place a bet on both exchanges, they are guaranteed to make money. For example, if one bookie offers 11/10 on Anthony Joshua to beat Joseph Parker, and another bookie simultaneously offers 11/10 on Parker to win, you can place £100 with both bookies knowing that regardless of which way it goes, one bookie will pay you £210 and the other will take your money, leaving you with a £10 (5%) net profit.

In reality it would be extremely rare for two bookies to screw up quite so obviously. In reality, within minutes both bookies would adjust their odds to, say, 10/11 on both fighters – which means if you bet £100 on both you will lose £9. Also, it should be noted that if Joshua and Parker draw the match, you lose all your money.

Betting arbitrage, while a perfectly legitimate way to earn money, typically produces low returns in exchange for a great deal of time and effort to identify a suitable pair of bets.

Should Apex Algorithms fail to generate sufficient returns from betting arbitrage to meet its costs, or if it gets its bets wrong, there is a risk that investors may lose all their money.

Investors should also note that in a “profit share” arrangement, any interest due to investors who invested in Apex’s 16% per annum bonds must be paid first, before any profit is shared out with “profit share” investors.

Whether investors are invested in Apex via bonds promising interest of 16% per annum, or via a profit share investment, there is a risk of permanent and total loss should Apex Algorithms fail to make sufficient returns via arbitrage to cover interest payments and other costs.

Back testing / past performance?

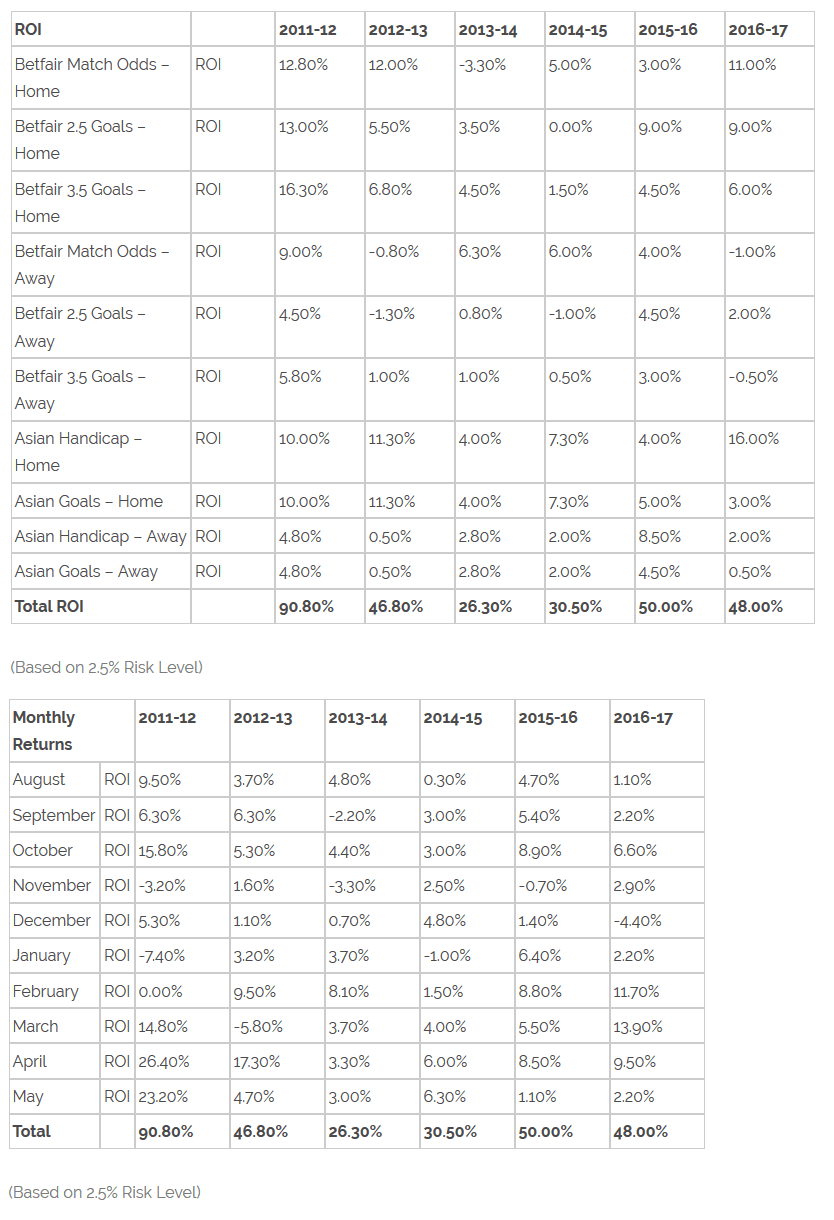

Apex Algorithms provide a table of “past performance” on its website and says this “reflects active trading as and on behalf of the Apex syndicate from 2014 to present day”, with results from 2011 reflecting the performance of syndicate members prior to forming the syndicate.

Confusingly, in a PDF brochure, the same table is referred to as “back testing”. The term “Back testing” refers to results that are not actual past performance, but results that an algorithm would have generated had it been applied in the past. “Back testing” and “past performance” are two completely different things – the former is theoretical performance, the latter is real performance.

Two tables are given; one shows the results broken down by ten types of bet, the other shows ten month-by-month returns.

(Why June and July are missing is not clear. The per-bet table shows only football bets, but Apex’s literature states that they invest in a variety of sports including tennis and American sports. Not all of these sports break off for the summer. Apex’s staff are entitled to a holiday the same as everyone else, but if the entire investment is suspended for two months each year, this should be disclosed.)

Both tables show a total return on investment at the bottom for each year, which, as you would expect, match each other. In each table, the figure in the “total” row is the sum of all the figures above (return per bet or return per month) – with a 0.1% difference in all but one year.

The problem is that in the first table, if Apex Algorithms divided investors’ money among the ten types of bets listed, the total return would be the weighted average, not the sum. If I have £100 and divide it equally between three bets returning 5%, 25% and -5%, I receive £108.30 and my return is 8.3%, not 25%.

The only way it could make sense for the returns per individual bet to generate the total listed is if Apex Algorithms invested all its investors’ money in “Betfair Match Odds – Home”, kept the 12.8% return in cash, reinvested the original stake in “Betfair 2.5 Goals – Home”, banked the 13% return, reinvested the original stake in “Betfair 3.5 Goals – Home”… and so on.

Quite apart from the illogic of Apex Algorithms investing sequentially in this way (the nature of arbitrage is that Apex needs to invest in whatever betting market is offering the opportunity to make risk-free returns), this would mean the table would have to at least show some similarity to the sequence shown in the month-to-month percentages. Not necessarily identical (it would make even less sense for Apex to spend a month investing in one type of bet and the next month investing in another type and so on) but if both tables show a series of sequential ROIs there should at least be some resemblance.

But the following table shows a completely different sequence of percentages. In 2011-12, for example, Apex Algorithms supposedly made a loss in two months even though all of its bets by category showed a profit.

Also note that if Apex Algorithms was reinvesting the profits from its successful bets, the annual total shown in the month-by-month table should be the product of the monthly ROIs plus one, not the sum. (109.8% * 106.3% * 115.8% * 96.8%… etc.) While Apex could conceivably bank profits in cash each month and only reinvest the original capital, why would it do so when it has a low-risk method of generating high returns?

I can only think of one explanation for why the returns in these tables do not correspond with each other or the correct method of calculating an overall annual ROI. What these tables actually show is two sets of made-up numbers which happen to add up to the same number at the bottom.

Should I invest with Apex Algorithms?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Apex Algorithms claim in their literature that this is a “Low risk investment” and their representatives claim “There will never be catastrophic loss like in the stock market.”

The reality is that investors risk up to 100% losses should Apex Algorithms fail to make sufficient returns from betting arbitrage to cover their costs – including the cost of their 16% per annum bonds.

As with any unregulated investment, it is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

There are also serious questions over Apex Algorithms’ supposed “backtesting / past performance” results.

A filing on Companies House reveals that Lord Timothy Razzall has stepped down as director of MJS Capital plc. MJS Capital plc offers unregulated bonds paying up to 9.85% per annum to fund investment in financial arbitrage.

Popularly known as “Lord Razzall of Dazzle”, Lord Razzall served as a director of MJS Capital from 19 May 2015 to 12 March 2018. He is described as non-executive Chairman in MJS Capital’s investment literature, and “responsible for scrutinising the performance of management in meeting agreed goals and objectives, in particular adherence to the investment policy and overseeing the correct and proper operation of the Security Fund”.

Lord Razzall remains a director of Barton Brown Limited, who wrote MJS Capital’s investment literature.

Under the heading and sub-heading “How the investment in the Bonds is protected”, MJS Capital’s literature states that the involvement of Barton Brown Limited and Lord Razzall in drafting the Information Memorandum means “Investment in the Bonds is directly protected” – in the sense that the involvement of Barton Brown Limited and Lord Razzall, along with their collective experience in corporate law, means investors can rely on the statements in the literature.

We reached out to Lord Razzall’s parliamentary office on Thursday for a comment on his reasons for leaving MJS Capital, but at time of writing have received no response.

Update 27 March 2018: By way of response, Lord Razzall has now provided us with a copy of his resignation letter to Shaun Prince, MJS Capital’s owner, which states:

The background to this is my concern about the effect I have as a politically exposed person on the company’s banking relationships.

This is a significant problem nowadays particularly for a company like MJS which is dependent on its banking relationships.

As you know I am happy to remain involved with the company as a consultant and advisor, but hope that my resignation as a Director will help with the banks.”

While Politically Exposed Persons are subject to a higher level of scrutiny when dealing with financial institutions, in itself it is difficult to see why having a PEP as director would cause problems for MJS Capital – particularly when you consider Lord Razzall was a non-executive chairman and did not exercise day-to-day control.

The FCA expects that a firm will not decline or close a business relationship with a person merely because that person meets the definition of a PEP (or of a family member or known close associate of a PEP). A firm may, after collecting appropriate information and completing its assessment, conclude the risks posed by a customer are higher than they can effectively mitigate; only in such cases will it be appropriate to decline or close that relationship. (FCA guidance FG17/6)

As Lord Razzall says, hopefully whatever problems MJS Capital is experiencing with its banking relationships will be resolved shortly.

Future Renewables Eco plc (FRE plc) offers 3 and 5 year unregulated bonds paying interest as follows:

3 year bonds:

£7,500 – £24,999 – 7%pa interest paid biannually or annually, or 6.999%pa if interest is deferred and paid out at the end of the term. (The literature states 7.5% interest for the deferred option, however a footnote states that this is simple interest. 7.5% simple interest paid after three years is equivalent to 6.999% Compound Annual Growth Rate.)

£25,000 – £49,999 – 8% interest paid biannually or annually, or 7.9% interest if deferred and paid out at the end of the term. (8.5% simple interest paid out after three years = 7.9% CAGR)

£50,000 + – 9% interest paid biannually or annually, or 8.7% interest if interest is deferred and paid out at the end of the term. (9.5% simple interest paid out after three years = 8.7% CAGR)

5 year bonds:

£7,500 – £24,999 – 7.5%pa interest paid biannually or annually, or 6.96%pa if interest is deferred and paid out at the end of the term. (8% simple interest paid out after five years = 6.96% CAGR)

£25,000 – £49,999 – 8.5% interest paid biannually or annually, or 7.7% interest if deferred and paid out at the end of the term. (9% simple interest paid out after three years = 7.7% CAGR)

£50,000 + – 9.5% interest paid biannually or annually, or 8.4% interest if interest is deferred and paid out at the end of the term. (10% simple interest paid out after three years = 8.4% CAGR)

The front page of the literature states “7-11%” returns but the highest headline rate of return, even on a simple interest basis, is the 10% paid to those who invest more than £50,000 in the 5 year option and roll up interest. I could find no mention of how investors can earn 11% from FRE bonds anywhere in the literature.

Furthermore, £50k+ investors in the 5 year deferred interest bond do not receive 10% returns. They receive 10% simple interest, but 10% simple interest paid out after five years (i.e. £75,000 on an investment of £50,000) is an annualised compound growth rate of 8.4%.

The use of compounded annual growth rate to represent the rate of return is universal in the finance industry. This is because those who elect for annual or biannual income can reinvest their interest payments, which those who elect for deferred income cannot.

The highest return available from FRE’s bonds is therefore 9.5%pa, the interest paid out to £50k+ investors in the 5 year bonds who elect for income paid out.

Why investors receive a lower rate of return for electing not to receive income is not clear. In most investments, investors who elect not to receive income receive a higher return to reflect the fact that they are exposed to more risk. For illustration only, if FRE defaults just before the end of the five year term and no money is recovered for investors, biannual income investors have at least received 42.75% of their money back (9 biannual payments x 9.5% / 2) whereas deferred investors lose all their money.

FRE is not the first issuer of unregulated bonds to apparently ignore how compound interest works when setting its bond coupons, but it is the most egregious example I have come across so far.

Given that FRE bonds should only be marketed to high-net-worth and sophisticated investors, I have to ask how many high-net-worth and sophisticated investors, and their professional advisers, are likely to overlook this point. A return to the drawing board may be necessary if FRE expects any sophisticated investors to opt for deferred income.

Who are FRE plc?

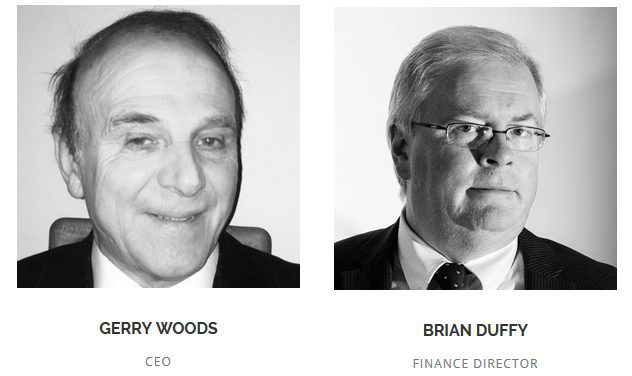

FRE’s website and the literature lists the directors as Gerry Woods (CEO) and Brian Duffy (Finance Director).

Future Renewables Eco plc was incorporated in May 2015, and is 100% owned by Future Renewables Eco Energy Ltd, which in turn has three shareholders: Jadenorth Properties Limited 45%, Bananas Consulting Ltd 45% and Anne Sellar 10%.

Jadenorth Properties is equally owned by Yvonne Duffy and Carolyn Paterson, presumably the wives of Bryan Duffy and Walter Paterson, who are listed by Companies House as having significant control. Bananas Consulting is wholly owned by Mark Eprile.

This means the ultimate controllers of Future Renewables Eco plc are as follows: Mark Eprile 45%, Bryan Duffy (via his wife) 22.5%, Walter Paterson (via his wife) 22.5% and Anne Sellar 10%. Mss. Duffy and Paterson are not registered as directors or mentioned anywhere in the literature, and it can safely be assumed that they do not exercise day-to-day control of the company and hold the shares for tax-efficiency reasons.

Gerry Woods and Brian Duffy were previously director and secretary respectively, and both shareholders, of Marlborough Residential Finance, a company which owned four adjacent properties in the Scottish countryside outside Perth. Marlborough Residential Finance defaulted on its debts in January 2017, owing £2.4 million to its secured creditor (Clipper Holdings who bought the debt two months previously from Allied Irish Bank). It is currently in administration.

How safe is the investment?

These investments are unregulated corporate loans and if FRE defaults you risk losing up to 100% of your money.

The purpose of the loan is to allow FRE to acquire wind turbine sites that benefit from government subsidy.

If FRE fails to receive sufficient money from the Government and other customers for its wind energy, or for any other reason FRE has insufficient money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Asset-backed security

Following the acquisition of a wind turbine site, FRE “will grant a fixed charge over the Project Site and any assets subsequently built on or affixed to the Project Site” to a Security Trustee who will hold these assets in trust for the bondholders.

Investors should not assume that because their loans are secured on these assets, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed loans have been known to lose 100% of their money (e.g. Providence Bonds and Secured Energy Bonds) when it turned out that the collateral was insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in FRE plc, only illustrating the risk that is inherent in unregulated corporate loan notes even when they are asset-backed.

If investors wish to rely on this security, it is essential that they undertake professional due diligence to ensure that in the event of a default, these securities are valuable and liquid enough to raise sufficient money to compensate all investors, as well as any other creditors that FRE plc has borrowed money from.

This is not the first time; FRE’s June 2016 accounts were filed over four months late in May 2017, and FRE survived a compulsory strike-off notice in January 2017 after somebody objected (probably HMRC, possibly another creditor).

By not filing its accounts on time, FRE risks a further strike-off notice from Companies House, and the directors also risk a criminal prosecution. If Companies House files a strike-off notice and after two months the company has still failed to file accounts and no objections are received, the company is dissolved and all its assets become property of the Crown.

Should I invest with FRE plc?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 9.5% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, FRE plc’s bonds are higher risk than a diversified portfolio of mainstream stockmarket funds.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees and any higher-ranking borrowers are paid.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “secure” investment or one which is backed by the Government, you should not invest in unregulated products with a risk of 100% capital loss.

Given that basic due diligence into a loan investment would start with reviewing the company’s accounts, investors should also exercise extreme caution when investing in a company that has failed to file accounts on time.

Secured Energy Bonds raised £7.5 million from investors promising returns of 6.5% per annum. In 2015 the company went bust and administrators were appointed.

The administrators published their latest progress report on 3rd January.

The report makes it clear that it is extremely unlikely that investors will see a penny of their money back. In total, the administrators have recovered £109,000 net from Secured Energy Bonds plc, after legal and other costs. The administrators’ costs currently stand at £561,000, none of which has yet been paid.

This means that as it stands, the costs of the administrator (who always stands first in the queue) will swallow up all of the money recovered from Secured Energy Bonds, and the investors will receive nothing.

It seems extremely unlikely that any further assets realised by the administrators will be sufficient to cover the costs they have already incurred, and any further costs that will be clocked up as the administration continues.

The claim that these bonds were “asset-backed” was, as with Providence Bonds which collapsed a year later in 2016, completely worthless.

Sale of SEB’s assets

In 2017 the administrators managed to sell two of SEB’s subsidiaries, SEB Mercury and SEB Venus, for £203,150. The sales process was protracted due to the initial preferred purchaser withdrawing after conducting due diligence.

£17,197 was received in final dividends from interests in CBD Energy Limited and Westinghouse Solar Pty Ltd, which also went bust.

The administrator also received 13,959,588 shares in BlueNRGY Group Limited. Whether these are of any value depends on whether BlueNRGY manages to successfully relist itself on NASDAQ – in its latest SEC filing it states “there is no assurance that we will be successful in doing so”.

Ongoing Financial Ombudsman case

Investors in Secured Energy Bonds have launched a Financial Ombudsman complaint against Independent Portfolio Managers, over its role in promoting and acting as “Security Trustee” for Secured Energy Bonds. Initially, the Ombudsman declined to consider the complaint on the grounds that the SEB investors were not customers of IPM, but it reversed this decision in 2017. When the Ombudsman will issue its ruling is not known.

Bond on Blockchain is an equity cryptocurrency investment traded on the BitShares platform.

The Bond is designed as a five year investment, with investors permitted to redeem 60% of the Net Asset Value after one year, 70% after two years, 80% after three years, 90% after four years and 100% after five years.

The Bond can also be traded on the BitShares platform at any time provided a market exists.

However, under US securities law, the bonds are “restricted securities” and therefore may not lawfully be sold until one year after purchase.

The Bond’s funds are invested as follows:

30% in unregulated bonds issued by UK property companies

30% in the Billion Hero Campaign

30% in lending Bitcoin to speculators

10% in alternative cryptocurrencies

The literature states that the investments “will provide Bond with a steady rate of return, projected at a minimum annual rate of 8% of Net Asset Value”. This is however a projection; no fixed rate of return is promised and the bond’s Form D filing with the SEC describes it as an equity investment, meaning the value will depend purely on the value of its underlying assets (loans to property companies, loans to Bitcoin speculators, the HERO cryptocurrency and alternative cryptocurrencies).

Who are Bond on Blockchain?

Robert Edwards, Bond on Blockchain director

Bond on Blockchain is managed by Euskara Management Ltd, registered in Belize.

Robert John Edwards is the sole director and shareholder of Euskara Management and is described in the literature as the founder of the investment. Edwards is also the owner of Vino Beano Limited, a UK wine seller, and was previously the founder of a UK recruitment consultancy, Burrows & Grey Limited (formerly Be A Sport @ Work Limited). Burrows & Grey was dissolved in 2016.

Is Bond on Blockchain regulated?

On Edwards’ LinkedIn profile, Bond on Blockchain is described as “Regulated and 100% Asset Backed.” However, the company has filed with the SEC under Rule 506(c), meaning it is exempt from most of the stringent securities regulations in the US and is to all practical purposes unregulated. Bond on Blockchain is not required to file with the SEC beyond a very short Form D notice.

The Rule 506 exemption means that Bond on Blockchain may only be promoted to “accredited investors”, which generally means investors who earn over $200,000 per annum or have net wealth of $1 million excluding your house. Firms relying on Regulation D 506(c) must take reasonable steps to ensure investors qualify as accredited “which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like.”(SEC.gov)

Sitting slightly uneasily with the requirement to be promoted to accredited investors is a cartoon promotion for Bond on Blockchain featuring the Spot The Dog kiddy language currently beloved of adpeople (This is Tim. Tim has Bitcoin, but the value always fluctuates” etc), the worst beard ever seen in financial advertising,

…and the kind of sexism we thought went out of style fifty years ago (“Tim is very happy. Because now he can tell his wife that they have a secure savings option on the blockchain.”) with a simpering housewife who is seemingly only prevented from sticking her heel in the air and kissing Tim on the cheek by the animators’ inability to draw people from the waist down.

Technology from 2017, advertising from 1957.

But accredited investors are unlikely to make their investment decisions based on the merits of cartoon adverts, so let’s move swiftly on.

How safe is the investment?

The 30% allocated to cryptocurrency lending is straightforward enough. Bond on Blockchain lends out investors’ money to Bitcoin speculators who attempt to make money speculating on Bitcoin. If they succeed, they can pay Bond on Blockchain back from their profits, but if they fail, there is a risk to Bond on Blockchain that they cannot repay their loans.

https://bondonblockchain.com/asset/ shows that the 30% to be allocated to “Property bond / real estate” will be allocated to three unregulated loan notes issued by UK property companies: Blackmore Bond, Marcello Developments and Nova Prime.

This means that 60% of Bond on Blockchain’s assets consist of fixed interest loans to third parties – UK property companies and cryptocurrency speculators.

The 10% to be invested in alternative cryptocurrencies is self-explanatory.

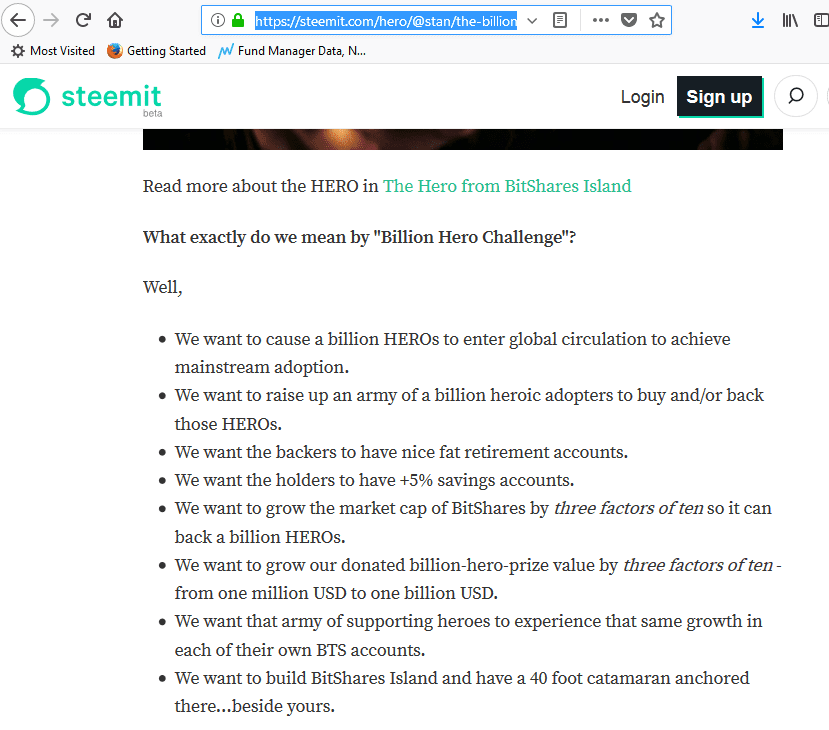

The 30% to be invested in the “Billion Hero Campaign” is where things get distinctly murky.

Billion Hero Campaign

The PDF literature states that 30% of investors’ money will be invested in the Billion Hero Challenge.

The Billion Hero Challenge was a proposed “contest” from the founder of the HERO cryptocurrency. Bond on Blockchain’s literature refers to the Billion Hero contest as involving the purchase of BitShares. This is not correct – HERO is a separate currency, which is collateralised using BitShares.

HERO’s founders claim that HERO is designed to appreciate by 5% each year with reference to the US dollar. This is achieved via its collateralisation with BitShares, on the grounds that as BitShares rise in value, the HERO will be able to deliver guaranteed returns of 5% per annum from its share in BitShares’ profits.

There is clearly a risk that BitShares fails to make sufficient profits to allow investors in HERO to cash out at the value of BitShares +5%pa.

We will leave the merits of HERO aside at this point and focus on the Billion Hero Challenge. The rules were simple: a prize fund containing a million dollars worth of HERO would be set aside at the beginning of the contest. Teams of contestants would be encouraged to buy and bid up the price of HEROs until the point that the value of the prize fund reached a billion dollars. At the point the prize fund reached a billion dollars, it would be divided among the twelve teams holding the most HEROs.

I use the past tense because the contest appears to have flopped. The total value of all HERO in existence (market cap) is currently under a million. The contest was to be tracked using a leaderboard on https://sovereignhero.com/, but of this there is no sign. Coinmarketcap.com suggests that the total market cap of HERO has never exceeded a million dollars, so clearly it was not possible to start with a prize fund of a million dollars.

Even if it had successfully launched, the contest strongly resembles a pump and dump scheme. If people are buying HERO in the hope of a) increasing the prize fund value to a billion dollars and b) holding more than other contestants at that point, then when they win the prize, all they have is “a billion dollars worth” of a currency that nobody wants to buy anymore, as the reason for buying it has evaporated.

This problem was explained away by the HERO founder as follows: by the time the prize fund reaches a billion dollars, HERO will be in use as a currency to such an extent that the disappearance of the Billion-Hero-Challenge-led demand will not have a material effect on the price.

With the collapse of the Billion Hero Challenge and HERO’s market cap yet to breach $1 million, it is impossible to say whether mass adoption of HERO was ever a realistic possibility.

Nonetheless, it is notable that Bond on Blockchain, while claiming that “In a market of volatility and ‘get-quick-rich’ promises, Bond offers security and stability”, planned to invest 30% of investors’ money in a get-rich-quick scheme, until it flopped at launch.

If this isn’t a description of a get-rich-quick scheme, I’m Ruja Ignatova.

HERO now appears to be running something called the Billion Hero Campaign, which “was conceived as a unique platform designed for fundraisers, charities, and foundations with a noble cause”. https://bondonblockchain.com/asset/ now lists the Billion Hero Campaign as the destination of 30% of funds.

It is not clear how exactly charity fundraising is expected to deliver a return for Bond on Blockchain investors. No explanation on how the campaign works is provided by billionherocampaign.com, other than some YouTube videos which demonstrate how to use the website.

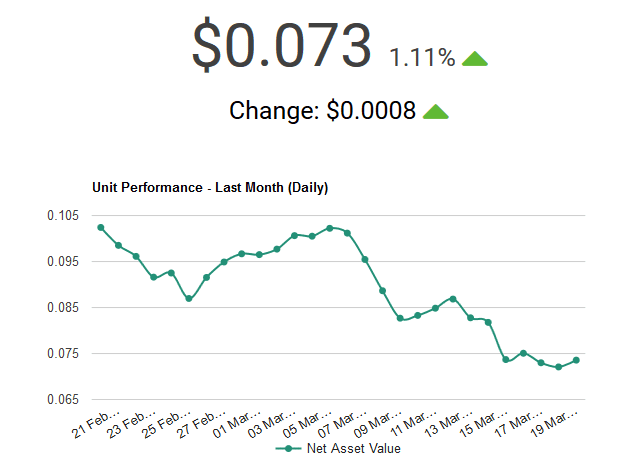

According to the literature, “an initial 5,000,000 Bond Units have been made available for presale purchase, at an initial $1 per unit, with the minimum level $500. At the time of writing, Bond Unit’s value has already reached $1.368 – a 36.8% rise.” The URL of the document dates this literature to December 2017.

As of March 2018, Bondonblockchain.com shows the value has collapsed to 7.3 cents.

Charges and costs

No details are given in the literature or in the Form D filing with the SEC as to what management fees will be collected from Bond on Blockchain, or any other details on how the cost of Robert Edwards’ management of the fund will be paid.

Should I invest with Bond on Blockchain?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Bond on Blockchain has certainly had a rough start to life given that its literature states that its shares were traded at $1.368 in December 2017, and the value has since collapsed to 7.3 cents at time of writing (nearly a 95% loss) according to its website.

Accredited investors who sense a buying opportunity should be aware that they are investing in assets which all have a possibility of total and permanent loss, namely

“alternative cryptocurrencies” (which may fail to gain acceptance and collapse in value or become untradeable)

loans to unregulated property companies Blackmore, Marcello Developments and Nova Prime

loans to cryptocurrency speculators

and the HERO cryptocurrency via the Billion Hero Campaign.

Buying a product which has lost 95% of its value only makes sense if you have concrete reason to believe that the underlying assets are undervalued by the market and will recover in value, or if you regard the investment as a total gamble and are prepared for 100% losses.

With a 95% fall in value from its December 2017 price and a 92% fall from its initial offering price, Bond on Blockchain has clearly failed in its aim to reduce the volatility associated with cryptocurrency.

Bond on Blockchain’s failure to disclose its charges (or however it pays for the cost of Edwards and others managing the fund) anywhere in its literature or website is disappointing in this day and age.

Independent Portfolio Managers Limited hit the headlines due to its role in the promotion of two failed unregulated bond issuers – Secured Energy Bonds and Providence Bonds, both of which went bust and lost all the investors’ money.

In November last year the company agreed with the FCA to cease all regulated activities.

On 30 December, the date IPM’s accounts were due to be filed with Companies House, the company instead elected to extend its accounting period by the maximum six months. This means it will now not have to file updated accounts until 30 June 2018. UK companies are permitted to extend their accounting period by up to six months providing they are not already overdue and haven’t already done this in the last 5 years.

IPM is currently the subject of multiple Financial Ombudsman complaints in regard to its role in approving the literature issued by Secured Energy Bonds and Providence Bonds. Neither Secured Energy Bonds nor Providence Bonds were regulated, so the bonds could not legally have been promoted to investors without an FCA-regulated firm to approve their literature – which is where IPM came in.

The FOS said initially that it would not consider the complaints as the Secured Energy and Providence investors were not customers of IPM. However they reversed that stance in April 2017, and are currently considering the complaints. How close we are to the Ombudsman giving a verdict is unknown.

What is also increasingly unclear, thanks in part to IPM staving off the date it has to file it accounts, is whether IPM has sufficient resources to meet investor claims to any meaningful extent. In its last accounts (March 2016), now two years old, it declared net assets of £128k. Investors are believed to have lost a total of £15 million in Providence and Secured Energy bonds.

We await the outcome of the FOS cases with interest. In the meantime, investors in Providence Bonds and Secured Energy Bonds can contact the relevant Investor Action Group on [email protected] and [email protected].

Investors should be extremely wary of anyone who asks them for money and claims they can recover any part of their investment, and should read up on fraud recovery fraud. By all means consult a regulated reputable solicitor, but be wary of throwing good money after bad.

For many years now, the regulated investment industry has attempted to classify both investment products and investors on a scale of risk – sometimes 1 to 5, sometimes 1 to 7 and sometimes 1 to 10.

The idea is simple and uncontroversial enough – a very cautious investor who cannot stomach any fluctuations in value would be a 1/10, and should only buy products that are 1/10 on the risk scale. While very-high-risk products that are 10/10 for risk (or 5/5 or 7/7 depending on whose scale you used) would only be purchased by investors willing to take that risk. Most people fall somewhere in the middle.

This idea of a risk scale found its way into regulation; everyone who offers investment products to the public in the European Union has to issue a Key Investor Information Document which shows where its product sits on a scale of 1 to 7, determined by its volatility (how much its product goes up and down on a daily basis).

Two common risk scales: the first is used by Distribution Technology (a leading risk profiling firm), the second is the risk scale mandated for use in Key Investor Documents by EU law. The third is the scale they are measured against; the investment’s volatility (how much it goes up and down).

Here is the problem with these risk scales: whether the scale tops out at 5, 7 or 10, they only consider products available via the regulated investment sector, and whose moving parts are listed on mainstream stock markets. This means a 10/10 risk investment is considered something like an emerging markets or smaller companies fund.

But there are quite obviously many investments which are higher risk than an emerging markets fund – many of which are routinely held by retail investors, such as individual shares or buy-to-let residential properties. These investments can not only fluctuate by more than 10/10 risk-rated funds; they can generate permanent and total losses.

Why is this a problem? Because promoters of unregulated investments have been known to hand-wave away the risk of losing money by saying something along the lines of “all investments have risk”. Logically, this is like chucking a novice swimmer in the deep end of the pool and then saying “all swimming pools have water”. They are denying that there is such a thing as a scale at all.

But if the experts routinely use a risk scale that can’t accommodate even commonplace investments like individual blue-chip shares and residential properties, how is the investor supposed to know which end of the pool they’re about to jump into when they’re offered an investment that doesn’t sit on the scale?

Instead of focusing on volatility (which falls apart at the higher end of the risk scale where volatility cannot be measured), the following risk scale measures investments by what retail investors actually want to know, which is a) can I get my money out? b) can I lose money?

Short term risk

Long term risk

Low risk

e.g. Easy-access deposit guaranteed by FSCS or other depositor protection scheme

Negligible risk of loss

Negligible risk of loss

Medium risk

e.g. Globally diversified portfolio of mainstream regulated equity funds

Fluctuates in value; bought and sold daily

Negligible risk of permanent loss if held throughout the market cycle

High risk

e.g. Single-sector or single-country regulated equity fund

Fluctuates in value; bought and sold daily

Risk of long-term loss even if held throughout the market cycle

Extra high risk type A

e.g. Individual buy-to-let residential property

Fluctuates in value; may be difficult to sell quickly

Risk of permanent loss

Extra high risk type B

e.g. Individual S&P 500 or FTSE Main Market equity

Fluctuates in value; bought and sold daily

Risk of total and permanent loss

Ultra high risk

e.g. Unlisted individual loan notes, unregulated fund which can borrow to invest

Fluctuates in value; may be illiquid; may be impossible to sell quickly

Risk of total and permanent loss

Scam

e.g. Ponzi scheme, advance fee fraud, binary options scam, etc

Near-certainty of total and permanent loss

Near-certainty of total and permanent loss

There are investments which do not sit comfortably in the above table, such as FSCS-protected fixed term deposits (low risk but illiquid) or bricks and mortar funds (generally considered medium risk but illiquid at times of crisis). However, these are niche solutions and the above table shows the progression of risk through the more common investments.

For those less familiar with the investment market, a little more explanation:

By a medium-risk “globally diversified portfolio” we mean a portfolio holding thousands of securities representing all global stockmarkets. This could be a single highly diversified multi-asset fund or a mixture of single-sector funds. Although such a portfolio will at times experience severe falls in value (in the last major crash in 2008, a typical fall was 30-40%), as long as the portfolio is properly diversified, the investment will recover when global stockmarkets recover.

By a high-risk investent we mean those which can lose money in the long term even after global stockmarkets have recovered. There were Japanese funds at the end of the 1980s which never recovered from the “lost decade”, even though they were diversified across lots of Japanese companies. This is why no-one should have all their money invested in Japan, or any single country, even if you live in it.

An extra high risk investment has no diversification, and is different from a plain high risk investment in one of two ways. Either a) it is illiquid and difficult to sell, or b) it is liquid but presents a risk of total and permanent loss (like S&P 500 or FTSE Main Market shares).

Residential property falls under type a), despite being considered by many laypeople as “safe”, because the reality is that residential properties can and do lose money if you get a bad tenant and have to spend money repairing the house instead of making money, and if the house fails to appreciate in value. (House price indices generally go up, but individual houses don’t always.)

An investment which has both illiquidity and risk of permanent and total loss is an ultra-high-risk investment.

A total loss is by its nature permanent.

People often make mistakes when managing medium- and high-risk investments (like betting too heavily on Japan or cashing out at the wrong moment) but as these investments have very little risk of total loss, these mistakes are usually fixable. And because these investments are generally liquid, the investor can correct their mistake as soon as they recognise it, albeit at a cost.

By contrast, someone who mistakenly invests in an ultra-high-risk investment does not usually realise their error until the money is already gone. And there is nothing to switch into a more diversified portfolio, and no way of correcting their error.

This is why developed regulatory systems have at their core the belief that unregistered securities should not be sold to the general public. There is no point saying “caveat emptor“ if the emptor has no way of knowing they should cavere until their wallet has already been emptied.

This is of course all a little academic: ultra-high-risk investments are generally exempted by the EU regulatory system from any requirement to hand investors a document which might show that they are being offered a maroon-level ultra-high-risk investment (as opposed to a “secured” “asset-backed” “insured” “bond”). But we can dream.

Privilege Wealth offered unregulated corporate loan note investments paying 9.85% per annum for a term of three or five years (based on an archived version of privilegewealthlp.com from March 2016). It described these as “low-risk, insured notes”. Investors’ money was to be used to fund payday loans in the United States.

Privilege Wealth PLC has now collapsed and entered administration, with Stephen Katz of David Rubin & Partners appointed as administrator. A statement of affairs was filed with Companies House on 26 February 2018.

According to the Statement of Affairs, Privilege Wealth PLC owes £42 million to various unsecured creditors, of which by far the largest amount, £28.4 million, is owed to Privilege Wealth One LLP, which is believed to represent investors who invested in its loan notes.

To meet these claims, Privilege Wealth PLC has £2,205 in the bank and a £2,353 VAT refund. All its other assets are listed by the administrator as of uncertain value. Under “Estimated to Realise” the administrator lists the total estimated assets as £4,558.

While some of its assets with “Uncertain” value, which include “Shares & Investments” (book value £9.5 million, actual value Uncertain) “Promissory Notes Receivable” (book value £16.3 million, actual value Uncertain) and “Promissory Notes Interest Payable” (book value £17.3 million, actual value Uncertain) may yet return some money, investors would be wise to manage their expectations.

Unless significant amounts can be realised from these assets of Uncertain value, the cash in the company will first be used to pay the administrator’s fees (the administrator always stands in the queue) and investors are at risk of 100% loss.

Who were Privilege Wealth?

The statement of affairs shows that Privilege Wealth plc was owned 20% by Bowline Private Fund in the Cayman Islands, 40% by Mark Munnelly (European Operations Director according to privilegewealthlp.com), 30% by Martin Sampson (Director) and 10% by Tomasz Pawelek (Director). Who controls Bowline Private Fund is not known.

Banned director Brett Jolly (who was banned from acting as a director for his conduct while acting for Anglo-Capital Partners Limited, a collapsed carbon credit scam) was also a Limited Partner of the Privilege Wealth One Limited Partnership. In a “letter to the editor” to Offshore Alert, he vehemently denies any wrongdoing, and says that while he was “very much involved with them since early on in their evolution”, his role was limited to “introductions to commissioned sales people” and that he was not an “owner” of Privilege Wealth.

Also part of the organisation was Christopher Burton, who ran a call centre for Privilege Wealth in Panama. In April 2017, Burton was shot three times in an assassination attempt. After recovering from his injuries, he awaits extradition to Spain for his role in a boiler room scam in Marbella.

“Low-risk” “insured” notes?

Privilege Wealth claimed on its website “Re-insurance of 95% of all utilised capital by “A Rated” insurers and “95% of Capital insured against loss”.

“100% of the Capital Value of each Loan Note (with a 5% deductible) is insured against “Default” and “Wrongful Act” by the General Partner”, and includes the following types of cover:”

There then follows a long list of types of cover, but the one of most interest to investors is

Default by the financial institution, the General Partner (and Partnership) in terms of the non-payment of 100% of the principal Capital Value of each Loan Note as loaned by any Loan Note Holder or Limited Partner to the General Partner (and Partnership) as agreed and signed in any Loan Note transaction between the General Partner and the respective Limited Partner.

However, this page then finishes off

* This is a broad terms description of the insurance policy for illustrative purposes only. The only contractual reference to insurance in contained in the policy itself.

Whether investors will indeed receive 95% of their capital back looks extremely unlikely at this stage.

This illustrates that when an unregulated bond is described as being “insured”, investors cannot assume that this will give them any protection against losses unless they have obtained watertight professional due diligence on the insurance contract, and on the insurer providing the insurance, and are therefore confident that the insurance will in fact pay out in the event of capital loss.

Legal case

Privilege Wealth successfully sued David Marchant of the well-known scam awareness blog OffshoreAlert.com for £80,000 after Marchant described Privilege Wealth as a fraud. The judge described this claim as “baseless” and stated that Privilege was “clearly not a fraud”.

Privilege had only claimed damages of £50,000, but the judge awarded £80,000 against Marchant, because Marchant had signalled his intention to ignore the judgment and continue publishing the material.

Less than a year after this judgment, Privilege Wealth has collapsed.

So much for “truth is an absolute defence”?

Not really. Firstly, Marchant didn’t enter any defence, relying on the fact that a UK libel judgment couldn’t be enforced against him in the United States. Secondly, it is still not established that Privilege was a fraud. (The long list of allegations made by Brett Jolly against the scheme to Offshore Alert doesn’t look good, but they are as yet unproven.) Running a failed investment is not fraud.

I don’t say this to excuse Privilege; I say this because time and again we see people justifying investment in ultra-high-risk investments with the rationale “if it wasn’t legit, the police or the regulators would shut it down”. If you invest in ultra-high-risk unregulated investments, neither the police, the regulators nor anyone else are going to save you from losing your money.

According to the administrator’s statement, the lawyers who won that libel case for Privilege, Lewis Silkin LLP, are still owed £45,000. They must now join Privilege’s investors at the back of the queue.

New Nordic Group and Emerging Trends RE Corp have “teamed up” to offer a range of unregulated investments (structured as redeemable convertible preference shares):

Option A Guaranteed Regular Returns – The Secondary Income Investment: 7% “rental guarantee” paid monthly (quarterly for investments under $10,000, under 3.5 million thai baht [about £80,000], or “foreign payments”) for a term of 15 years

Option B Guaranteed Capital Gain – The Long Term Income Investment:

Option 1: 5% simple interest rolled up and paid out after 3 years (equivalent to 4.8%pa compound interest)

Option 2: 7% simple interest rolled up and paid out after 5 years (6.2%pa compound interest)

Option 3: 10% simple interest rolled up and paid out after 10 years (7.1%pa compound interest)

Option 4: 12% simple interest rolled up and paid out after 15 years (7.1% compound interest)

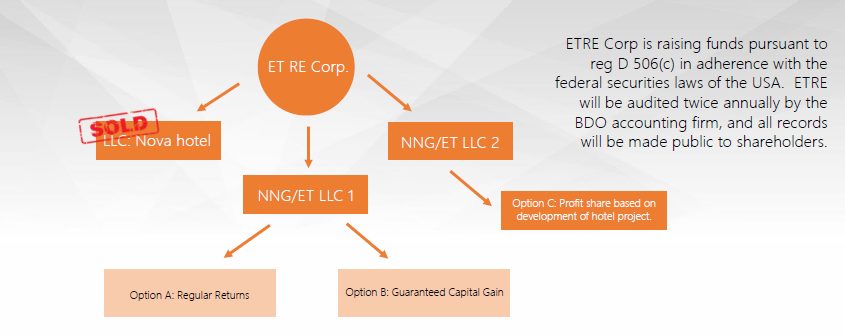

Option C: Capital Gain based on Profit Share: The Short Term Investment – preference shares in a company (NNG/ET LLC 2) developing a hotel project in Pratamnak Hill, Thailand.

All three options are structured as preference shares, issued by two companies owned by Emerging Trends RE Corp:

NNG/ET LLC 1, which is the issuer of the preference shares under Options A and B

and NNG/ET LLC 2, which is the issuer of the preference shares under Option C.

Unlike options A and B, returns from option C are variable and presumably depend on the price the development can be sold for on completion of construction. We have seen two brochures (one for all three options, one covering Option C only) which provide different projections for Option C. The first describes the term as “Approximately 2 years from construction commencement. Anticipated to begin July 2018” and says “anticipated project profits to be at 30%-60% (based on construction price, re-sale value and Hotel Brand long term operational forecasts)”. (“Hotel Brand” appears to be placeholder text.)

The second brochure states “Estimated term: 2-4 years” and “Estimated return: 42%”.

Details on the exit route for the Option C investment in the literature are somewhat vague. The second brochure says “We are developing a hotel project in Pratamnak Hill together with one of the world’s biggest hotel chains” – presumably, in order to return investors’ capital, the hotel chain in question is to pay NNG/ET LLC 2 on completion. However, the identity of this buyer is not clear. On page 16 of the second brochure, under “Operations” the page is blank except for the text “Will add details of hotel brand”.

Who are New Nordic Group?

No information is provided on New Nordic’s website as to who controls the business. A number of “country managers” and other members of middle management are shown, but no Chief Executive Officer / Managing Director / Chairperson is named, or any other information or who the directors or owners of the company are.

There are a number of “New Nordic” companies registered in various countries, including the UK. I was not able to establish who the ultimate owners or controllers of New Nordic Group are.

New Nordic has been in business since 2009.

Who are Emerging Trends RE Corp?

David Simpson, CEO of Emerging Trends RE Corp

Emerging Trends RE Corporation was incorporated in the State of Delaware, USA on 26 May 2017.

According to Emerging Trends RE’s website, the Chief Executive Officer is David Jules Simpson, a former Trainee Adviser at Co-operative Insurance (now Royal London). According to the FCA Register David Simpson left Royal London in 2005. Prior to returning to the world of finance, Simpson ran lovepattayathailand.com, a website providing news and classifieds for the Thai resort city of Pattaya.

The other directors are Senior Executive Bob Pritchard, a marketing consultant and author of books including “Kick Ass Business and Marketing Secrets”, and Head of Design & Technology Tommy Wiberg.

The company describes itself as “a modern day alternative to a high street bank”. As the company offers only capital-at-risk investments, the company is clearly not an alternative to a high street bank offering regulated deposits.

How safe are New Nordic / Emerging Trends RE’s investments?

These investments are unregulated preference shares and if the issuer defaults you risk losing up to 100% of your money.

The investments are described as “redeemable convertible preference shares”. The purpose of raising money via preference shares under all three options is to allow New Nordic Group to develop residential and commercial property.

Under options A and B, if New Nordic Group fails to make sufficient profits from its property developments, or for any other reason Grove Developments has insufficient money to pay the promised coupons, and redeem the preference shares at the promised date, there is a risk that they may default on payments of interest and capital to investors.

Under option C, if New Nordic Group is for any reason unable to complete and sell the hotel development, the company is wound up, and there are insufficient funds in NNG/ET LLP 2 to compensate preference shareholders, there is again a risk that preference shareholders’ money may be lost.

Investors’ money is secured on property and cash owned by the LLPs (NNG/ET LLP 1 in the case of Options A and B, and and NNG/ET LLP 2 in the case of option C).

Before relying on this security, it is essential that investors undertake professional due diligence on NNH/ET LLP 1 and/or 2 to ensure that in the event of a default, the assets owned by the company would raise enough money to compensate investors, as well as any other debtors.

Investors should not assume that because the loans are asset-backed, they are guaranteed to get at least some of their money back through sale of the collateral if the company defaults. If the companies have insufficient assets to compensate all investors after meeting liabities to the insolvency administrator (who always stands first in the queue) and any other creditors who rank above the preference shareholders, they can still potentially lose up to 100% of their money.

The literature states “All investment options offered by ET in conjunction with NNG are fully secured by property or cash meaning that these are the safest types of investment available.” This is a highly misleading statement. As discussed above, preference shares secured on the assets of the company have potential for up to 100% loss if the assets of the company are insufficient to pay preference shareholders, after paying the insolvency administrator and any higher-ranking creditors.

Conventionally speaking, the safest type of investment available is a deposit account protected by a depositor compensation scheme, which carries virtually zero default risk. A portfolio of stocks and shares diversified across thousands of individual securities is riskier than a deposit account, but carries virtually no risk of permanent and total loss, and is therefore lower risk than an individual preference shares (secured on assets or not).

Are New Nordic / Emerging Trends RE’s investments “regulated”?

The first brochure describes the investments as “fully regulated and protected by US Law”. However, the second brochure states that “ETRE Corp is raising funds pursuant to reg D 506(c) in adherence with the federal securities laws of the USA”. Emerging Trends RE Corp also states that the firm relies on Regulation D 506.

Reg D 506(c) allows investments to be exempt from the stringent registration requirements of US securities law, providing that the investment is only sold to accredited investors – investors with more than $200,000 annual income or $1 million in assets excluding their house. Firms relying on Regulation D 506(c) must take reasonable steps to ensure investors qualify as accredited “which could include reviewing documentation, such as W-2s, tax returns, bank and brokerage statements, credit reports and the like.”(SEC.gov)

As the entire point of Regulation D 506(c) is to exempt certain securities offerings from SEC regulation, an investment relying on Regulation D 506(c) is for all practical purposes unregulated. They are not required to file with the SEC beyond a very short “Form D” notice.

A search for “New Nordic” and “Emerging Trends” on the SEC’s EDGAR database for their Form D notices returned no results at time of writing.

Should I invest with New Nordic Group / Emerging Trends RE Corp?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Although all three options are structured as individual preference shares, Options A and B are essentially loans, with a fixed coupon and the promise to return capital at the end of a fixed term. Option C is an equity investment, with the term depending on the progress of construction, and the return depending on how much the property is sold for at the end of construction; although NNG gives a projected return, no promises are made as to how much the return will be.

Both individual loans and individual equity securities are only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

As discussed above, New Nordic / Emerging Trends RE’s investments are higher risk than a diversified portfolio of mainstream stockmarket funds, despite their claims to offer the “safest types of investment available”.

These investments are described as asset-backed. Before relying on the security backing the investments, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees and any other borrowers are paid.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for the “safest types of investment available”, you should not invest in unregulated products with a risk of 100% capital loss.

Popularly known as

Popularly known as  uture Renewables Eco plc was incorporated in May 2015, and is 100% owned by Future Renewables Eco Energy Ltd, which in turn has three shareholders: Jadenorth Properties Limited 45%, Bananas Consulting Ltd 45% and Anne Sellar 10%.

uture Renewables Eco plc was incorporated in May 2015, and is 100% owned by Future Renewables Eco Energy Ltd, which in turn has three shareholders: Jadenorth Properties Limited 45%, Bananas Consulting Ltd 45% and Anne Sellar 10%.