First Alternative Group offers managed spread betting on currency claiming “Average earnings are 3% to 6% per month”.

Spread betting is not explicitly mentioned on the website, but an internal URL refers to “spread trading” and the statement “tax free profits in the UK” strongly suggests that spread betting is being offered. Investment gains (including on forex trading) are subject to capital gains tax in the UK, but gains from spread betting are considered gambling wins and are therefore tax free.

In a video on the website, an unnamed person standing in front of a picture of an office (the lack of motion in the background makes it clear that he is standing in front of a still image) claims that First Alternative will “guarantee to outperform your standard investment classes, which on average earn less than 10% per year”. He also refers to it as a “secure investment”.

Who are First Alternative Group?

Unnamed First Alternative representative

No details are provided on the website as to who is behind the business.

The site states “Expertly managed account with TAX FREE profits in the UK” but no UK address or company details are provided. The domain registration details of firstalternativegroup.com have been hidden.

How safe is First Alternative Group?

Notwithstanding First Alternative Group’s claim that the investment is “secure” and that they “guarantee to outperform standard investment classes”, spread betting is ultra high risk and can result in 100% losses; depending on the type of spread bet, investors can lose more money than they put in. Describing any spread betting or forex trading investment as “secure” is highly misleading.

If First Alternative Group fails to consistently win on its spread bets, investors may lose up to 100% of their money – and potentially more than they deposited if First Alternative Group exposes them to more than they deposited.

First Alternative Group promise to refund investors’ money within 30 days if they are not satisfied. The guarantee applies to £500, £2,500 or £5,000 “trial accounts”. This guarantee relies on First Alternative Group having sufficient funds available to refund investors. As does any guarantee “to outperform standard investment classes”.

Due to the lack of information provided by First Alternative Group, it is impossible to assess how likely First Alternative Group is to be able to fulfil its guarantees.

Should I invest with First Alternative Group?

Spread betting is, as the name suggests, gambling and 100% losses or greater are a strong possibility. Nothing that First Alternative Group claims about its ability to generate average returns of 3% to 5% a month, its guarantee to refund investors within 30 days or its guarantee to outperform alternative investments changes that.

Spread betting is regulated in the UK by the Financial Conduct Authority. However a search for First Alternative Group on the FCA’s register produced no results. First Alternative Group does not claim any regulatory authorisation on their website.

Investors should think carefully before handing over money to any business which does not disclose any physical address details or details of who is behind it.

Do not proceed unless you are prepared for 100% losses.

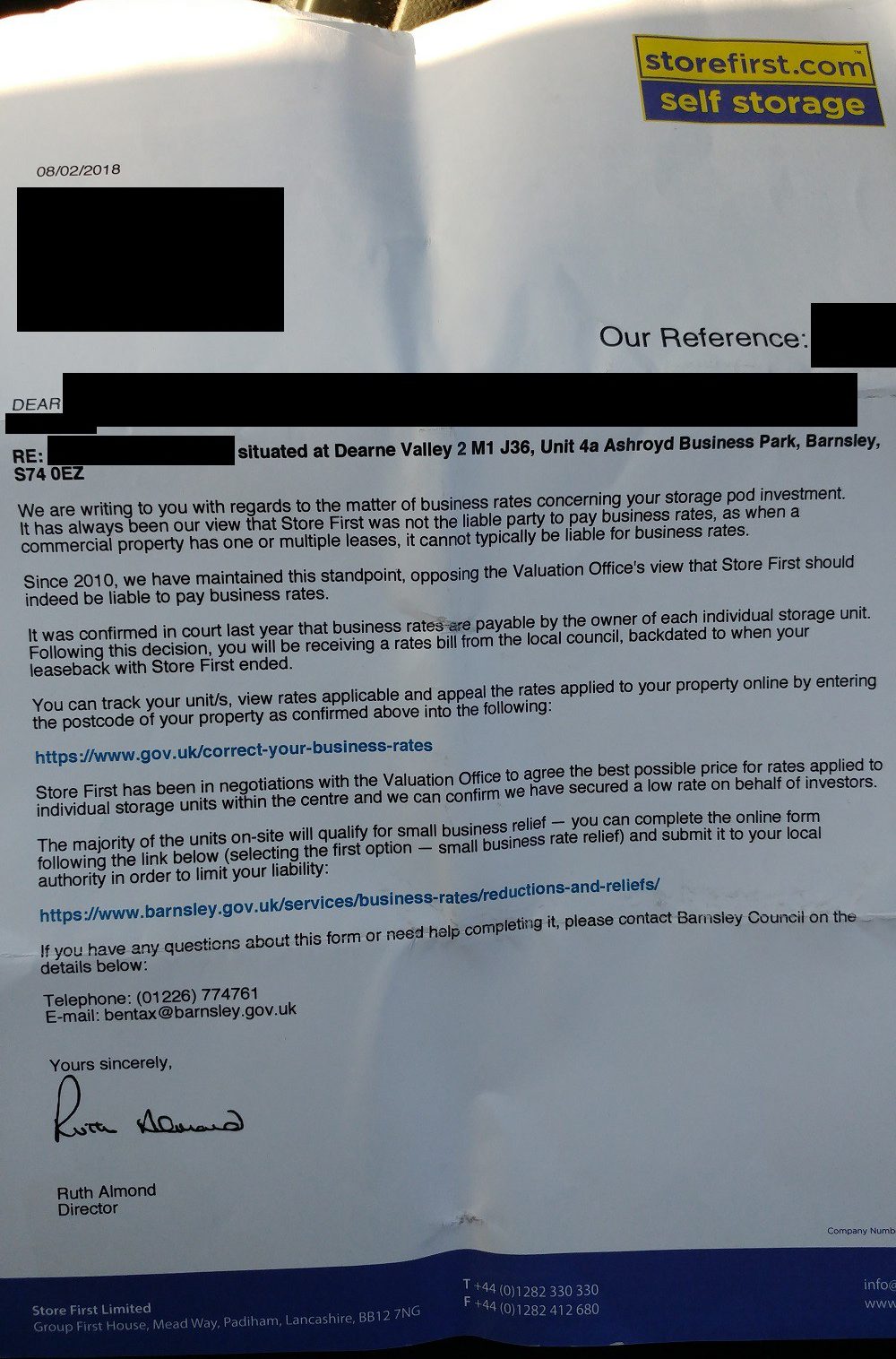

Store First offered investors the opportunity to invest in storage pods with the promise of an 8% “guaranteed” return in the early years.

In a number of cases these guaranteed returns however quickly dried up; an investor has told us that they received the promised “guaranteed” returns for 12 months but these payments then stopped. Store First pods have been seen on Rightmove being offered for as little as £3,940 (almost certainly considerably less than the seller paid for them). Whether these pods were actually sold is not known.

On top of this, Store First has recently written to investors to tell them that they are liable to pay business rates to Barnsley Council (and not, as the Valuation Office had previously argued, Store First itself).

Business rates are calculated based on the “rateable value” of a property – in this case the storage pod.

Store First’s letter says “Store First has been in negotiations with the Valuation Office to agree the best possible price for rates applied to individual storage units within the centre and we can confirm we have secured a low rate on behalf of investors”.

By “best possible price” Store First means the lowest possible price as the lower the value of a property, the less tax the business owner is liable for. So essentially Store First have been spending their time trying to persuade the Valuation Office that Store First pods are worth as little as possible.

Sadly for investors, the Valuation Office has apparently not taken the view that the storage pods are near-worthless, as otherwise no business rates would be charged.

Future developments

In 2017 the Secretary of State for Business lodged a petition in the High Court to wind up Store First and various associated companies. The petitions were adjourned in July 2017. At time of writing, a court date has still not been set.

Also in July 2017, Store First Limited extended its accounting period by six months, giving it another six months to publish its 2017 accounts. The accounts are now due to be filed with Companies House within the next month, by the end of March 2018. (Store First cannot extend the accounting period again as the period for the 2017 accounts is already the maximum eighteen months, plus you can only do this once every five years.)

Unfortunately for investors, the rateable value determined by the Valuation Office is somewhat theoretical and based on the rent that the property could have been let for in 2015, based on its size, location and the nature of the property. The VO may have taken the view that it is not their problem that some Store First investors are unable to realise any rent from their property.

Nonetheless, it would seem well-advised for individual Store First investors to contact Barnsley Council and the Valuations Office as a matter of urgency and appeal the rateable value of their investment that Store First has “negotiated” on their behalf, on the basis that the market value of the property is considerably less. We are not able to say whether this has any chance of success, but it is surely worth trying. Details of how to challenge a rateable value can be found on gov.uk.

There is another obvious way out of this mess. Investors in Store First were told they had a “buy back option” after five years. A Store First investor has told us that when they applied to exercise the buy back option, they were told it is optional, and that Store First has another five years in which to decide whether to buy the investment back.

The solution is for Store First to offer to buy the investors’ pods back immediately at the rateable value they “negotiated” with the Valuations Office. If Store First has negotiated this value with the Valuations Office, they must surely believe it represents fair value.

While this would likely result in investors writing off a significant loss, it would free them from having to pay further money to Barnsley Council on top of what they paid for the storage pod. Store First, in exchange, would get their storage pod at a value they believe is fair, along with the yield from future storage customers.

Supercar Investment Club offer the opportunity to invest collectively in supercars, with units starting at £500.

At time of writing, the company is yet to actually invest in a supercar; it has recently launched and is in the process of raising enough money to buy its first.

Once sufficient funds have been raised, the company will purchase supercars and hold them for a minimum of three years. After three years has passed, the supercar will be offered on the open market. If it can be sold for a profit, Supercar Investment Club will automatically sell the car. If an offer is received which makes a loss for investors, investors will vote on whether to accept it, in proportion to their invested funds. If investors holding a 50% majority share vote against selling it, the car will continue to be held.

During the three year period, if Supercar Investment Club receive any offers which would make a profit for investors, these will similarly be put to an investor vote. Offers during the three year period which would make a loss will be automatically rejected.

Supercar Investment Club charge a 6% initial fee, a 1% fee over three years and take 15% of any gross profits on sale.

Who are Supercar Investment Club?

Supercar Investment Club’s website provides no details of who is behind the business.

Companies House shows that Adam Sanderson is the sole director and owner of Supercar Investment Club Limited. The company was incorporated in July 2017.

Supercar Investment Club is regulated by the Financial Conduct Authority as an appointed representative of Prosper Capital LLP.

How safe is the investment?

To their credit, Supercar Investment Club makes extremely clear on their website that investors’ capital is at risk and that investors should take advice if they are in any doubt.

It is, as SIC says, perfectly possible to buy a supercar and sell it for a higher amount later.

However, this relies largely on luck and the whims of the market. A supercar is still a car and in the long term would be expected to depreciate in value, even if the rarity value of a well-maintained supercar can counteract this to some extent.

If, after the three year period is up, no buyer can be found who will offer Supercar Investment Club enough money to make a profit for investors, investors could find their money locked up indefinitely, until investors holding a 50% majority share vote in favour of cutting their losses.

Supercar Investment Club has the right to deduct “unexpected costs” from any sale price.

Investors could therefore lose up to 100% of their money if Supercar’s fees and any unexpected costs exceed the price that the car can be sold for.

Prior to being invested in a supercar, investors’ money is held with Mangopay, a company regulated in Luxembourg.

Should I invest with Supercar Investment Club?

This blog does not provide financial advice. The following is not a personalised recommendation, but a list of facts and general principles that investors should consider.

As mentioned above, it is perfectly possible to buy a supercar and sell it for a profit a few years later. But this is pure speculation, and relies essentially on luck. A supercar has no yield (in theory it could be rented out but this would result in more rapid depreciation; Supercar Investment Club say that the car will only be driven for yearly events, which precludes renting it out). This means investors are relying entirely on someone coming on along in three years and offering a larger sum for the car in the future.

“Luxury goods” investments such as supercars, fine wines and art are generally only suitable for high net worth investors who already have so much invested in conventional stockmarket investments that diversifying into assets with no yield starts to make sense.

The biggest attraction of a supercar as an investment for a high net worth investor is that even if it never makes a return, they can drive it around, or show it off in their garage. The same doesn’t apply to someone investing collectively in a supercar.

Supercar Investment Club’s fees (amounting to 2.33% per annum over the life of the investment, assuming there is an exit after three years, and 15% of gross profits) are extremely high compared to the fees charged on conventional stockmarket investments. Though SIC could quite reasonably say that this isn’t a conventional stockmarket investment, and that there is no real basis for comparison as there are virtually no other companies offering collective investment in supercars.

Before investing, investors should ask themselves:

How would I feel if the market collapsed for the supercar I invested in and I lost up to 100% of my money?

How would I cope if no profitable offers were received for the supercar after the three year period, other investors voted against selling at a loss, and there was no secondary market for my share, meaning that my money was locked into the investment indefinitely?

Do I have a diversified portfolio with so much invested in assets with a positive expectation of return (such as equities, commercial property and fixed interest securities) that it makes sense to invest money in depreciating assets with no yield?

Investors should not be seduced by the glamour of “owning” a supercar. As they will never be allowed to drive their investment, they should view it as dispassionately as any other piece of paper they might invest in.

Grove Developments offers unregulated corporate bonds paying 10.9% for a 1 year term (rolled up and paid out), 10.3%pa for a 2 year term (income paid twice yearly) or 10.9%pa compounded for a 4 year term (interest rolled up and paid out at the end of 4 years).

Grove’s literature describes the first option as 10.9% per annum but under “Returns to Investors Explained” it shows investors who invest £5,000 as receiving £6,090 on maturity, £10,000 as receiving £12,180, and so on all the way down the table. This of course equates to a 21.8% return over the year.

It can safely be assumed that the table is wrong and that a 10.9% return is being offered, given that the investment literature repeatedly refers to the return as 10.9%, and that there would be no reason to invest in Grove’s other two options if the first one paid double the interest.

The third option is described as 12.8% per annum but this turns out to mean simple interest, with the table of returns – assuming that it’s accurate – showing a total return on investment of £15,120 for a £10,000 investment. As interest is only paid out on maturity, this works out as a 10.89% per annum return on a Compound Annual Growth Rate basis.

It is unclear why investors would want to invest in the third option when they could receive the same annual return with more flexibility by investing in the one year bond and reinvesting at the end of each year.

Status

Open to new investment.

Who are Grove Developments?

Grove Developments Limited (the literature refers to Grove Developments plc, but no such company appears to exist) was incorporated in December 2010 as a property development company.

According to its latest Companies House filings, Grove Developments Limited is 100% owned by AMSL Investments Limited, a Jersey-based offshore company. Grove Developments is part of the Arora Group of companies, a trading name of Arora Holdings Limited.

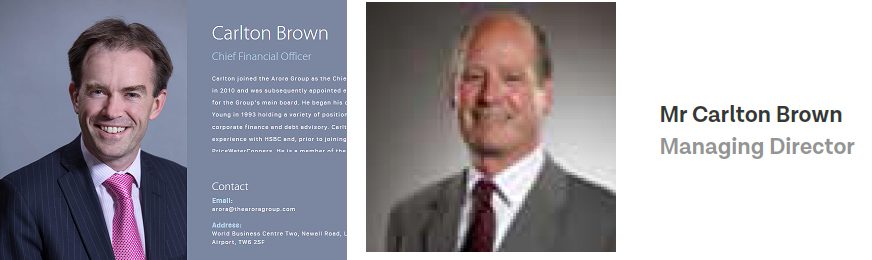

The managing director according to the literature is Carlton Brown. The accompanying photo for Carlton Brown appears to be of a completely different person to the one shown on the Arora Group website.

Left: From http://www.thearoragroup.com/about/people. Right: From Grove Developments investment literature. The poor quality of the image on the right is as per the original.

The other directors according to Companies House are (job titles taken from thearoragroup.com): Surinder Arora (Arora Group founder and chairman), Sinead Hughes (Grove Developments Director) and Athos Yiannis (Arora Group Tax Director / Company Secretary).

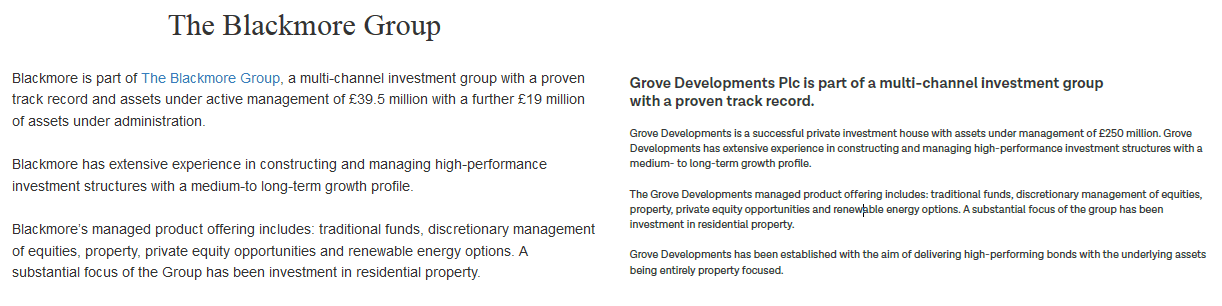

Parts of the literature for this investment appears to have been copy-and-pasted from the website for Blackmore Group, an unrelated company.

Left: https://www.blackmorebonds.co.uk/about-us. Right: Grove Developments investment literature.

The text that Grove Developments has copied from Blackmore and adopted for themselves makes very little sense in this context, in particular “The Grove Developments managed product offering includes: traditional funds, discretionary management of equities, property, prviate equity opportunities and renewable energy options”.

There is no mention of operating investment funds or discretionary management on thearoragroup.com or grove-fund.co.uk, which describe Grove Developments as a property development business. Furthermore such activities would require authorisation from the Financial Conduct Authority. Grove Developments does not appear on the FCA Register or claim any other regulatory authorisation for fund management or discretionary management.

Grove Developments appears therefore to have copy and pasted text from Blackmore Group despite the fact that it is a largely inaccurate description of their business.

How secure is the investment?

These investments are unregulated corporate loans and if Grove Developments defaults you risk losing up to 100% of your money.

The purpose of the loan is to allow Grove Developments to buy properties at under market value and sell them at a profit.

If Grove Developments fails to make sufficient profits from its property developments, or for any other reason Grove Developments has insufficient money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Investors’ money is secured on “all land and property assets owned by Grove Developments”.

Before relying on this security, it is essential that investors undertake professional due diligence to ensure that in the event of a default, these securities are valuable and liquid enough to raise sufficient money to compensate investors, as well as any other creditors that Grove Developments has borrowed money from.

Investors should not assume that because the loans are asset-backed, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed loans have been known to lose 100% of their money when it turned out that the collateral was insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Grove Developments, only illustrating the risk that exists with unregulated corporate loan notes even when they are asset-backed.

Grove Developments claims that “multi-layered security reduces risk to an absolute minimum”. There is very little mention of default risk in its investment literature, even under “How secure is my investment?” in its “FAQ” section.

Under this FAQ there is however the curious statement “Your investment is secured by a legal charge over the assets of the Company and in addition, by the Capital Guarentee [sic] Scheme, which works like an insurance policy, paying out up to £250,000 per investor.” There is no previous mention of this Capital Guarantee scheme in the literature, how it works or where this £250,000 comes from.

There is a strong possibility that this statement is another copy-and-paste, possibly from Asset Life plc (another provider of unregulated corporate bonds), which does feature a £250,000 “capital guarantee” scheme.

Unlike with the Blackmore copy-and-paste, I have not been able to find the original text, so cannot say definitively that this is another copy-and-paste. However, I cannot think of another explanation for why this “Capital Guarantee” scheme does not feature anywhere else in the literature or have any details on how it works.

Should I invest with Grove Developments?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 10.9% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Grove Developments’ bonds are higher risk than a diversified portfolio of mainstream stockmarket funds.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees and any other borrowers are paid.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for an investment with the “absolute minimum of risk”, you should not invest in unregulated products with a risk of 100% capital loss.

Furthermore, even for high-net-worth and sophisticated investors, the numerous inaccuracies in Grove Developments’ literature, specifically regarding 1) its name 2) the identity of its managing director 3) its business activities 4) the existence or otherwise of a £250,000 “Capital Guarantee” scheme 5) the returns on the “Option One” bond, may be of concern.

Delta Capital Markets was an unregulated firm offering binary options to UK investors.

While the firm was active, a number of complaints were made by disgruntled investors on Moneysavingexpert.com and Trustpilot complaining of losing money on trades (which is to be expected with binary options) and being unable to withdraw the money they hadn’t yet lost (which isn’t).

The website has now been offline for several days, and forum users report that they are unable to contact Delta Capital Markets via phone.

It appears that the owners of Delta Capital Markets have disappeared with any remaining money.

Who were Delta Capital Markets?

No information was provided on Delta Capital Markets’ website as to who were behind the business. According to a disclaimer, Delta was a trading name of Annax Global Ltd registered at Ajeltake Road, Ajeltake Island, Majuro, Marshall Islands, MH96960. The identity of the owners of this company remains unknown.

The UK registered address of Delta Capital Markets was a virtual office.

The website deltacapitalmarkets.com was registered by an Alan Curran of Axium Corporate. Axium Corporate Limited was a UK company that was dissolved voluntarily in December 2017, just under two and a half years after it incorporated in August 2015. It never filed accounts as an active company. Alan Curran resigned as sole director in August 2017 at the age of 85 and was replaced by another. Whether Curran was involved with the running of Delta Capital Markets or only registered the website on their behalf is unknown.

Can I get my money back?

Delta Capital Markets was not regulated by the Financial Conduct Authority. If you were advised to invest with Delta Capital Markets by an FCA-regulated adviser, you may have a claim against them – but that appears to be unlikely.

In the absence of any regulated claim, recovering the money appears to be highly unlikely.

Investors should beware of “fraud recovery fraud” where someone claims they can recover your investment if you pay “legal fees” or “liquidation fees” or other upfront fees. If someone contacts you claiming they can get the money back, it is almost certainly a scam. If you want to pursue a claim via the courts, use a reputable solicitor of your own choice. Bear in mind there is no point throwing good money after bad by paying legal fees to pursue money that cannot realistically be recovered.

Delta Capital Markets investors should be aware that they are now probably on a “suckers list” and therefore highly likely to receive calls attempting to subject them to fraud recovery fraud or other scams.

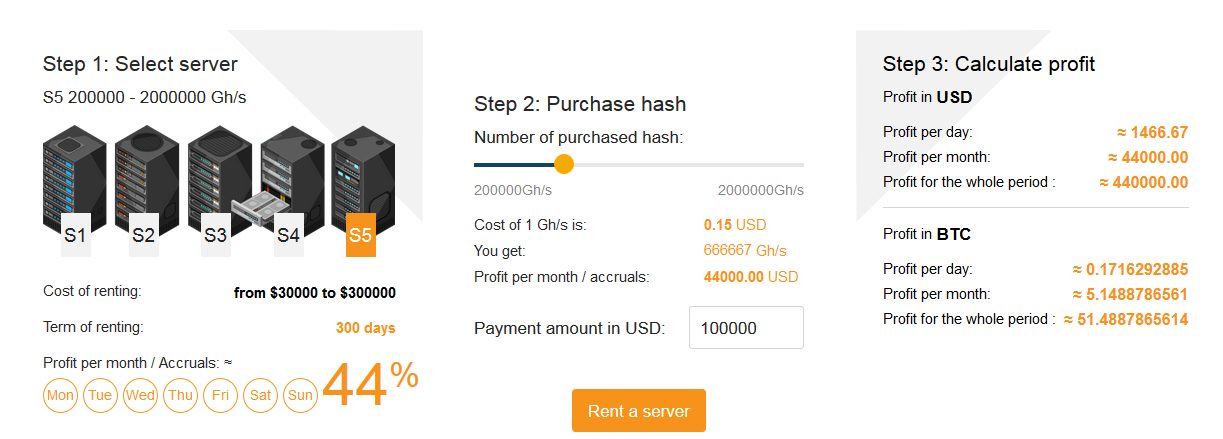

World Mining offers unregulated securities purporting to represent the rental of cryptocurrency mining servers, with investors “purchasing hash” (investing money in mining computers) and receiving returns of up to 44% per month simple interest for a term of up to 360 days.

There are five servers which pay returns as follows, with larger investment amounts being generally eligible for servers paying higher returns (although bizarrely, S3 has the highest annualised return despite having the shortest investment term and the third highest minimum subscription). Despite World Mining supposedly being a British company (more on that later), returns are quoted in US dollars and Bitcoins.

S1 – $15 to $2,025 – 360% profit after 360 days (390%pa)

S2 – $150 to $7,500 – 396% profit after 360 days (428%pa)

S3 – $900 to $15,000 – 336% profit after 280 days (1,174%pa)

S4 – $4500 to $150,000 – 377% profit after 290 days (1,129%pa)

S5 – $30,000 to $300,000 – 440% profit after 300 days (1,126%pa)

Who are World Mining?

World Mining Limited has one shareholder and director, Philip Johnson. World Mining Limited was incorporated in October 2017 and consequently is yet to file accounts.

In December 2017 World Mining’s website credited Philip Johnson as CEO, and also included a range of fake biographies using stock images, as revealed by BehindMLM.com. The management page has since apparently been overhauled – Philip Johnson’s name now does not appear anywhere in the management page, and the stock images have been replaced.

The new management page now does not state who is the CEO. Presumably it is still Philip Johnson. Whether any of the new images now represent real employees is unknown.

Should I invest with World Mining?

World Mining claims to offer returns of over 1,000% per annum at a time when the UK base rate is 0.5% and mainstream stockmarket-linked investments generally use 5% per annum as a medium rate of projected return.

The company claims that it generates its returns from cryptocurrency mining, however the returns from cryptocurrency mining are far less than they were in Bitcoin’s early years due to people entering the market with more and more powerful computers.

If anyone was able to legitimately generate returns of over 1,000% per annum from cryptocurrency mining, others would enter the market and dilute World Mining’s returns well before the 280-360 day period was up.

World Mining provides no independently audited accounts or other evidence that they are able to consistently generate returns of over 1,000% per annum.

The reality is that the only way to consistently generate returns of over 1,000% per annum is to pay existing investors using new investors’ money. Using new investors’ money to pay existing investors makes World Mining a Ponzi scheme.

As with all Ponzi schemes, when new investors’ money dries up the scheme will collapse. The administrators of the scheme will make money, along with affiliates who earned commissions from persuading others to invest, and possibly a few early entrants. Everyone else will lose money.

World Mining’s website, with its offer of returns over 1,000% per annum and invitation to subscribe money via its “Registration” button, clearly represents an inducement to invest and is therefore a financial promotion. Offering a financial promotion in the UK requires authorisation from the Financial Conduct Authority.

A search of the FCA Register shows that World Mining is not authorised to offer financial promotions in the UK (a “World Mining Fund” is clearly unrelated, given it was registered 14 years before World Mining Ltd existed), and World Mining does not claim any authorisation for its financial promotion on its website. World Mining is therefore committing a criminal offence under the Financial Services and Markets Act.

Christianson Property Capital offers unregulated loan notes paying 10% per annum over ten years, which is compounded and paid on maturity.

Investors have a “break clause” that allows them to withdraw 50% of their investment after 5 years.

Status

Believed to be open to new investment. The “invest” section of its website states “For more information download pdf coming soon”, but an investment brochure is still available to download from its website, and we will assume the information in this brochure stands until we learn otherwise.

The investment brochure is available to download from the website without any requirement to be a high net worth or sophisticated investor or professional intermediary.

Who are Christianson Property Capital?

No information is provided on the website or in the investment literature as to who is behind the business.

Companies House shows that Manish Gambhir is the sole owner and director of Christianson Property Capital Limited.

Christianson Property Capital was incorporated three months later in May 2014. According to its last accounts (April 2016), the company had £1.1 million in net liabilities. This mostly comprised ~£7 million in amounts owed by related companies, minus ~£8 million in liabilities represented by loan notes such as those reviewed here.

The “related companies” appear to consist of a subsidiary, Victory House Group Ltd, which in turn owns another subsidiary, Victory House 1 Ltd. Two other subsidiaries (Victory House 2 and 3) are described in the April 2016 accounts as dormant.

How secure is the investment?

These investments are unregulated corporate loans and if Christianson Property Capital defaults you risk losing up to 100% of your money.

Christianson Property Capital “focuses on the acquisition, trading and development of property in the UK”.

If Christianson fails to generate sufficient returns from its properties, there is a risk that Christianson may default on payments of interest and capital to investors.

Investors’ money is secured on the real estate assets of the company.

Before relying on this security, it is essential that investors undertake professional due diligence to ensure that in the event of a default, that these securities are valuable and liquid enough to raise sufficient money to compensate investors if needed, as well as any other creditors that Christianson has borrowed money from, and that their security over these assets is watertight.

Investors should not assume that because the loans are asset-backed, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed loans have been known to lose 100% of their money when it turned out that the collateral was insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Christianson Property Capital, only illustrating the risk that exists with unregulated corporate loan notes even when they are asset-backed.

Christianson Property Capital’s literature states in the risk warning at the end that investors are not covered by the Financial Services Compensation Scheme.

Should I invest with Christianson Property Capital?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering 10% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Christianson Property Capital’s loan notes are higher risk than a diversified portfolio of stockmarket funds.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that a) the security exists b) in the event of default, the security could be easily sold and would raise enough money to compensate all the investors and other borrowers, after the adminstrator deducts their fees.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for “security” or “assured returns”, you should not invest in unregulated products with a risk of 100% capital loss.

Under UK law and regulations, unregulated corporate loan notes should only be offered to high-net-worth or sophisticated investors. (In the regulatory jargon, they are considered non-mainstream pooled investments, being debentures issued by “special purpose vehicles”, an issuer whose objects and purposes are primarily the issue of securities.)

“Sophisticated” does not mean “clever”. It has a specific definition, meaning a member of an angel investment network, a previous investor in unlisted companies, a private equity professional, or a director of a company with a turnover over £1 million.

Leaving the regulations aside, it is a basic principle that inexperienced investors should not be investing significant amounts of their capital in an investment which has a material risk of total and permanent loss.

Many unregulated firms are currently very keen to promote their high ratings on Trustpilot. Often they display 5-star Trustpilot icons on the home page of their website.

Typical Trustpilot link on the website of an unregulated issuer

When reading the reviews left on Trustpilot for the issuers of unregulated loan notes, it is clear just how many are highly unlikely to be sophisticated or high-net-worth investors.

In an unscientific survey, I have read through around 300 reviews left for one particular issuer and counted those which showed strong evidence that the reviewer was neither a high net worth investor or sophisticated investor.

I marked a review as definitely unsophisticated if it stated explicitly that they did not have much experience of investing, appeared to believe they had invested in a deposit account or that the investment was otherwise capital protected, used very broken English, or were under the impression that they had been given advice by the issuer (which they are not authorised to do).

I marked a review as possibly unsophisticated if they seemed to place excessive importance on customer service and the friendliness of the customer representatives, or on receiving their first interest payments promptly.

How efficient and customer-friendly an investment company is should really be of very little interest to a high-net-worth or sophisticated investor. Many of them will be using intermediaries or assistants to deal with their investments on their behalf. Even if they are managing their investments personally, they only have to deal with the company twice over a period of several years – at the beginning, and when they withdraw their money.

Many of these firms have been in operation for less than five years and the fact that they have so far dealt promptly with applications and made interest payments on time is of very little significance.

I found that out of 300 reviews, 32 displayed definite evidence of being from an unsophisticated investor, and a further 40 were possibly unsophisticated.

Most of the reviews were too short to draw any conclusions from.

72 out of 300 may be a minority, but it is a very high amount given the unsuitability of these investments for retail investors. It is likely to represent several millions of pounds worth of life savings at risk. Only 7 reviews showed clear awareness that their capital was at risk.

Not a real review, but a mockup of a typical Trustpilot review for an unsophisticated bond. Names and the text have been changed to protect the unsophisticated.

Two Trustpilot reviewers even left reviews to say that they were not happy about being repeatedly asked by the issuer to leave a review on Trustpilot when they had only been invested for a week.

I have not named the company for two reasons. Firstly, because this survey is inherently subjective. Secondly, because of the possibility that the company’s bonds were sold by unrelated third parties and the issuer itself is blameless for any particular review.

To make it a bit more scientific, I looked up the Trustpilot page for a regulated firm, Octopus Investments, which also invests in asset-backed lending and property finance, but offers its products almost entirely via regulated financial advisers. In statistics, this is known as a “control group”. It had no reviews whatsoever on Trustpilot.

I tried two of its larger rivals, TIME Investments and Foresight Group: they also had no reviews on Trustpilot. So from my control group I draw the conclusion that firms that do not offer their products to retail investors do not get reviewed on Trustpilot, even if they have been around for many years with a good track record.

Conclusion

This is a highly unscientific survey and does not constitute evidence that any individual investor should not have taken out an unregulated corporate loan note.

And there is no reason whatsoever to believe that the 72 people who are or may possibly have invested without understanding the risks will not in due course receive their original capital on time and be perfectly satisfied.

UCG Trust describe themselves as “an investment marketplace that connects capital investors with borrowers from all over the world of non-bank lenders. It is a new alternative to the traditional banking system.”

The company offers unregulated loan notes paying annual income as follows:

US dollars: 9.5% over 1 year, 10.75% over 2 years and 12% over 3 years

Euros: 9.25% over 1 year, 10.5% over 2 years and 11.75% over 3 years

Pounds sterling: 9% over 1 year, 10.25% over 2 years and 11.5% over 3 years

If the investor is recommended by a friend, they receive an additional 1.5% APR return, so the maximum return offered is 13.5%pa.

Commissions

UCG Trust pays a commission of 1% of the amount invested to anyone who recommends another investor. The recommended investor also receives an additional 1.5% return.

Who are UCG Trust?

There is no information on UCG Trust’s website as to who is behind the business.

The “small print” at the bottom of the website says that UCG Trust is the trading name of UCG Marketplace Ltd, registered at 1000 N West Street, Wilmington, Delaware. There is no company by that name registered with the State of Delaware.

There is however a UCG Marketplace Ltd in the UK which was incorporated in July 2017 with one director and shareholder, Daniel O’Donoghue. The company is registered to “Suite 13069 43 Bedford Street, London, United Kingdom, WC2E 9HA”, which is a branch of Mail Boxes Etc. Whether this is related to UCG Trust is unclear.

The UCGTrust.com website was registered on 18th January 2016.

Is UCG Trust safe?

These are unregulated investments and should UCG Trust default, investors risk losing up to 100% of their money.

UCG Trust states that they “provide lending to small businesses fully online combining 5 lending platforms in United Kingdom, Czech Republic, Slovakia, Malaysia and India”.

If UCG Trust fail to make sufficient returns from their lending to small businesses, there is a risk that they default on their bonds.

UCG Trust however claims in various pages on its website that “All the risks of investing in lending secured by the company under AASA” (I have been unable to find out what this acronym means), “Forget about loses of your investment and start joining thousands of investors earning solid returns with the simple investment process” and under its FAQs “How is my money protected? – All investments are secured by the company. It means that all defaulted loans will be covered by the profit of UCG TRUST.”

UCG Trust cannot make any profits if its obligations to investors exceed the money it makes from its borrowers. The cost of borrowing is deducted before you calculate your profit.

Perhaps this refers to retained profits from previous surpluses of funds received from borrowers, after making repayments to investors. But UCG Trust cannot possibly have much in the way of retained profits when it has only been in business for two years at most.

If UCG Trust does have sufficient funds to guarantee payments to investors, why solicit investment in the first place? Why not loan those funds out to small businesses, and take all of the profit, without paying out up to 13.5% to investors?

Despite UCG Trust’s exhortation to “forget about loses”, if UCG Trust receives insufficient money from borrowers and has insufficient retained profits to meet obligations to investors, investors risk losing up to 100% of their money.

Offering unregulated securities in the US and unauthorised financial promotions in the UK

UCG Trust, which claims to be based in Delaware, USA, with its offering of loan notes paying up to 13.5% in US Dollars, clearly represent a securities offering to US investors. Offering securities in the US requires authorisation from the USA’s Securities and Exchange Commission.

UCG Trust’s website also clearly represents a financial promotion to UK investors by inducing them to engage in investment activity by investing in its sterling loan notes. Both P2P lending and offering financial promotions to UK investors requires authorisation from the UK’s Financial Conduct Authority.

A search on both the SEC’s and the FCA’s registers for UCG or United Capital Group returned no results.

The only regulatory authorisation UCG claims is “All activities of UCG TRUST within EEA are maintained and supported by the United Capital Group, authorised and regulated company by the Commission de Surveillance du Secteur Financier (CSSF)”. A search for UCG or United Capital Group on the CSSF’s register again returned no results.

UCG Trust is committing criminal offences in both the United States and United Kingdom by offering unregistered securities / P2P lending and unauthorised financial promotions respectively.

Should I invest with UCG Trust?

This blog does not provide financial advice. The following are statements of fact based on publicly available information, or near-universally accepted investment principles; they are not personalised recommendations. Investors should consult a regulated independent financial adviser if they are in any doubt.

Despite UCG Trust’s claim to be risk-free, there is clearly a significant risk of capital loss should its loans to small businesses fail to pay sufficient returns to meet its obligations to investors.

Furthermore, the firm is offering unregistered securities in the United States, and offering a P2P lending platform and unauthorised financial promotions in the United Kingdom. Offering unregistered securities in the United States and carrying on a regulated activity without authorisation in the United Kingdom are criminal offences in both countries.

Do not invest unless you are prepared to risk 100% losses.

On 30th January we reviewed the investment firm Braxton Knight and concluded that its offer of unregulated securities paying a fixed return of up to 80% per annum with “capital risk less than 5%” constituted a Ponzi scheme, and also that the firm was offering both financial promotions and financial advice without authorisation.

The day after we went to press, the Financial Conduct Authority issued a warning against investing in Braxton Knight, and Braxton Knight now appears on the FCA Register as an unauthorised firm, with a note that the FCA “strongly suggest you avoid dealing with unauthorised firms like this”.

Carrying on a regulated activity without advice is punishable by a sentence of up to two years’ in prison and/or a fine. Operating a Ponzi scheme is fraud, which carries further penalties. The FCA has not disclosed whether any criminal investigations are ongoing, but we would not expect them to.