Wellesley has become the latest minibond issuer to default on investors. Income payments were suspended last week and the company announced on Tuesday that it would attempt to persuade investors to approve a Company Voluntary Arrangement.

According to The Times, investors in property-backed minibonds are facing a write-off of 22% or more, while investors in non-property minibonds face total losses.

An early indication of problems at Wellesley Finance came in January 2020 when their auditors cast material doubt over whether the company could continue as a going concern.

I’ve been asked more than once why Wellesley was never reviewed here. The answer is that by the time Bond Review was launched in December 2017, the company had mostly cleaned up its act as far as its adverts were concerned, and (unlike the likes of London Capital and Finance) made it pretty clear that investors were investing in loans to a company and capital was at risk. I don’t write a review just to tell investors what the company has already told them.

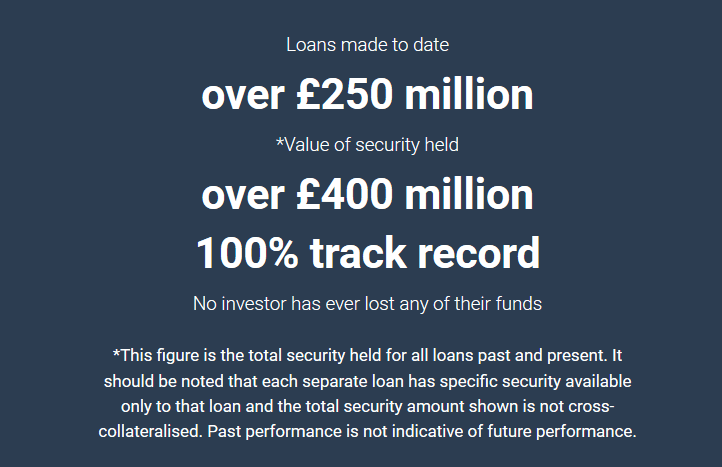

Historic Wellesley advertising contained a number of familiar tropes that have since been identified as misleading by the regulator.

Regardless of the extent to which Wellesley investors can be blamed for investing in an inherently high-risk investment, the collapse of Wellesley is another blow to the concept of advertising high-risk unregulated and pseudo-regulated investment securities directly to ordinary retail investors.