Krono Partners launched in 2013 and offered unregulated seven-year bonds paying interest of 8% per year, supposedly from investing in distressed real estate in the United States and Europe. It then offered another series of bonds which would supposedly be used to invest in SME bridging loans.

The company went into administration in March 2018, supposedly as a result of bank accounts operated by Jade State Wealth being frozen.

This, it has since become clear, was only the tip of Krono’s problems. Krono holds neither distressed real estate nor bridging loans. Instead over three quarters of its assets (according to the Statement of Affairs) consist of an investment registered in the Cayman Islands known as “Company X” which raises corporate finance via Exchange Traded Notes.

Throughout the period of administration, none of Krono’s investments have paid any returns which could have been used to pay investors’ returns of 8-10% per year, even if it hadn’t gone into administration.

Company X is now Company Y

Hopes of investors getting any of their money back rest largely on Company X paying commission from its fundraising to Krono, in return for the money Krono invested in it. When Smith & Williamson were appointed as administrators, Krono management claimed that investors could expect repayment in full.

The administrators have now revealed that Company X can’t actually pay any commission to Krono because of regulations in the Cayman Islands. Whoops.

Thankfully, a way around this has been found which involves a new Company Y being set up in Hong Kong, and has seemingly replaced Company X.

No commissions have yet been received from Company Y either. The administrators list five “key projects” being undertaken by Company Y which are at various stages of fundraising; none have yet reached the stage where they pay Krono (and in due course their investors) any money.

Other than cash in the bank, Krono’s other assets consist of relatively small amounts in shares and micro loans, which are also yet to return anything. A “Company B” in which Krono owns 4 million shares is due to list on the Canadian Stock Exchange by 31 December 2019.

The biggest payment the administrators have received so far is in question. £85,000 was received under “other debtors” which were “relating to the sale of an equity interest”. Subsequently the administrators were paid another £16,649. The unnamed payer is now claiming that only the £16,649 was due and the £85,000 should not have been paid.

The £85,000 / £101,000 is by far the biggest realisation made to date (the only other being £42k in a trading account and cash in the bank) so it will be a blow if it turns out that most of it has to be handed back. Total receipts in the administration to date currently stand at £143k, while the administrators’ costs so far stand at £154k.

The Financial Conduct Authority reviewed Krono Partners in 2014, shortly after launch. After four months it closed its case and took no further action.

Krono is one of a number of failed unregulated investments currently in administration with Smith & Williamson, alongside London Capital & Finance and Park First.

A meeting of victims in the collapsed Park First investment scheme to approve the administrators’ proposals has been adjourned to 25 November, after a proposal to appoint alternative administrators was not included on the agenda.

Smith & Williamson (also administering Reyker Securities and London Capital and Finance) were the choice of Park First’s directors.

US-based Safe or Scam LLC has proposed an alternative administrator, Quantuma LLP (currently attempting to gain control of collapsed care home investment scheme Carlauren Group).

Safe or Scam characterise Smith & Williamson’s proposals as amounting to the write off of £115m of debt owed by Park First group companies to the companies in administration.

The administrator’s report confirms that the four Park First companies involved in the CVAs are owed a total of £115.4m by other companies in the Park First group, but that this £115.4m “has no recoverable value”.

They are actually saying that these four Park First companies transferred £115.4m to other group companies and there is no chance of recovering that money for the investors ! There has been no explanation why this money was transferred nor any explanation as to why is cannot be recovered. The administrators are just expecting creditors to accept a loss of that magnitude because they tell them to. So….. if creditors vote FOR the CVA proposals what effect would this have ? Well, if they vote FOR the proposals they would be agreeing to the following:

To write off £115.4m where the administrator has not even told them which companies took the money, why they were paid the money and why it is not possible to recover it; and

To sign away their rights to be able to take any form of recovery action against any of the parties involved; and

To allow the existing management to continue to run the businesses without any investigation into their conduct or the possible misappropriation of funds.

I asked S&W for comment on whether this was an accurate description of their proposals a week ago, and have not received a reply.

In a subsequent blog post on Saturday 12th October, Safe or Scam accused S&W of misinforming creditors by implying that a proposed £33m cash injection from Group First companies was contingent on Smith & Williamson’s proposals (including the £115m debt write off) being accepted, and the company entering a Company Voluntary Arrangement.

In short: either take £33m or risk getting nothing.

According to SOS, this was “erroneous”; the FCA has confirmed to rival suitors Quantuma LLP that the £33m should still be available to a liquidator, whether the original proposals are accepted or not.

The meeting of creditors has been rescheduled for the 25th at City Temple Conference Centre, London.

Comment

The rescheduled meeting sets up an intriguing clash for the fate of the administration between the Park First directors’ chosen administrators and Safe or Scam’s.

The parallel between London Capital & Finance and Park First goes beyond the fact that the unrelated collapses of both are being cleaned up by Smith & Williamson.

In both cases Smith & Williamson were appointed by the directors of the unregulated investment schemes themselves.

There is of course no suggestion that S&W are failing to carry out their statutory duties to act in the interests of creditors, over the people who appointed them if necessary.

There is also no question that the first job of an administrator of a collapsed unregulated investment scheme is to win the trust of creditors – and this goes double when the administrators were appointed by the people who lost their money in the first place.

Smith & Williamson’s appointment to London Capital & Finance was followed by a series of gaffes, which included unquestionably parroting the idea that LCF investors were sophisticated and high-net-worth (which very quickly turned out to be false), and saying on national radio that it was a good thing that LCF invested in a handful of companies linked to the directors, rather than hundreds of SMEs as investors had been led to believe, because it made the administrators’ job easier.

(Which is true, but the kind of thing you should look over your shoulder before saying if you’re at the Friday night office social, and is a downright stupid thing to say on national radio in front of stricken investors.)

S&W also claimed in the same interview that “the numbers all add up” and suggested investors could hope to get their money back; only to later reveal that what the numbers added up to was 80% losses as a best case scenario.

All that has however been left in the past, and there was no serious attempt to replace S&W with completely independent administrators of LCF investors’ own choice. Nor has there been any suggestion that S&W hasn’t maximised recoveries so far.

By contast, in the case of Park First Safe or Scam are accusing Smith & Williamson of being far too quick to effectively write off £115m of intercompany loans by proposing a Company Voluntary Arrangement.

Whichever choice the investors make, no-one can deny that more scrutiny over where the money went and whether it can be recovered is sorely needed.

Park First investors sue Park First and its directors for “fraudulent misrepresentation”

In other Park First news, a group of Park First investors are suing both Park First itself and Park First owner Toby Whittaker personally, alongside others including Park First director Ruth Almond, the Evening Standard reveals.

The investors are seeking £6 million which suggests that they represent a relatively small percentage of Park First investors.

A key part of the scheme was that the Park companies would sub-lease the plots back from the investors, offering a guaranteed return of 8%. The company said “projected returns” would rise to 10% in years three and four and 12% in the two following years.

In fact, the claim says, the sub-leases only lasted for two years, after which Park broke them and failed to provide subsequent services, leaving the plots impossible to sell. The investors also claim Whittaker’s companies misled them that they would easily be able to sell their spaces if they wanted to. There was no secondary market to buy them, which Whittaker knew, the case alleges.

The claim says some of the car parks in Glasgow were fenced off, making it impossible for them to return the kinds of profits being promised.

Park First director Ruth Almond said “The action will continue to be defended. We believe investors would be better served by pursuing options set out by the administrators.” That would be the option which apparently involves writing off most of the liability owed by Park First discussed above, then.

In general it takes exceptional circumstances for directors to be held personally liable for the failings of their companies; limited liability companies are called that as a reason.

Whether such circumstances exist remains to be proved in court.

Sadly, people investing lots of money in obscure micro-cap unregulated investments and losing all their money is not in itself an exceptional circumstance.

The FCA’s action alleges that Park First was an illegal collective investment scheme, which we already knew as that was why it was originally shut down in late 2017 (not 2016 as the Standard says).

More seriously, the FCA alleges that Park First’s directors claimed the parking spaces were being sold at a 25% discount, based on independent valuations, but were “aware that the valuations were based on unrealistic returns”.

The FCA is suing Park First owner Toby Whittaker, director John Slater, Park First and numerous other connected firms, demanding the defendants repay a “just sum” to be distributed to victims.

The FCA has justified its lack of previous action, which allowed Park First to remain in control of the scheme’s assets, and its attempts to return the money to Park First investors, on the basis that if it had wound up the companies earlier, it might have made it less likely that investors got their money back.

Whether leaving Park First and its directors in overall charge of the money for another one-and-a-half years succeeded in increasing recoveries for investors remains to be seen.

In the original settlement in late 2017, the FCA secured a “promise” from Park First not to dispose of their assets, and ringfenced the sale proceeds of a car park at Luton Airport plus a further £1 million – £33m in total – to meet buyback payments for investors. This is the payment at the centre of the dispute above.

Fluid is offering IFISA bonds and unregulated bonds paying 6% per year for a three year term.

Funds raised are to be used to invest in short-term bridging loans.

Who are Fluid?

Ansar Mahmood, Fluid Managing Director and owner

Fluid is currently raising funds in its subsidiary Fluid ISA Bond 2 Limited, within an ISA wrapper provided by Goji Financial Services. Previously it was raising funds via Fluid ISA Bond, with the ISA wrapper provided by Northern Provident Financial. Both companies will lend on the funds to Fluid Lending Limited.

The ultimate holding company is Fluid Trust plc which is owned 100% by Fluid’s Managing Director, Ansar Mahmood. According to the brochure, Mahmood has entered the bridging loans industry after 15 years as a chartered accountant.

How safe is the investment?

Fluid’s brochure makes much of the fact that its bridging loans are secured on property.

However, investors are not investing directly in secured loans, but in loans to Fluid Lending Limited, which in turn uses the money for secured loans. These loans to Fluid Lending Limited are not secured (there is no indication that they are in the investment literature, and Companies House shows no charges against Fluid Lending Limited at time of writing).

In any case, secured lending on property is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Fluid, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not Fluid) to confirm that in the event of a default, the assets of Fluid would be valuable and liquid enough to compensate all investors. Investors should not simply rely on what Fluid tells them about their assets.

Customer service

I don’t usually dwell on standards of customer services because it’s virtually irrelevant. The only time someone investing in a three year bond should need to deal with customer services is when they hand the money over and when they get paid back.

There is no other reason to contact them, unless they’ve changed their address or other details, or something’s gone wrong.

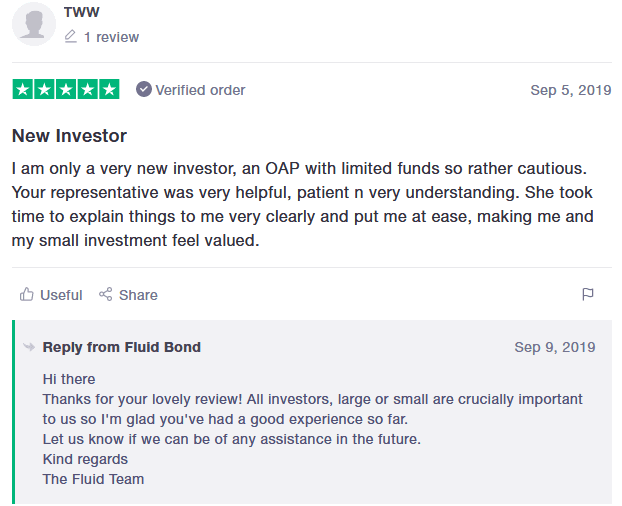

Nonetheless it is worth noting that Fluid pays particular attention to customer service. It has 55 reviews on Trustpilot and in almost every case, the company has taken time to personally reply to the review.

I will leave aside the question of whether “an OAP with limited funds” with a cautious attitude to risk should be investing in an inherently high risk loan to a single company, as I’m not in a position to second-guess their investment decision.

Given the emphasis Fluid places on customer service, it is worth emphasing that customer service has absolutely nothing to do with the likelihood of a company successfully repaying its debts. No investor in Fluid has yet reached the three-year maturity date so reviews say absolutely nothing about the likelihood of Fluid repaying the money on maturity.

Should I invest in Fluid?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted startup company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

As an individual, illiquid security with a risk of total and permanent loss, Fluid’s loan notes are much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “secure” investment, you should not invest in corporate loans with a risk of 100% loss.

Asset manager Reyker Securities has been placed into special administration.

Reyker was mostly known as a stockbroker and Discretionary Fund Manager, but part of its business involved approving promotional literature and providing an ISA wrapper to two investments reviewed here: Blueprint Bond and Astute Capital.

Both Blueprint and Astute Capital remain in business and should in theory be largely unaffected by Reyker’s collapse, as the ISA status of investors’ funds should remain valid despite the administration.

They will however be unable to raise further money via Reyker ISAs.

Reyker Securities ran out of money after a failed attempt to sell the business, plus unspecified “legal actions being faced by the company” and the downturn in the structured product market.

Last month it was revealed that the Financial Services Compensation Scheme has compensated investors in Providence Bonds and Secured Energy Bonds in full (up to £50,000), paying out a total of £10 million (£5 million for each).

Providence and Secured Energy Bonds paid interest of 8.25% and 6.5% per year. Both collapsed with total losses to investors.

Investors brought Financial Ombudsman claims against Independent Portfolio Managers, who approved the schemes’ literature, enabling the investments to be promoted to retail investors. These complaints were initially rejected on the basis that they were not customers of Independent Portfolio Managers, Providence / SEB was.

The investors took legal advice, and before the matter went to court, the FOS changed its mind and began looking into complaints against IPM. An Ombudsman found against IPM in three published cases. IPM went bust shortly after, over an unpaid regulatory fee.

Those FOS decisions against IPM allowed the investors to claim on the FSCS.

Last year I poured cold water on the hope that investors would be compensated, saying that if the FSCS did so, it would effectively make all unregulated investments risk-free, provided the investment wasn’t too lazy to jump through the hope of finding an FCA-regulated company – any FCA- regulated company – to approve its literature.

Naturally I am delighted for the investors that I have been proved wrong. And in fairness, I was in good company. The FOS also initially rejected investors’ complaints. And back when Secured Energy Bonds and Providence Bonds were being promoted to investors, nobody told them that the investments were in fact 100% risk-free (up to £50,000) by virtue of the fact that the literature was misleading and approved by the investment’s Corporate Director.

(undermisselling (n.) – The act of an FCA-regulated company selling a supposedly guaranteed investment that is too good to be true, and by thus misselling it, making it actually true, but not making it clear that it is too too good to be true to not be true.)

I have previously asked: if investors are compensated on the basis that IPM was personally liable to them for misleading literature, does this mean any investment with Section-21-approved misleading literature is risk-free?

Independent Portfolio Managers was specifically sanctioned by the FOS for promoting security features of the investment (the fact that the bonds were secured loans and the existence of a Security Trustee) without equally prominently highlighting the risks (the fact that secured loans can still lose all your money and the Security Trustee, which was none other than IPM, was as much use as a chocolate fireguard).

The FOS found IPM was liable directly to investors because it not only approved the literature, but acted as Corporate Director and Security Trustee to the bonds.

Part of the reason IPM’s expertise is relevant over and above their ability to review the materials is that it had an ongoing role in the investment scheme, approving new documents as they are created.

The expertise is relevant to IPM’s status as Corporate Director which was a non-contingent role that was promoted as part of the security of the bond. And IPM’s expertise was relevant to its contingent but nevertheless prominently proclaimed status and role as Security Trustee by which it might have to intervene to manage the investor’s asset. IPM was in effect being advertised as a manager of the investor’s assets upon a condition being met: this is an active (albeit contingent) managerial role,to which IPM’s expertise is relevant.

[…] The purpose of IPM’s involvement in the arrangements was to bring about the investment.

I can think of many unregulated bonds with literature approved by an FCA-regulated third party, but none of the top of my head where the same third party acted as Security Trustee or Corporate Director, that are still in business.

The FOS might still find the company that signed off the literature liable for “bringing about the investments” – anything’s possible – but its decisions against IPM are not a precedent.

(I’m using precedent in a general sense – FOS decisions do not set legal precedent in the same way a court case does.)

Good news for payers of FSCS levies that the practice of FCA-regulated companies misselling bonds and also acting as Security Trustee, in doing so making them FSCS-eligible, appears to have ended.

If only the same was true of the practice of FCA-regulated companies misselling unregulated bonds at all.

Lidex Trading claims to provide a “Lidex Trading Multi Asset Fund” paying a fixed dividend of 21% per year, although in their very next paragraph they claim the dividend is 10% a year.

According to a reader, Lidex Trading are cold-calling investors, falsely claiming to be following up a query from the investor.

How safe is the investment?

Lidex Trading claims that it

employs programmatic strategies to guide its asset allocation processes and leverages key strategic partnerships to ensure efficient deployment of capital Lidex Trading [sic] is led by a veteran team of asset management, venture, and technology professionals with decades of collective experience.

It also claims

The Lidex Trading Multi Asset Fund is a 3 year fund that purchases equity in the top 25 private companies and uses computer science to trade on forex, commodities and stocks and shares , providing a fixed dividend of 21% a year from fund liquidity which can be paid monthly, quarterly or per annum to fund members.

In its very next paragraph the return suddenly changes from 21% to 10% a year.

This fund is completely unique and stand alone offering the stability of seeing your capital gain a fixed dividend of 10% a year with the excitement of large cash payments as companies list and grow.

Leaving aside Lidex’s meaningless gibberish, if Lidex Trading was actually running a “Multi Asset Fund” investing in whatever in the UK, this would require registration for the FCA.

Just to remove any ambiguity, Lidex Trading helpfully confirms that is committing a criminal offence, stating in its footer “The investment products marketed by Lidex Trading are regulated by the financial conduct authority. [sic]”

Lidex Trading is not registered with the FCA. Lidex claims to be “FCA registered through our trustee”, Capital Emerging Markets. This however is false as if it was regulated as an “appointed representative”, it would still appear on the FCA register in its own right. This means that Lidex Trading would be committing a criminal offence if it was running a collective fund as it claims.

Lidex’s claim to provide consistent dividends of 21% per year also fails the Ponzi smell test. If Lidex really was able to generate consistent returns of 21% each year, it would keep it to itself, and not dilute its returns by sharing its secret with the market. If it did look for external investment, it would do so very quietly, and not break the law by cold-calling people at random.

Lidex provides no evidence of generating consistent dividends of 21% per year since 2015, because they don’t exist. Any returns paid to investors come from investors’ own money or those of another, making Lidex a Ponzi scheme.

Who are Lidex Trading?

Lidex Trading claims “we have been trading in the UK since 2015” and there is a Lidex Trading Limited on Companies House which was founded that year. However Lidex Trading’s website (lidextrading.co.uk) was only launched in 2019.

In a further example of Lidex Trading’s extreme laziness when it comes to scamming investors, the names of its supposed “Team”, such as CEO “James Wilson”, are completely different to the directors of Lidex Trading Limited on Companies House.

There is a distinct possibility that the Lidex Trading Limited on Companies House is blameless and someone has simply copied their name.

Who Lidex Trading actually are is unknown. No photos are supplied on its “Team” page and “James Wilson” and its other directors probably do not exist. The domain was registered anonymously.

Should I invest with Lidex Trading?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Any investment offering yields of up to 21% should be considered extremely high risk – especially when they can’t even make up their minds as to what the “fixed” yield is.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Is my portfolio big enough that I could lose 100% of my investment and not worry about it?

Most importantly, investors should think long and hard before handing their money to a company that lies about being FCA authorised, is breaking the law by operating an unauthorised collective scheme (even if its Multi Asset Fund exists, which it probably doesn’t), and can’t even keep its story straight from one sentence to the next.

It’s one thing to be scammed and another to be scammed by something so embarrassingly inept.

Do not invest unless you are prepared to lose all your money.

Other variants of the same scam

My research on Lidex led me to two websites which have copied and pasted much of their material from the same place as Lidex.

Specifically IPO-Dex (which claims to be a trading name of Fink Asset Management) and Ashdown Trading.

Both IPO-Dex and Ashdown Trading are also scams in much the same way as Lidex. All share substantially similar marketing material and falsely claim to be appointed representatives of Capital International Emerging Markets Fund (which has nothing to do with them).

There is already an FCA warning about IPO-Dex, while Fink Asset Management is not registered with the FCA, nor is Ashdown Trading. The fact that these companies are blatantly operating illegally, added to their nonsensical claims about non-existent returns, identify all three companies as scams.

As a low-effort, high-churn variety of scam, it is likely that more variants on the same scam will pop up in the coming months until the scammers either get caught (unlikely) or they have fully exhausted the market for their particular spiel (far more likely).

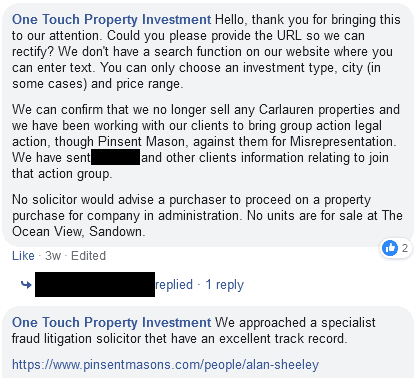

On the public Facebook group Sandown Hub, a resident of Sandown noticed that one of its former introducers, One Touch Property Investment (officially One Touch Solution Ltd), was apparently continuing to sell units in its care home.

One Touch clarified that it was no longer selling Carlauren investments. In the ensuing thread, it revealed that it has approached a “fraud litigation solicitor” on behalf of investors to pursue Carlauren over “misrepresentation”.

(The conversation below took place in the public domain, in a public Facebook group, but personal names have been blanked as a courtesy.)

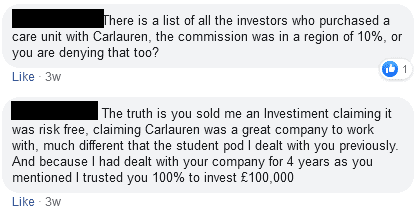

Angry clients of One Touch queried One Touch’s own role, accusing it of taking 10% of Carlauren investors’ money in commission.

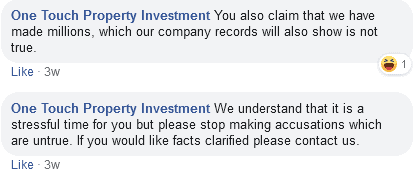

One Touch did not deny taking 10% in commission, though it did dispute a supposed accusation that it made “millions” (no investor actually mentions “millions” in the thread).

What One Touch’s company records actually show is: not a lot. The company has consistently used small company exemptions and does not publish its profit and loss account via Companies House, meaning that how much One Touch received for selling Carlauren investments is unknown.

Several investors suggested One Touch should refund to investors the commission it made from selling Carlauren investments. One Touch did not respond to these requests.

Administration update

Three Carlauren entities are already in administration, with Quantuma LLP appointed as administrators: Carlauren Lifestyle Resorts, Carlauren Care and Accordiant. The latter was responsible for the committment to pay returns of 10% per year to investors.

Quantuma recently revealed, in their initial report into Accordiant, that they have applied for the wider Carlauren group into administration. As at September 2019 an initial hearing had been adjourned, and the Administrators are awaiting a hearing date.

In the meantime, director Sean Murray has been required “to give undertakings to the Court that each of the respondent companies’ assets will not be disposed of or dealt with in any way other than the ordinary course of business”.

Carlauren’s directors are opposing their application to put the wider Carlauren Group into administration and have challenged the validity of the current Administration.

Carlauren itself is adopting either an ostrich or “lights are on but nobody’s home” approach to the administration. Carlaurengroup.com now redirects to carlaurenlifestyle.com, which makes no mention of the administration.

Cryptocurrency miner Viderium has filed its first accounts for the year ending December 2018.

The company aimed to raise £5 million from bonds paying 9.8% for a 3 year term, reviewed here in June 2018 (its accounts say their loans carry interest between 9.8% and 12%). Its accounts show that as at December 2018, it missed its target by about £1 million, with total creditors of £3.9 million.

Viderium’s information memorandum stated that in its first year, it would target revenue of £2.7 million and a net loss of £224k, before hitting profitability in year 2.

Viderium has not published its profit and loss account, and its accounts were unaudited, so the amount that can be gleaned from its published accounts is limited. And an allowance has to be made for it raising 20% less than it hoped.

Nonetheless, it is clear from the net liabilities figure of £2.15 million that year 1 losses were considerably greater than hoped. Exactly how the losses broke down is not stated in the published accounts.

With the first bonds not repayable until 2021, there is naturally time for Viderium to turn things around.

Three of Viderium’s leading staff members, Alexander Johnson, Ross Archer and Russell Spratley, divide their time between Viderium and their new venture, Whisky Cask Company, reviewed here a few weeks ago.

A filing on Companies House shows that Blackmore Bond has again exploited the accounting-period-shortening trick to extend the date that its accounts are due.

Blackmore Bond plc should have filed its December 2018 accounts by June 2019, but used the one-day-shortening loophole to legally delay filing accounts for three months. That three months expired on Friday 27th and on the very same day, right in the nick of time, Blackmore Bond electronically submitted a further adjustment.

Blackmore cites the resignation of its auditor, Grant Thornton, as the reason for its failure to file accounts in a timely fashion.

Immediately after London Capital and Finance was shut down by the FCA, Blackmore replaced LCF at the top of Surge’s Top Isa Rates and Best Interest Rates websites. Given the level of undesired publicity it has received as a result, this marketing strategy has arguably backfired.

Blackmore has now stopped accepting investment from UK investors and, almost uniquely for a UK-based investment company, only accepts investment from outside the UK, via its Blackmore International website.

The administrators of Asset Life have released their initial report.

Asset Life plc, reviewed here in January 2018, raised £8.9 million from investors in three unregulated minibond issues (A, B and C). At the time of my review they were offering 8.75% per year for a three year term.

When the A and B investors were due to be repaid, Asset Life failed to do so. Asset Life plc asked for 12 months’ grace, which some gave, but others refused. Asset Life was unable to repay those investors who insisted on getting their money back. Interest payments stopped in November 2018.

What regulated activities the FCA thought Asset Life plc might be up to is still unclear (even the administrators say they are still in the dark on this point). Raising funds in unregulated minibonds is not a regulated activity, nor is investing them in random mines in Elbonia.

Nonetheless the warning had the effect of preventing Asset Life plc from taking new money in from its Series C bonds, “leaving it with insufficient working capital to meet its existing obligations” (which glosses over the fact that Asset Life plc hadn’t had enough money to meet its existing obligations since it defaulted on the Series A and B investors and stopped paying interest in November 2018).

Asset Life went into administration three months later in August 2019.

The investment

Investors’ funds were to be used to invest in companies with significant growth potential.

Only two such companies remain: Aprelskoe, which is not a virulent Swedish liqueur but a Kyrgyzstani gold exploration company, and Lori Iron and Steel, an Armenian iron ore extraction company.

According to Asset Life plc’s directors, neither is capable of returning any funds without throwing good money after further investment.

The administrators have been advised that there is no realistic prospect of selling Asset Life plc’s shares in Aprelskoe or Lori except to the companies themselves or a connected party.

The administrators therefore intend to continue holding the investments while they continue discussing with other shareholders.

According to the administrators, all of Asset Life plc’s other investments resulted in total losses.

With wearisome predictability, the Asset Life plc directors blamed Brexit for the company’s collapse.

The directors explained to bondholders that there were various reasons for the delay in repayment of the loans, including poor market conditions as a result of the UK’s current political situation, and the uncertainty of Brexit hampering investment decisions.

How specifically Brexit is to blame for Asset Life plc’s failure is unclear. The fall in Sterling after the 2016 referendum should have made it easier to pay back investors’ money in Sterling using revenue earned overseas in obscure ex-Soviet satellite states, not harder.

Prospects for return

Series C bond investors are being treated as secured creditors while Series A and B bond investors are being treated as unsecured.

A Security Trustee was initially in place for the Series A investors but the Trustee company was dissolved shortly after funds were raised.

The fact that Asset Life plc’s old investors are outranked by their new ones could come as a kick in the teeth, if of course Asset Life plc does actually manage to realise any returns for bondholders at all after paying the administrators’ fees. This would appear to be extremely uncertain.

Director Martin Binks failed to provide a proper Statement of Affairs, instead submitting only previously published accounts and a schedule of bondholders (not a full list of creditors), plus “various items of loose paperwork”.

The administrators have done their best to provide their own schedule, but their list of assets has £8,000 of cash in the bank as the only asset with any known value, with all other assets listed as “nil” or “uncertain”.

What happened to the Lenders Guarantee and insurance?

As late as July 2017, Asset Life plc claimed on its website that funds were guaranteed up to £250,000. In October 2016, this guarantee was supposedly provided by GEF Guarantee Equity Fund Limited.

[Our Fixed Interest Plan] offers an inclusive Lenders Guarantee by GEF Guarantee Equity Fund Limited which protects both the deposit and interest promised to our clients at Asset Life.

GEF Guarantee Equity Fund Limited was a company in Israel owned by a UK company, GEF Guarantee Equity UK Limited. In October 2016, the UK parent had already been in liquidation for half a year.

At some point between then and July 2017, Asset Life plc replaced this with a similar Lenders Guarantee – still with “Capital deposit and interest protected up to £250,000” – this time covered by Klapton Insurance, headquartered in Anjouan, a small island in the Indian Ocean.

However in February 2018 the claim that the insurance guaranteed investors’ capital was removed and replaced by the more vague “an active form of indemnity insurance to cover the Loan”. The insurer was not named except as “underwritten by A rated (AM Best) Rated insurers, either Lloyd’s of London or Company markets”.

Of these various insurance policies there is no mention in the administrators’ report.

Around February 2018, the FCA-regulated company responsible for signing off Asset Life plc’s website switched from Opus Capital to Equity For Growth (Securities) Limited.

Asset Life plc Chairman Martin Binks is well-experienced in the unregulated minibond sector.

Binks was a director of collapsed minibond firm London Capital & Finance from October 2015 to August 2016.

Since May 2014 Martin Binks has been a director of another former minibond firm, Anglo Wealth Limited.

In December 2018 Anglo Wealth Limited was described as an “elegantly packaged scam” by a Southwark Crown Court judge, who sentenced two other Anglo Wealth directors, Terrence Mitchell and Andrew Meikle to suspended prison sentences and disqualification as directors.

According to the administrator’s report, Mitchell remains Asset Life plc’s joint-largest shareholders with a 10% share (banned directors are not banned from being shareholders).

Binks was not part of the criminal case and has not been accused of any wrongdoing in relation to his ongoing role at Anglo Wealth.

Despite the fact that the bulk of the Anglo Wealth funds were “dissipated on supporting the defendants’ lifestyles”, according to lawyers advising the CPS, Anglo Wealth investors were repaid in full.

The connections between Asset Life plc and Anglo Wealth are identified as an “area of specific concern” by the administrators.

We are aware that certain individuals previously involved in managing Asset Life plc were disqualified in acting in the promotion, formation and management of any company following criminal proceedings relating to a predecessor company, Anglo Wealth Limited (AWL). The Company’s audited accounts show that Asset Life plc acquired a number of its holdings from AWL in consideration for writing off an intercompany debt. We are therefore investigating the relationship between AWL and Asset Life plc, and the nature and extent of the intercompany transactions.

So, just to make sure everyone is following along:

Anglo Wealth raised just over £1 million from investors (according to its 2017 accounts, the last filed before it repaid investors).

Anglo Wealth was, according to the judge that sentenced Meikle and Mitchell, an “elegantly packaged scam”.

According to lawyers assisting with the prosecution, “Unusually for a prosecution of this type, the investors were re-paid in full (albeit only after the pair knew they faced criminal investigation)”.

Anglo Wealth managed to find money to repay the investors despite the fact that the investors’ money was already gone, Anglo Wealth having “dissipated the bulk of the funds on supporting the defendants’ lifestyles.”

In part due to the fact that Anglo Wealth managed to repay its investors with other money from sources unknown, Mitchell and Meikle did not see the inside of a prison cell, receiving only suspended sentences plus fines totalling £250,000 (less than a quarter of the amount they scammed from investor).

Asset Life plc, described by the administrators as Anglo Wealth’s successor company, raised a total of £9 million from investors between 2014 and 2019.

Anglo Wealth borrowed money from Asset Life plc (this is the intercompany debt referred to in the administrators report).

This intercompany debt was settled by Anglo Wealth passing holdings to Asset Life plc.

All these holdings received from Anglo Wealth to settle this debt to Asset Life have either gone bust with total losses, are of uncertain value, or were realised before the company defaulted on its investors and entered administration.

The administrators’ investigations continue.

…The lack of accounting records and the involvement of numerous third party payment agents has made the task of reconciling the Company’s financial affairs extremely challenging.

Due to the lack of transparent information on the trading transactions of this Company, we anticipate that these investigations may take some time. In addition, our investigations are likely to require the use of Insolvency Act 1986 powers to compel the provision of information from third parties.