The administrators of Basset & Gold, the collapsed unregulated investment scheme promoted by West Ham FC, have released their latest update.

Basset & Gold’s funnelled investor funds into payday lender Uncle Buck, via an intermediary shell company, River Bloom UK Services (aka RBUK).

The bad news for investors is that the administrators predict total losses, regardless of how much is recovered from Uncle Buck, due to another River Bloom company, registered in Cyprus, outranking Basset & Gold investors.

Any recoveries in UB are first due to be paid to RBC as they are the senior debt holders, further recoveries after payment in full to RBC are then applied to RBUK and this is where recoveries for Basset & Gold plc bond holders would come from.

The redress procedure will affect the amounts payable to RBC and hence any potential recoveries to RBUK. Based on current information it is unlikely there will be a return, however we will update bond holders in our next report.

The good news for investors is that the Financial Services Compensation Scheme has agreed to bail out one of Basset & Gold’s investors, paving the way for further claims by anyone sold Basset & Gold bonds since 1 March 2018 (including funds which were invested before that date but rolled over afterwards).

We have been advised in recent days that the FSCS has completed the assessment of at least one claim, and found it valid under their rules. Therefore, they will soon be declaring B & G Finance Limited ‘in default’ and commencing the agreement and payment of compensation claims.

Basset & Gold marketed itself to investors while specifically holding out the possibility that they would be compensated by the FSCS if B&G defaulted.

Basset & Gold Facebook comment to potential investor from 2018.

Mis-selling of Basset & Gold bonds was not an “unlikely eventuality” but part of its business plan. Basset & Gold’s website employed a number of misselling tropes including describing its high-risk loan notes as “cash bonds” and “Pensioner Bonds”, claiming that its structure “protects our investments and your capital” and that its “100% track record” was some sort of assurance rather than completely irrelevant. All these tropes have been identified as misleading by the FCA in the past few years.

As I’ve noted before, this means that B&G attempted the unusual feat of setting the FSCS up as an unwilling guarantor of its unregulated investment scheme in advance. The early signs are that the FSCS is going along with it – unless the successful claims that the administrators refer to turn out to be a small minority.

(Basset & Gold set up a separate limited company to market the bonds which secured regulated status from the FCA in 2018. The investment scheme itself, i.e. the offering of loan notes and the funnelling of that money to Uncle Buck via companies in Cyprus, remained unregulated.)

We can infer that the administrators seem to think that other investors will succeed in their claims, otherwise mentioning the successful claims in their report would achieve nothing accept to give investors false hope. The FCA also gave indications that misselling of B&G bonds had been widespread.

It remains to be seen how many claims of misselling will be accepted by the FSCS, but the general public (who ultimately pay for the FSCS via their bank accounts, loans, pensions and other financial products) should probably brace itself for a very large payout.

The administrators continue to investigate the relationships between the various component parts of the Basset & Gold / River Bloom scheme.

£2.4 million worth of cash has been recovered in addition to an £100k loan made via a P2P platform. Net recoveries currently stand at £1.9 million but this is before the administrators draw their fees, which have been agreed at £1.75 million plus 25% of recoveries.

The administrators of collapsed West Ham sponsor Basset and Gold have released their initial report.

Around 1,800 people, described as “everyday investors” by the administrators, invested nearly £36 million into Basset & Gold after being recruited by “internet based marketing and social media campaigns”.

Despite Basset & Gold’s literature claiming that investments were “backed by assets, such as property, corporate debentures and other forms of security in order to PROTECT our investments and your capital”, virtually all of investors’ money was loaned to a payday lender called Uncle Buck.

The opening stanza of the administrators’ potted history reads bizarrely like marketing copy.

The initial target for the business was to provide everyday investors with fixed interest returns, that were easy to understand, using fixed income investments with no additional fees involved.

What this nonsense has to do with Basset & Gold, which gave its investors little chance of understanding that they were investing almost all of their money in a single payday lender, or that “no additional fees” meant 20% of investor monies would be paid to companies controlled by B&G owner Hadar Swersky as commission, is unclear.

The administrators continue:

B&G achieved its targets and provided significant growth year on year.

The only thing that was actually growing was B&G’s debts to investors, from £2m in 2016 to £36 million in 2020. B&G’s (virtually) sole debtor, Uncle Buck, made a loss in all of the four financial years up until it went bust, with its net liaibilities deteriorating from minus £1.4 million in March 2017 to minus £20 million in February 2020.

In April 2019 Basset & Gold stopped marketing its bonds as the FCA started nosing around after the collapse of London Capital & Finance.

Basset & Gold employed an independent firm to carry out a due diligence exercise into Uncle Buck.

They concluded that Uncle Buck would only repay its loans if new money continued to flow in from B&G.

It is believed that the completed independent business review concluded that UB should be able to repay the debt due on time but this was contingent on B&G continuing to fulfil its obligation to UB by virtue of continuing to fund UB’s activities as a HCSTC [payday loans] provider.

In June 2019 B&G were contacted by the FCA who raised concerns about Uncle Buck’s negative balance sheet and bad debt provision. B&G commissioned another independent review, which “portrayed a positive situation with minimal issues identified in respect of UB’s systems and processes”. This failed to mollify the FCA.

Towards the end of 2019 Uncle Buck were supposedly confident of finding £3 million a month worth of lending which would allow it to become profitable. However, in March 2020, “for reasons yet to be explained to the Administrators”, Cypriot shell company River Bloom called in the loan to Uncle Buck, which it was unable to repay, and the jig was up.

Basset & Gold owner Hadar Swersky

Note that as per a diagram in Appendix B, Basset & Gold = River Bloom = River Bloom UK Services = entities controlled by serial entrepreneur Hadar Swersky, which raised money from investors and loaned them to Uncle Buck, a company controlled by a Steven Murray.

While the administrators have managed to recover £2.3 million in cash, they do not expect “any material recoveries for bond holders from the Administration of Uncle Buck”.

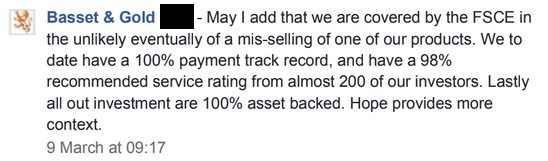

Investors hopes for recovery rest largely on the FSCS. Despite minibonds not being covered by the FSCS, Basset & Gold representatives marketed their bonds specifically on the possibility of FSCS compensation if things went south.

Back in 2018, an investor was told by Basset & Gold’s official Facebook channel:

May I add that we are covered by the FSCS in the unlikely eventually of a mis-selling of one of our products. We to date have a 100% payment track record, and have a 98% recommended service rating from almost 200 of our investors. Lastly all our investments are 100% asset backed. Hope this provides more context.

Given Basset & Gold’s systematic use of misleading literature, which banged on about its irrelevant “100% payment track record” and compared its investments to cash deposits, all identified by the FCA as misleading practice, you’ll struggle to find a Basset & Gold “everyday investor” who won’t claim they were missold.

Still, it’s not all bad – thanks in part to sponsorship money funded by Basset & Gold investors, West Ham FC have successfully kept themselves in the Premier League to entertain us all next season. Which, if claims on the FSCS are successful en masse, will be converted into another load of subsidy from the general public. Up the Sc… I mean Hammers!

After being denied compensation from the Financial Services Compensation Scheme (other than a tiny handful of exceptions,) London Capital & Finance investors have raised money via crowdfunding to launch a judicial review.

As at 23rd April the campaign had already raised £7,833, exceeding its initial £7,000 target. Technically the campaign is to fund the judicial challenges of only the four LCF investors on the creditors’ committee, but if their challenges succeed, this will surely set a precedent for the rest.

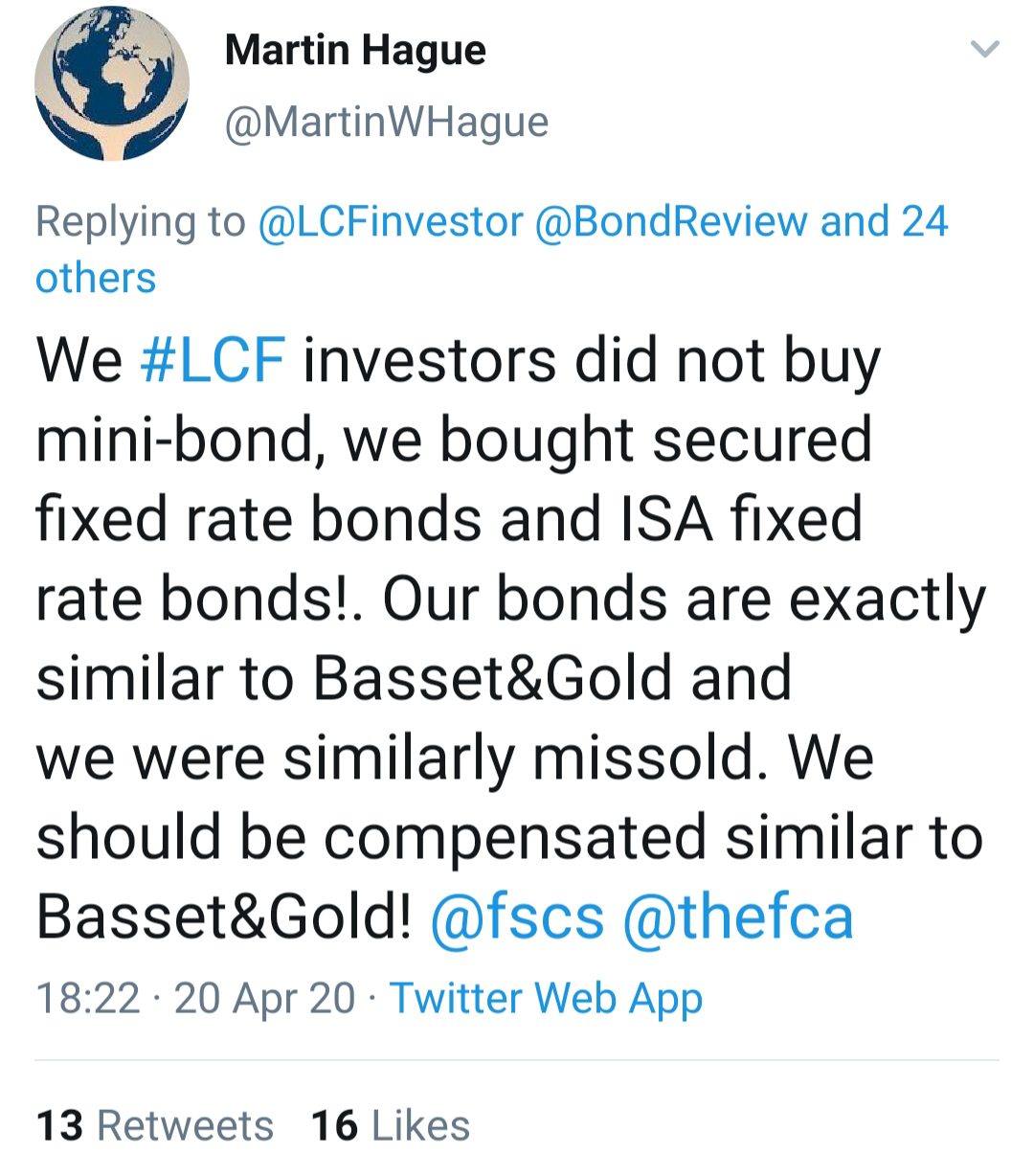

London Capital & Finance investors have been both emboldened and enraged by the FSCS’ early indications that it will bail out investors in fellow collapsed minibond scheme Basset & Gold, which went into administration on 1 April.

We have concluded there will be some customers who were given misleading advice by LCF and so have valid claims for compensation. However, we expect that many customers will not be eligible for compensation on this basis.- Jan 2020 FSCS announcement

By contrast, Basset and Gold investors have been given a far more positive indication by the FCA that compensation will be payable on the grounds of misselling.

The FSCS has determined that many investors have a good prospect of claiming compensation.– Apr 2020 FCA announcement

The distinction between LCF and Basset & Gold is that LCF had one FCA-regulated company, which both issued the investment and the investment literature, while Basset & Gold had two separate companies, one of which was not FCA-regulated and issued the minibonds, the other of which was FCA-regulated and issued the investment literature.

Which is of course entirely meaningless from the perspective of an ordinary retail investor. Nothing was stopping LCF from setting up two different companies instead of one, and keeping the misselling separate from the bonds themselves, except that they didn’t think of it (or care).

It is therefore not a surprise that the Basset & Gold collapse has given LCF investors fresh hope for compensation.

Commentary

My own money would be on the regulator and the Government as a whole eventually figuring out a Barlow Clowes / Equitable Life solution – i.e. compensation paid, not in line with arcane FSCS rules that even they don’t seem to understand, but on a one-off basis in recognition of regulatory failures which allowed LCF to run longer than necessary and lose more ordinary savers’ money than was necessary. This is what happened in recognition of regulatory failures over Barlow Clowes (in the 80s) and Equitable Life (in the 90s).

The litany of regulatory failures by the FCA is not seriously disputed. The FCA gave London Capital & Finance the “CAT standard” of FCA registration and ignored the systematic misselling of its investments for a further 3 years afterwards despite numerous attempts by outsiders to blow the whistle. As the FCA CEO in charge at the time has now been kicked upstairs to the Bank of England, the FCA is now free to issue regular mea culpas and lessons will be learneds.

Whether the FSCS or the Treasury pays compensation makes little difference as the general public pays either way; nearly everyone pays taxes and nearly everyone pays FSCS levies via use of financial services.

The main obstacle in the way of compensating LCF investors is moral hazard; the fear that if LCF investors are compensated, it will encourage others to invest in schemes paying unrealistically high returns for supposedly safe investments on the assumption that they’ll get their money back if it goes wrong.

The obvious counterpoint to the moral hazard argument is that the exact same argument applied to compensation for Barlow Clowes, the exact same argument applied to Equitable Life, and the exact same argument applies to Basset & Gold. In the first two cases the moral hazard argument was beaten by the argument that such a monumental failure of regulation and Government should result in compensation, and improvements to the regulatory system to ensure it doesn’t happen again.

There is a better way than whataboutery for LCF investors to counter the moral hazard argument; campaign not just for compensation but for the UK to bring the UK’s securities laws out of the 1920s and require all investment securities offered to the public to be regulated by the FCA, as is the case in the US.

If it becomes more difficult to open unregulated investment schemes and promote them to the public, this would counteract the moral hazard incentive to open and invest in them. It offers the taxpayer’s purse a quid pro quo – a one-off compensation payment (trivial in the grand scheme, especially now) in exchange for less economic damage in the future.

Or we could just do nothing and wait for the next wave of unregulated investment scandals, some of which, like Basset & Gold or investments recommended by dodgy FCA-regulated advisers, will inevitably fall onto the public purse. As my old ma always said, if you keep doing what you’ve always done, you’ll keep getting what you’ve always got.

So far so normal. Unregulated high risk investment fails, news at 11.

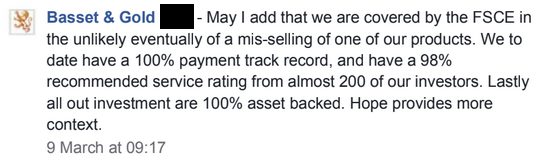

What was unusual about Basset & Gold is that back in 2018 at least, they were promoting their bonds while explicitly holding out that investors might be compensated by the FSCS if things went sour – on the basis of misselling.

From Basset & Gold’s Facebook page in March 2018, since deleted. [sic]The FSCS confirmed on 1 April that investors can make a claim for misselling if they were sold their bonds via Basset & Gold’s FCA-regulated company.

Although Basset & Gold Plc has also entered administration, FSCS is unlikely to be able to pay compensation based purely on Basset & Gold Plc’s failure to repay the bonds, as issuing bonds is not normally a regulated activity.

For FSCS to be able to pay compensation, the customer must have been mis-sold their bonds, for example, because they relied on a misleading statement about how Basset & Gold Plc was investing their money.

How many Basset & Gold investors were missold the bonds? The Financial Conduct Authority suggests it’s quite a lot.

The FSCS has determined that many investors have a good prospect of claiming compensation. […]

We had concerns around the accuracy and fairness of B&G plc’s financial promotions of the mini bonds.

As a result, B&G Finance made improvements to its advertising in December 2018 and wrote to all bond holders in January 2019 clarifying that B&G has used ‘the vast majority of Bond proceeds to finance a large facility agreement with an FCA-regulated short-term consumer lender’.

No further bonds were issued to retail investors from May 2019.

In short, the FCA was concerned that B&G plc was misselling Basset & Gold bonds until May 2019. So anyone who invested in Basset & Gold prior to their clarifying their investment literature in response to an FCA investigation, which will be most of them given that Basset & Gold closed to new investment in May 2019 (10 months before it collapsed), potentially has a claim for misselling. This is not according to me or some claims management firm trying to drum up business, this is according to the FCA.

That said, we’ve been here before.

London Capital & Finance, which collapsed at the beginning of last year, was also FCA-regulated. The vast majority of LCF investors are waiting to find out whether they will receive compensation. Early indications from the FSCS are far less positive than the message given to Basset & Gold investors above.

While FSCS maintains that the act of issuing mini bonds is not a regulated activity, and is therefore not something we protect, we have concluded there will be some customers who were given misleading advice by LCF and so have valid claims for compensation. However, we expect that many customers will not be eligible for compensation on this basis.

So whether Basset & Gold investors will be compensated en masse is still not clear.

As a result of IPM’s involvement, investors in Secured Energy Bonds and Providence Bonds were – after a legal struggle – compensated by the FSCS.

In retrospect therefore, both bonds were risk-free. If the bonds had succeeded investors would get higher returns than cash, and as they failed investors were bailed out by the FSCS. (Which is to say the general public.) Naturally the investors didn’t know at the time they would be bailed out, and they faced years of stress and worry while their lawyers fought the Financial Ombudsman, but that is the position with the benefit of hindsight.

The IPM literature was misleading at the time it was being issued to investors, and the legal position is that this made them eligible for compensation from IPM, and in turn the FSCS, if the investment failed (even if it took the FOS a while to acknowledge it). So the investment was in reality risk-free from the beginning – unless investors exceeded the FSCS limits (£50k at the time).

Basset & Gold have essentially attempted the same setup as IPM + Secured Energy Bonds (or Providence). One company issues the bonds (SEB bonds / B&G PLC). Another FCA-regulated company promotes them (IPM / B&G Finance). The bond issuer goes bust. Investors complain that they were missold by IPM / B&G Finance. FSCS bails them out – or has strongly suggested it will bail them out in the case of B&G.

The difference is that if Basset & Gold investors are compensated, Basset & Gold will essentially have executed a risk-free Secured Energy Bonds type scheme in advance, having successfully arranged its business to ensure that investors would be compensated by the FSCS, and having promoted its bonds to investors on the basis that the FSCS would step in, as per the Facebook screenshot above.

Back in September 2018 I asked (deliberately provocatively) whether the precedent set by IPM had made all unregulated investments risk-free, providing they took the fairly trivial step of setting up an FCA-regulated company to approve the investment literature, which is about as difficult as cutting out two tokens from a cereal packet and sending it to the FCA. (Unlike giving financial advice, signing off investment literature does not require professional qualifications and specific permission from the FCA.)

The collapse of LCF appeared to show it hadn’t. When they bailed out SEB and Providence investors the FOS inserted an anti-precedent device into its reasoning, stating very specifically that SEB and Providence investors were being compensated because IPM was particularly closely intertwined with the businesses it was promoting. IPM did not just sign off the literature but act as Security Trustee. This didn’t apply to London Capital and Finance, which both issued and promoted its own bonds.

However the much more positive noises made by the FSCS and the FCA towards Basset & Gold investors – “The FSCS has determined that many investors have a good prospect of claiming compensation” – seems to have turned that on its head again.

What is there to stop somebody else following the same business model as Basset & Gold – forming one company which issues the bonds, and another which obtains FCA registration and promotes the bonds – and offering whatever rate it feels like to attract investors, on the basis that investors will be bailed out by the general public on the basis of misselling?

Only the FCA taking prompt action to stop the misselling.

Basset and Gold started in its current business model in late 2015 (when an off-the-shelf company called Bladegold was acquired and renamed). Readers have alleged that its activities were reported to the FCA in 2017. No visible action was taken by the FCA until December 2018 when B&G changed its literature, and B&G was eventually stopped from taking new money in May 2019, before collapsing 10 months later.

So in other words, we – that is, all of us who pay FSCS levies via our bank accounts and pensions – are screwed.

Another angle on the Basset & Gold story is the remarkable ability of West Ham to source money from the general public.

There is in reality no difference between the taxpayer and the FSCS-levy-payer as everyone in the UK pays taxes and everyone in the UK uses financial services.

West Ham already play in a stadium that was built by the taxpayer for the 2012 Olympics. As you don’t get crowds of 50,000+ to watch humans running in circles unless the Olympics is on, and the Olympics comes to the UK once in a lifetime, West Ham were allowed to rent the stadium on very favourable terms, to avoid the embarrassment of the Olympic Stadium being knocked down for flats.

Basset & Gold investor money was used to fund sponsorship to West Ham. If the FSCS bails out Basset & Gold investors to any substantial degree, that means the general public’s money replaces Basset & Gold investors’ money in that equation.

Basset & Gold, which offered unregulated bonds, “pensioner bonds” and 30-day “cash bond” notice accounts, announced today that it has gone into administration.

Paul Boyle, David Clements and Tony Murphy of Harrisons Business Recovery and Insolvency (London) Limited were appointed as joint administrators of Basset & Gold PLC (the Company) on 1 April 2020 (the Joint Administrators). They were also appointed as joint administrators of B&G Finance Limited (B&G Finance), a related company, on the same date.

The Company which is not regulated by the FCA, issued bonds which were sold to retail consumers. B&G Finance, which is regulated by the FCA, acted as an intermediary between the Company and investors, arranging investments in the bonds sold by the Company.

Following the appointment of the Joint Administrators there will be no further bond issuances or related investment activity. No bonds have been issued to retail investors from May 2019.

[Hat tip to reader John Doe for spotting the announcement.]

I reviewed Basset & Gold’s bonds in December 2017, commenting that contrary to their “100% asset backed” spiel, the bonds were high risk unregulated investments with an inherent risk of 100% loss.

Basset & Gold claimed on its 2018 website that its bonds offered a “high level of security”. The company also used to claim to offer FSCS protection, on the basis that one of its companies, B&G Finance Limited, was regulated by the FCA, and therefore investors were covered for “misselling”.

Comment from B&G’s Facebook page in March 2018 (the original post appears to have been deleted along with the comment)

How many investors successfully make FSCS claims for Basset & Gold’s failed investments being missold to them remains to be seen.

It also remains to be seen whether the bonds being “100% asset backed” results in recoveries for investors. In other “asset-backed” investments which went into administration, investors have faced anything up to 100% losses as the assets backing the investments were not worth nearly enough to repay creditors.

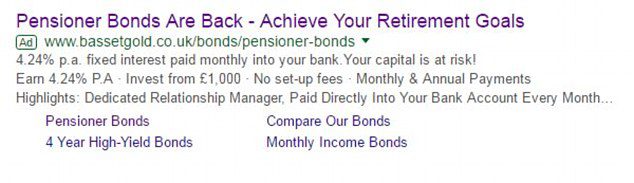

In addition to its West Ham tie-up, Basset & Gold sold its investments via Google Ads, at one point piggy-backing on NS&I’s popular (and risk-free) “Pensioner Bonds”.

The company has sponsored state-funded football club West Ham United for several years and prominently features the tie-up in its advertising. Its Facebook page is still dominated by West Ham players bedecked in Basset & Gold logos.

The announcement provides no explanation as to why Basset & Gold has fallen into administration.

Reviews left last month on reviews.co.uk suggest the company was already struggling with payments to investors.

Last week I telephoned and was told some one would call me back and no one did. I called again the next day and eventually was put though to my find manager who showed little interest but assured me that he would sort the issue and email me that day. I am still waiting and getting very anxious about the safety of my investment.

As at September 2018, Basset & Gold’s investments consisted almost entirely of money loaned to River Bloom UK Services Limited. River Bloom UK Services Limited published accounts for December 2018 which were unaudited and contained almost no information beyond that the company had £35 million in debts and £35 million in assets described only as “other creditors”.

Hadar Swersky, controller of Basset and Gold

Both Basset & Gold and River Bloom are controlled by Hadar Swersky, Israeli founder of hedge fund Smart Box Capital. In 2015 Swersky described himself as “an award winning hedge fund manager and entrepreneur. Widely regarded as a savvy investor with accurate trend spotting, his fund was an early mover in multiple fields including algorithmic trading, online option trading and online alternative finance. “

Basset & Gold has filed its accounts for the year ending September 2018.

Basset & Gold is now one of the UK’s most visible issuers of unregulated bonds, thanks to its sponsorship of Premier League football team West Ham United.

It currently offers a one-year “Fixed Monthly Income Pensioner Bond” paying 4.24% over the year a 3-year IFISA paying 6.12% per year, and a 5-year IFISA paying 8.15%. All are capital at risk investments that, like any loan to a micro-cap unlisted company, have a risk of up to 100% loss.

According to its accounts, it now owes just under £30 million to investors, up from £13 million in 2017.

Its net assets position is slightly above water at £233,784.

At the time of its 2017 accounts, Basset & Gold’s assets consisted almost entirely of loans to a company registered in Cyprus, River Bloom Limited. B&G has now apparently shifted these loans into the UK; its assets now consist almost entirely of loans to a UK company, River Bloom UK Services Limited.

B&G’s auditors (Shaw Wallace) emphasise that the financial viability of B&G depends on the “counter party” to whom River Bloom UK Services Limited lends investors’ money. It seems likely that this counterparty is either the Cypriot company or another company controlled by Basset & Gold’s owner.

Emphasis of matter

…The valuation and recoverability of this loan from River Bloom UK Services Limited is dependent on the financial strength of the counter party to whom it advances investments. Whilst the management accounts of River Bloom UK Services Limited show a neutral position, the directors of Basset & Gold plc have carried out a thorough impairment review of the profitability, solvency, liquidity, forecasts [sic] as well as a review of the unqualified audited accounts of the counter party of River Bloom UK Services Ltd and are satisified that counter party maintains its ability to service the facility and repay investments to River Bloom UK Services Limited.

Under ISA auditing rules, the inclusion of this item as an “emphasis of matter” indicates that the directors being satisfied that RBUSL’s counterparty remains able to service its debt to RBUSL (and in turn to Basset & Gold’s investors) is fundamental to users’ understanding of the financial statements.

According to its last confirmation statement, Basset & Gold is majority-owned by Israeli Hadar Swersky.

up to 7.46% per annum for bonds paying monthly income for a term of up to 5 years

7.7% per annum for 5-year bonds with interest rolled up

4.32%pa on 1-year “pensioner bonds” for the over 55s only

and 3.14% on “cash bonds” which pay interest bi-annually and are redeemable by giving 30 days’ notice.

Who are Basset & Gold?

There is no information on the website on who the directors or owners of the company are.

Companies House shows that Basset & Gold plc is wholly owned by B&G Investments Ltd, a company registered in the Seychelles. I was unable to find any information about B&G Investments.

The directors of Basset & Gold plc are Daniel Smith and Dror Israel Sordo.

Dror Sordo was previously the Chief Executive of PlusUK500, an AIM-listed CFD and forex-trading website – essentially a bookmaker for gambling on financial markets. According to the FCA register, he left that position in 2013, although his LinkedIn profile has not been updated.

Investors should think very carefully before investing money with a company that is not upfront about who is owning or running it.

How secure is the investment?

All investments offered by Basset & Gold are unregulated corporate loans and if Basset & Gold defaults you risk losing 100% of your money.

There are very few details on the website as to how your money is invested by Basset & Gold, but a risk warning at the bottom of the website states “Investment through the Basset & Gold Fixed Income Bonds involves lending to companies or individuals and therefore your capital is at risk and interest payments are not guaranteed if the borrower defaults”.

There is a vague reference in the risk warning to the investments being asset-backed. However, if for whatever reason Basset & Gold is unable to sell the assets your bond is secured on for enough money to cover its obligations, investors still risk losing up to 100% of their money.

Should I invest with Basset & Gold?

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

This particular bond is advertised as asset-backed. Before putting any reliance on the security backing the bond, investors should undertake professional due diligence to ensure that a) the security exists b) in the event of default, the security could be easily sold and would raise enough money to cover all investors’ money c) the charge over the security has been properly and legally recorded.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “cash investment” or an investment that offers “security”, you should not invest in unregulated products with a risk of 100% capital loss.