With the taxpayer still reeling from the £170m+ bill that has fallen on them from the London Capital and Finance scandal, is it time to start issuing a “ScamSmart” leaflet to first-time investors who’ve just come into large lump sums?

During the last wave of “pension liberation” scams in the early 2010s, hundreds of millions of pounds were lost by investors who transferred their pensions to fraudsters who promised fabulous returns and “loopholes” that would allow the investor to release their money earlier and in larger quantities than the rules allowed.

Although pension fraud remains rife, the scale of the problem was dampened by in a number of ways:

HMRC no longer allowing anyone to set up a pension scheme if they sent in two tokens from a breakfast cereal packet

George Osborne’s “pension freedoms”, which dramatically reduced the appeal of “pension liberation”

“ScamSmart” leaflets were issued to anyone who might be considering a transfer, with a distinctive scorpion cover and clear warnings about what a scam might look like.

If people making a decision on what to do with a large pension fund should be given a leaflet to try and stop them doing something really foolish with it, could the same be done for people who’ve received a large non-pension sum of money into their accounts?

A recurring theme in the fallout of London Capital and Finance was the stories of people who had received a large sum of money, larger than they had ever handled before in their life; typically inheritance, pension commencement lump sums, or downsizing proceeds, and invested the lot in LCF. Often having thought they had done the right thing by checking it was an FCA-regulated firm. It is easy to say they should have sought independent regulated financial advice, especially as they should have. But you don’t know what you don’t know.

It should not be too impractical to draw up rules for solicitors, banks and pension companies that state that if a client is to be paid a sum of money larger than £100,000, and that the company handling the money

is not aware that the client intends to immediately use the money [e.g. buying another house with it]

and does not have evidence on file that the money is a relatively modest part of the client’s free assets, say 25% or less

…then a one or two page leaflet should be issued before releasing the money warning them of how easy it is to lose a large sum of money as a first-time investor. The leaflet could run along the following lines:

Don’t use social media or Google to look for investments.

Consider talking to a regulated, independent financial adviser on how to use the money.

A large sum of money kept in cash will lose value to inflation over time. Mainstream investments go up and down but should only lose money if they are cashed in during a fall, or not properly diversified, or use gearing.

Don’t use social media or Google to look for investments.

Be suspicious of any investment that promises returns that seem too good to be true. Beware any “cash” or “guaranteed” account that pays even slightly more than normal bank accounts. Beware any investment that is not diversified across the world’s major stockmarkets.

Don’t use social media or Google to look for investments.

I’m normally the first person to scoff at anyone who suggests that the solution to a problem is to issue a leaflet and tick a box. But I’m not proposing a “ScamSmart” leaflet on the grounds that it will stop scams; just that it might stop a few investors losing their money.

It will also force us to confront the reality that someone who has just received a sum of money larger than they’ve ever handled before is being thrown into a pool of sharks blindfolded. The first step to solving a problem is to admit that we have a problem.

The Government’s “Online Harms Bill” was originally set to address racism, child abuse and romance scams.

An amendment by MP Stephen Timms was brought forward that would have brought investment scams within the scope of the Bill, including powers to fine Google and other search engines if they failed to tackle investment scams.

The amendment received a broad coalition of support including FCA head Nikhil Rathi, the CEO of advice and asset management giant Quilter, the Financial Services Compensation Scheme (FSCS), TV’s Martin Lewis and the Money and Mental Health Institute.

But despite positive noises being made by the Government, the Queen’s Speech made no mention of financial harm when introducing the bill.

The amount of money lost into scams would collapse dramatically overnight if search engines were subject to a fine (or, even better, held liable for investor losses) if they promoted any investment to UK investors that does not have authorisation from the Financial Conduct Authority.

Google would probably say that it is impractical, given the number of ads placed via its system, to vet every single one that mentions investment. However that is exactly what they said for years to justify why YouTube was filled with copyrighted material including virtually every popular film and TV show available to download in full (in 10 minute chunks). When the possibility of being held liable for copyrighted content become imminent, a technological solution was suddenly and magically found.

Given that banks can now be held liable for frauds in which they have done no more than send money to where their customer asked them to send it, it makes little sense to say we can’t expect Google to check whether someone advertising an investment scheme can actually do it legally – a burden no greater than expecting Google not to bring up an advert for your local drug dealer if you type in “cocaine”.

But that is by the by as the Government apparently sees no need. Scam epidemic? What epidemic?

The interminable saga of London Capital and Finance returned to the newspapers this week when John Glen, secretary to the Treasury, provided an update to the Sunday Telegraph on the announcement that the Treasury would set up an ad-hoc compensation scheme to compensate LCF investors who have so far missed out.

This is not a decision that requires a lot of head scratching, nor can the Treasury claim it is waiting for more information, two years since the FCA-authorised Ponzi scheme collapsed.

refuse to pay compensation (as the Government usually does when unregulated and pseudo-regulated investment schemes collapse – albeit mostly because they don’t often take in £240m and make the national press)

find a novel interpretation of the rulebook that allows compensation to be paid while claiming this is how it’s supposed to work (the Independent Portfolio Managers option)

admit the system has failed and form an ad-hoc compensation scheme (the Allied Steel, Barlow Clowes, Equitable Life etc etc option)

This has become increasingly untenable the more compensation has been paid out, at the expense of those who pay levies to the Financial Services Compensation Scheme, i.e. everyone who uses financial services, i.e. you and I.

So what is preventing the Treasury from making a decision? “We’re busy” isn’t an explanation, as delaying a decision that the Secretary of the Treasury has already announced creates more work, not less, as you still have to make the decision eventually but you also have to issue explanations for the delay on top.

Unless the Treasury is hoping that London Capital and Finance’s stable of duff investments manages to find a deposit of unicorn dust in the North Sea which magically pays out all investments, delaying a decision for three months achieves nothing.

The ideal scenario for all of us is if compensation for LCF investors was announced alongside a comprehensive overhaul of UK securities laws to require all investments offered to the UK public to be registered with the Financial Conduct Authority – as has been the case in the USA for almost 90 years.

The prospect of bailing out yet another collapsed unregulated scheme would be a less bitter pill for the regulated financial sector (and by extension the general public which banks, saves and insures itself with it) if it had a genuine reason to believe that it would be less likely to happen again, and result in a smaller bill when it inevitably does.

Such an undertaking would require a lot of work behind the scenes and could not be announced at the drop of a hat. It could also not be more timely as the UK plots its recovery from the pandemic, a recovery that would be significantly stronger if the UK sloughed off its reputation as the scamming capital of the developed world.

Alternatively, the Treasury could announce that it’s time to move on, lessons have been learned, and the UK will recover from the pandemic by having National Savings and Investments offer Covid bonds at 2% per year (maximum investment £5,000 per person).

At around £19,500 per investor, that’s pretty typical of the average total investment.

Apart from £2.7m for investors who transferred a stocks and shares ISA, the vast majority of that was paid for LCF giving misleading “advice”. Despite not being a financial advice firm, not being authorised to give financial advice, and employing no financial advisers, Financial Services Compensation Scheme levy payers, i.e. the general public, have been put on the hook on the basis of “I’d advise my own mother to invest in this” school of salesmanship.

864 investors have seen their claims on the basis of advice rejected (a quarter of the total).

That £56.3 million bill represents only a quarter of the total number of LCF investors. If this ratio of successful claims continues to hold true over the remaining 7,858 who have not yet received a response from the FSCS, that would cause the total bill to levy payers and the general public to reach £187million. I’ll emphasise that this is a finger in the air calculation, and could be miles out if the FSCS has prioritised claims with more chance of success, for one reason or another.

Still, if that ends up being anywhere close to the final bill, you almost have to ask why the Government didn’t just bail out 100% of LCF investors, rather than arbitrarily excluding a relatively small number. By the time you’ve decided to compensate 75% of investors (with the potential for more if the Treasury decides to pay further ad-hoc compensation), any arguments about moral hazard have already been thrown out of the window.

LCF investors have complained regularly that the system used by the FSCS to assess claims is inadequate, frequently rejecting claims initially and then upholding them if the investor has the gumption to appeal (i.e. the same system used by the DWP to keep the UK disability benefits bill down) and relying on gibberish machine-transcribed versions of recorded phone conversations.

As I’ve regularly predicted, we seem to be heading towards the worst of both worlds where neither LCF investors as a group nor FSCS-fee-payers are satisfied with the outcome.

Real reform of the UK’s securities legislation as a quid-pro-quo for a fair and consistent (but not necessarily 100%) bailout of LCF investors would at least have salved the pain to FSCS levy-payers, i.e. legitimate financial services businesses and the general public, who would be mollified by the fact that another London Capital and Finance couldn’t happen (at least not to the same extent). But as yet the Government seems to have gone with “let’s do the same thing over again and see if it has a different result”.

In one of the more depressing sections of Dame Gloster’s report into the FCA’s mishandling of the FCA-authorised Ponzi scheme (in a crowded field), Dame Gloster highlighted how, instead of using the investigation as an opportunity to learn from its mistakes, the FCA instead tried to shirk responsibility, claiming that holding individuals responsible for their failings might deter people from applying to be senior bureaucrats, and questioning whether, in a very real sense, there was any such thing as responsibility at all.

It also claimed that nobody could have seen the collapse coming (they did) and that the investigation was using the benefit of hindsight (it wasn’t).

Before the Select Committee, current Bank of England Governor Andrew Bailey tried to reverse ferret out of this dodging of the philosophical concept of responsibility, claiming that the report had made a “fundamental misunderstanding” and that he had only sought to remove personal names from the report where they related to “culpability” rather than “general responsibility”.

Gloster for her part refuted that there had been any misunderstanding and stated in an open letter that Bailey’s attempt to have his name removed from the report went beyond what Bailey claimed, and “the distinction between personal culpability and responsibility was merely one argument”.

Before the Committee, Bailey also claimed that Gloster “put it to you that if only we told the staff to pull their socks up the problem would have gone away”. How Bailey got that impression from Gloster’s forensic, comprehensive, nearly 500 page report is a mystery to me.

This is more than a case of “he said, she said”, because implying that the Governor of the Bank of England has not been straight with Parliament is a very serious matter. And yet it is still a side issue.

The best defence for Andrew Bailey would have been to say “Yes, we ignored the numerous whistleblowing reports from reputable professionals and the general public, failed to consider whether a company systematically misselling high-risk bonds needed more investigation then telling them to change the adverts, and wrongly dismissed the whole scheme as ‘not our problem’. But I was merely one big cog in a crappy machine. The entire UK securities law framework is not for purpose, and creates a pathway for high-risk investment schemes to be systematically sold to the public. I screwed up, but because there is a framework that allows you to sell high-risk unregulated investment schemes to the public, as long as you separate out the promotion of the scheme from the investment scheme itself, it was inevitable that someone would screw up.”

But Bailey can’t say that. Because the Governor of the Bank of England can’t tell the world that the UK securities law framework is not fit for purpose. In an interesting new version of the Peter Principle, Bailey has been kicked upstairs into a position of responsibility that gives him too much to lose by calling out the incompetence of those above him.

One of the implicit jobs of the head of the Bank of England, in between taking the flak from savers for lowering interest rates or borrowers for raising them, is to maintain confidence in UK PLC. So admitting that the UK is the scamming capital of the developed world is not going to happen.

London Capital and Finance collapsed two years ago, and there has been no serious movement since then towards:

Reforming the UK’s securities law, starting with the Financial Services and Markets Act 2000, to ensure that any firm offering investment securities to the public must register with the Financial Conduct Authority (or equivalent). In contrast to the current system that randomly exempts loan notes and other schemes that try to dodge the UK’s more limited ban on collective investment securities.

Reforming the FCA from the top down and rooting out its “regulatory perimeter”, aka the cultural attitude of “if it’s unregulated it’s not our problem”.

London Capital and Finance investors are at present still anxiously waiting to see whether the Treasury will announce further compensation for those left behind by the essentially random compensation payments made so far. (E.g. to people who transferred stocks & shares ISAs but not, for no discernible reason, cash ISAs, and people who successfully convinced the FSCS they received advice from a firm which was not a financial advice firm and employed no financial advisers.)

The legitimate financial industry and the general public, who will ultimately have to pay for any further compensation, are anxiously waiting to see whether Parliament will do anything to stop it happening again, and again, and again.

On Thursday 17th, Dame Elizabeth’s Gloster’s long awaited report into the £237 million collapse of London Capital & Finance was published.

The report is damning and makes very clear that the FCA bears a large part of the blame for LCF accumulating, and losing, as much investor money as it did.

Furthermore, the following is, in the Investigation’s view, self-evident: had some or all of the FCA’s failures in regulation outlined in this Report not occurred, then it is, at the least, possible that the FCA’s actions would have prevented LCF from receiving the volume of investments in its bond programmes which it did. For instance, had possible irregularities by LCF been detected (and their significance appreciated) by the FCA42 sooner than late 2018, then the FCA should, in the Investigation’s view, have intervened (or taken other regulatory action) earlier.

This has been widely covered in the press, along with the apology from Andrew Bailey, who was head of the FCA throughout much of LCF’s lifespan, and was rewarded for its failure by being kicked upstairs to the job of Governor of the Bank of England.

Here are some edited highlights for those who want a bit more detail than the headlines, without reading the full 494 page report. This is not intended to be a full summary of the report (so you’ll have to forgive me for skimming over accounts of high-level supervision discussions at corporate away days, important as they are) but a list of the most interesting / juiciest bits for ordinary investors.

LCF was waving red flags from day 1, but its accountants didn’t notice

Accounting behemoth PriceWaterhouseCoopers told the FCA in November 2017, on being replaced by another firm of auditors, that there were no matters to bring to the FCA’s attention. The fact that LCF was paying 25% commissions and had no investments with a realistic hope of paying sufficient returns to fund 25% commissions and 8% interest to bondholders apparently wasn’t deemed worthy of notice.

A chartered accountant hired to review the historic information submitted by LCF to the FCA found “red flags” and inconsistencies in financial information that could have been spotted as early as 2016. It also found that the information provided to the FCA by LCF continually indicated that LCF could not meet its liabilities without raising further investment.

It noted that LCF had to charge up to 29% annual interest to its underlying borrowers to fund its commission and interest payments, and this made no sense considering LCF claimed to be engaged in secured lending with low loan-to-value ratios – such borrowers would have no need to pay such high interest. [A11]

The FCA told potential investors that LCF was not a fraud, and FSCS protected

An elderly (septuagenarian) investor was told by the FCA that LCF was “unlikely to be operating fraudulently” as it was FCA-authorised. This was not an isolated incident. [A6 4.2 and 6.7]

A call-centre worker who did advise a potential investor to be “very cautious” and report LCF to Action Fraud, having correctly identified the misleading nature of LCF’s promotions, and subsequently raised concerns with the FCA’s Supervision division, was slapped down as “in error”. They were told that there was already an article on the FCA’s intranet to say that they were “already aware of this issue” and that LCF was not in breach. [4.6-4.7]

A limited number of FCA call-handlers incorrectly advised LCF investors that they would be protected by the Financial Services Compensation Scheme. [6.2]

Potential investor: It does sound too good to be true doesn’t it?

FCA call handler: Let’s have a look… So that’s [London Capital and Finance] coming up as authorised and regulated, so that’s absolutely fine. That means if you wanted to invest with them, you’d be protected by up to £50,000 by the Financial Compensation Scheme.

Transcript of call between a potential LCF investor and an FCA call handler. [C12 2.36]

FCA action against LCF was limited to watering down their misleading advertising

The FCA first contacted LCF with concerns over how its bonds were being marketed in January 2016. At the time LCF’s website claimed LCF was “100% protected”. This was amended following the FCA’s intervention.

Despite LCF’s misleading promotions, the FCA took no follow-up action to verify a) that all LCF’s investors qualified as high-net-worth and sophisticated and that it could produce evidence to confirm this, and b) that it was lending investor money to a diverse portfolio of SMEs as it claimed. A cursory investigation would have revealed that neither was true, and led inevitably to LCF being shut down before it caused £237 million in investor losses.

The FCA’s previous intervention into LCF’s misleading financial promotions were not flagged up during LCF’s application for FCA authorisation. [A8 10/5/16]

Further FCA intervention into LCF’s misleading financial promotions took place in September 2016, this time over lack of past performance disclaimers and warnings about the illiquidity of the investment. Again there was no follow-up after LCF mollified the FCA by amending its website. [A8 Sep16]

In January 2017, LCF disclosed to the FCA that it paid 25% commission on funds invested by bondholders. This commission was not disclosed to bondholders. The FCA apparently didn’t see anything alarming about this. [A8 26/1/17]

In October 2016, LCF applied for permission from the FCA to hold client money. In a dim corner of the FCA’s collective mind, a lightbulb went on: “why would a firm dealing with corporate finance want to hold client money?” This led to LCF being subjected to an “Enhanced” risk assessment process (the 2nd most rigorous out of 4 classifications), during which the FCA asked detailed questions of LCF. In June 2017, LCF threw in the towel in its attempt to gain permission to hold client money.

In response, the FCA downgraded LCF to the “Standard” risk channel (the 2nd least rigorous out of 4) and from then on accepted all LCF statements and responses at face value in regard to its application for regulatory permissions, including in relation to the security of its loans. [C9 6.9]

The FCA consistently treated LCF’s unregulated bonds as not its problem

The report finds that, in the multiple times that the LCF crossed FCA desks, it repeatedly failed to examine LCF’s unregulated business or consider the investment scheme holistically (as a whole). [C2]

In the wording of the report, the “FCA’s approach to its regulatory perimeter was unduly limited” and “the FCA did not sufficiently encourage its staff to look outside the Perimeter when dealing with FCA-authorised firms such as LCF”.

The “regulatory perimeter” is internal code for the FCA’s cultural attitude of “if it’s unregulated it’s not our problem”. As per the statutory objectives given to the FCA, unregulated investment schemes promoted to the public very much are the FCA’s problem, and the Financial Services and Markets Act specifically empowers the FCA to act on such schemes, using court action if necessary where its statutory powers are insufficient.

FCA staff members responsible for reviewing LCF’s application for regulatory status had no accountancy qualifications, and training to analyse company accounts was “on-the-job”. (I.e. non-existent; when it comes to authorising financial firms so they can promote themselves directly to the public, doing the job with no training is not training.) [C2 2.6a]

According to a supervisor, there is little training on how to identify financial crime within the FCA’s Supervision division. [C2 2.6b]

LCF partly fell through the net because responsibility for its regulation had been transferred from the Office of Fair Trading (which formerly regulated consumer credit) to the FCA. 50,000 such firms were subject to a “limited strategy”. As a result, from 2014 to early 2019, LCF was subject to no proactive supervision by the FCA. [C2 3.5]

The FCA failed to see anything untoward about the fact that LCF was generating no revenue from the regulatory activities it had applied for permission to do. (This was, of course, because LCF applied for FCA authorisation purely to use it as a “seal of approval”, and to allow it to access the ISA market.) [C2 3.2]

The FCA treated LCF’s repeated breaches of financial promotion rules as separate cases, rather than considering whether these repeated breaches could indicate poor systems and controls or even misconduct. [C2 3.7b]

A number of members of the public contacted the FCA identified correctly

that LCF’s literature was misleading

that LCF’s published accounts raised questions over its financial viability, contradicted LCF’s claims to have loaned money to numerous SMEs,

that LCF had conflicts of interest between itself and connected companies

Whenever these reports from the public were escalated, they continually foundered against the FCA’s “it’s unregulated so it’s not our problem” regulatory perimeter.

An internal FCA report from 2013 identified that there was a risk of minibonds such as LCF’s slipping through the cracks. “In addition, if they [are] not sold on an advised basis, it seems that it would not be a sector team issue. This is a risk as there is a possibility that this issue is overlooked as each sector might consider it beyond the scope of their remit.” [Translation: nobody’s been given the job of looking at minibonds so every FCA team will say “more than my job’s worth”.]

The report also noted the increasing amount of money that was going into minibonds, and that misselling of minibonds via lack of risk warnings was endemic. It is unclear whether this report was ever acted on by or even reached senior FCA management. [C7 2.2]

There is no evidence that the FCA took any steps to check whether LCF’s bonds were sold only to high-net-worth and sophisticated investors. [C7 2.6]

FCA senior bureaucrats shirk responsibility

In its response to the Investigation, the FCA claimed that the Investigation was unfairly using the benefit of hindsight. [C1 10.3b]

As the Investigation notes, this is of course false, as per its accountant’s report which showed that there was more than sufficient cause for further investigation and intervention as early as 2016.

The FCA also claimed that it would have taken a forensic accountant to spot the red flags in LCF’s financial information. [C9 6.21]

As the Investigation notes, this is also patently incorrect. Plenty of lay members of the public managed to spot the issues in what little financial information LCF released, including the lack of evidence for its claim to have loaned out hundreds of millions to SMEs with asset security. Many took their concerns to the FCA.

The FCA ignored red flags in LCF’s provided financial information, ignored its own interventions into LCF’s misleading advertising, and has then had the nerve to claim nobody could have seen it coming at the time. It’s a bit like running your car over someone and then claiming “well it’s easy to say I should have seen them now they’re in the rear view mirror”.

The FCA claimed “the draft report had not adequately recognised that the FCA must necessarily prioritise and take a risk-based approach”. Or, to translate, “what’s all the fuss about? It’s only a piddly £237 million.” [C1 10.3]

In a paragraph straight out of an episode of Yes Minister, the FCA told the Investigation that it would be wrong to assign responsibility for the failings over the FCA to individuals, on the grounds that a) it might deter people from wanting to be FCA senior bureaucrats, b) that investigations such as these are supposed to focus on institutional failures and not individual ones, c) the very concept of responsibility is ambiguous. [C1 11]

As the Investigation pointed out, this attitude is at odds with the FCA’s own “Statements of Responsibility” and “Management Responsibilities Map”, implemented in 2016 after the Treasury recommended that the FCA should apply the same framework to itself that it applies to the senior management of banks.

For all the failings in the report, the most glaring paragraph to me is the one where it was claimed to the FCA that the concept of “responsibility” is some kind of ambiguous, philosophical concept, ignoring its own Responsibilities Map and the principles it (somehow) expects the UK finance industry to follow.

And where exactly did this come from? A footnote to the report reveals it came from the submission to the Investigation made by erstwhile head of the FCA, current head of the Bank of England, Andrew Bailey. It came from the top.

It appears to be lost on FCA senior management that responsibility and accountability is what they pay you the big bucks for. For many people it is what they pay you minimum wage for (ask any carer).

The FCA’s 2018 intervention into LCF was delayed by fears of being met with a hail of bullets

The FCA’s belated intervention in late 2018, which resulted in LCF being closed to new investment and immediately collapsing, only happened by chance, as a result of an unrelated search on an external database while looking for something else, which turned up a report which identified significant concerns about LCF. The FCA staff member who stumbled upon the document stated “if the document didn’t mention LCF, it’s entirely possible that nobody would have looked at it”.

The report was circulated by the FCA’s Intelligence Team, ultimately resulting to an unannounced site visit in late 2018. [C13 7.12f]

The site visit was initially due to take place on 21-22 November, but was delayed for three weeks because the FCA team responsible felt there was a risk of being met with armed resistance, and stated they would not proceed without police support. The local police force refused to attend as they concluded the risk of LCF meeting FCA bureaucrats with a volley of gunfire was insignificant. Consequently the site visit eventually took place on 10 December. An FCA team member described the delay as “frustrating”. [C13 7.12f]

An FCA team making an unannounced site visit to a Ponzi scheme, yesterday.

The FCA failed to consider taking action to freeze the accounts of LCF, and companies and individuals connected to it, prior to its December 2018 site visit. [C2 3.23e]

Conclusion

Dame Gloster makes a number of sensible recommendations as to how the FCA should reduce the chance of similar scandals happening in the future, and limit the damage when it does. These include better training for FCA call handlers, more effort to consider the whole of a regulated firm’s business when supervising it, more effort by senior management to identify emerging risks, etc etc.

What Dame Gloster does not address, most likely due to limitations placed on her by the Government which commissioned the report, is how we can expect the FCA to follow such recommendations.

When you consider:

the lamely defensive response of the FCA to the Investigation, which suggests that despite a change in leadership, the FCA has been more concerned about loss of face than using the Investigation to identify ways in which it can do better

the repeated and systematic way in which the FCA contrived reasons to file reports and screaming red flags about LCF in the circular filing cabinet under the desk

an environment where members of the Supervision division receive no training in financial crime, and where FCA call centre staff were so poorly coached that they actively endorsed LCF to potential investors

…we have a clear picture of an organisation that is so infested by the cultural attitude of “if it’s unregulated it’s not our problem” that I fail to see how anyone can be confident the FCA will follow the Gloster recommendations, no matter how many mea culpas the FCA and Bailey give.

If the Government had replaced Andrew Bailey with an outsider with a reputation for a pro-active and activist approach, we might have grounds for optimism that change could come from there. But they went with a lifelong mandarin in Nikhil Rathi, so we’ll have to hope he has hidden depths.

Today marks the third anniversary of Bond Review’s first ever article, our review of London Capital & Finance, which went on to collapse owing £240m to investors.

So far Bond Review’s three years have seen:

114 reviews of high-risk, mostly unregulated investments promoted to the public

380 total articles keeping you up to date with news, developments and occasional commentary on the unregulated investment world

13 legal threats (not counting duplicate threats from the same scheme)

As ever, thank you to those who have donated already. The knowledge that somebody values what I’m doing is as important than the money towards the hosting costs.

Highlights of 2020

In the holiday tradition of reminiscing on the year just gone (if we really must), here’s a roundup of some of the bigger articles of 2020:

As a refresher, OneCoin took in £4 billion from investors in exchange for “OneCoins”, its made-up cryptocurrency. OneCoins were given an imaginary and ever-increasing value, which investors could cash out to a very limited degree via an exchange. These withdrawals were funded by new investors’ money, in the classic Ponzi scheme fashion.

The scheme collapsed in 2017 when it ran out of money and the exchange was shut, although OneCoin limps on to this day as a pyramid scheme, despite the arrest or disappearance of virtually all its former top brass.

In 2016 one of OneCoin’s promoters / victims had a Road to Damascus moment and started making videos calling out OneCoin as a scam. OneCoin hired Carter-Fuck to send letters threatening her with libel action.

McAdam stood her ground, declined to remove her videos and heard no more from Carter-Ruck.

So far, still so cookie-cutter cryptocurrency scam.

Where it gets interesting is that Private Eye notes that the Financial Conduct Authority issued a scam warning against OneCoin in September 2016.

Shortly after Carter-Ruck sent its SLAPP attempt to McAdam, the FCA withdrew its warning.

The FCA has refused to comment on whether the removal of the OneCoin scam warning followed any lobbying from OneCoin’s end.

Yet nonetheless, somehow and for some reason it was persuaded to remove an entirely factual scam warning.

Thanks to the BBC’s “Missing Cryptoqueen” podcast, we now know the answer to the question “Did the FCA spinelessly cave in to a half-baked Ponzi scam” is “yes”.

[22:28 Gary Gilford, a lawyer for OneCoin mastermind Ruja Ignatova] At the time, when I think Carter-Ruck and Chelgate were involved, the Financial Conduct Authority put out a warning on their website, about anyone doing business with OneCoin and OneLife.

So Carter-Ruck and Chelgate were writing to the Financial Conduct Authority.

Whatever they did, was convincing enough for the FCA to take the (OneCoin) notice down. […]

[24:42, Simon Harris, former Chelgate employee] In the weeks prior to my arrival (at Chelgate) on August 2017, there was a warning on the … FCA’s website.

And Chelgate worked with Carter-Ruck to pressurize (the FCA), to weaken their public stance on OneCoin.

The FCA’s withdrawal of the scam warning led directly to further investor losses, as OneCoin promoters used the withdrawal as “proof” that OneCoin wasn’t a scam.

[26:34 Ken Labine, OneCoin promoter] If they (the FCA) still thought we were a fraudulent company, OneCoin, then guess what; that warning’s not removed. Game over.

The FCA made no visible attempt to stop OneCoin promoters portraying the removal of the scam warning as approval.

It has bleated that it took the scam warning down because OneCoin was not carrying out any regulated activities.

The FCA does not regulate cryptocurrency assets, and therefore it could not take this matter further.

This, of course, is bollocks.

OneCoin investors handed their money to OneCoin in order to invest in their made-up points, which were tracked via an SQL database. They were able to cash out a return for as long as OneCoin had enough investors’ money in the system to honour withdrawals. Investors took no part in the day-to-day running of OneCoin, simply sat back and watched their “coins” increase in value and/or attempted to make a return by taking withdrawals (paid with other investors’ money).

This pooling of investors’ money to pay out returns, with no day-to-day involvement by investors, represents a collective investment scheme. Promoting a collective investment scheme to UK invstors requires authorisation from the FCA.

The fact that the scheme in question was a Ponzi scheme with no real underlying investment is irrelevant. That investors handed over money for coins tracked via an SQL database rather than, say, car parking spaces is irrelevant. The essential elements of a collective investment scheme are the pooling of investor money and the lack of day-to-day involvement by investors, both of which were true of OneCoin.

There are plenty of Ponzi schemes which manage to conceal their nature from regulators. London Capital and Finance, for example, could not be publicly called out as a Ponzi scheme until after it had collapsed, and the administrators had revealed that its half-billion-odd of asset security didn’t exist, and it had no income-producing assets funding returns to investors.

OneCoin was not one of them. It operated openly as a Ponzi scheme from the beginning, with no serious attempt to pretend that it had any source of funds with which to honour withdrawal requests other than investors’ own money.

And the real scandal is not that the FCA’s scam warning was entirely factual, and trivially proven as such from facts publicly available at the time, but that this didn’t even actually matter as the FCA has statutory immunity from being sued.

Suing the FCA for libel for publishing a scam warning against you requires persuading a court not just that you aren’t a scam, but that the FCA acted unlawfully or in bad faith, a virtually insurmountable bar which OneCoin was never going to clear.

The good news here is that the OneCoin scandal gives the FCA a golden opportunity to prove it has actually changed under new head Nikhil Rathi.

By publicly naming the official who gave OneCoin the green light to scam UK investors, sacking them for gross misconduct (if they are still there), and giving an unconditional apology to all UK OneCoin victims. (An apology with zero compensation – the UK taxpayer should not underwrite foreign Ponzi schemes.)

Anything less will confirm that the FCA still views consumer protection as an annoying and tedious distraction from its real job of high-level thought leadership.

On 20 July the Treasury proposed a tweak to the rules surrounding promotion of minibonds and other high-risk unregulated investments sold to the public.

Currently, any firm which is authorised by the FCA, no matter what they are authorised for, can approve a financial promotion for an investment security, giving the investment the green light to be sold to the public.

It would not be fair to say that to be able to flog an unregulated investment security to the public, you need to cut out two tokens from a packet of breakfast cereal and send it to the FCA. What you need to do is hire someone else who at some point has sent in their tokens, and get them to approve your adverts.

Under the Treasury’s proposal, firms would need specific consent from the FCA to be able to sign-off financial promotions for unauthorised firms.

The Treasury’s consultation however leaves two glaring holes in the UK regulatory framework unaddressed:

unauthorised firms would still be free to run around Facebook, Google Ads and other advertising platforms running financial promotions, in the absence of any attempt by the FCA to clamp down on them

unregulated firms whose investments are advertised by the public would still be able to use “smaller company” exemptions to avoid filing full accounts and disclosing their financial position to any meaningful extent.

The Treasury seems to think the problem of billions of pounds of UK investor wealth being destroyed by inappropriate unregulated investments can be solved by taking the hoop that unregulated investment opportunities have to jump through in order to be able to enter this chaotic Wild West, and raising it slightly higher.

Without any meaningful attempt to stop such investments being marketed to unsophisticated investors, there is little evidence that this will have much of an effect.

Illustrating the scale of the problem, the Times revealed that, according to a Freedom of Information request, the FCA did not prosecute even one firm over misleading financial promotions between 2013 and 2019, fined only three groups and individuals, and did not remove a single firm’s permissions.

The FCA bleated that over 1,000 financial promotions had been amended or removed, but as promotions are often time-limited anyway, this is irrelevant unless action is taken to deter further misselling. It is equivalent to the Advertising Standards Authority’s famously pointless catchphrase “The advert may not appear again in its current form”.

The FCA’s failure to prosecute or shut down any firm between 2013 and 2019 suggests either

there wasn’t any problem with systemic and habitual misselling of investments between 2013 and 2019

the FCA doesn’t give a shit.

If anyone seriously believes the first, help is available, talk to your GP.

It would have been big news if the FCA had come up with any reasons why promotion of ultra high risk unregulated minibonds to retail investors should be allowed to start up again.

The FCA’s announcement glossed over the fact that even before the “ban”, high risk minibonds should never have been promoted to unsophisticated retail investors to start with.

To take the £230m potentially lost in London Capital and Finance as an example, the FCA had more than enough ammunition to stop LCF’s bonds being sold to retail investors without a general ban on minibonds, long before the scheme collapsed in late 2018.

LCF was systematically and brazenly promoted to UK retail investors via Google Ads and websites which misleadingly compared the bonds to FSCS-protected cash accounts. Its own website claimed at one point that it had “£685.3m assets held as security” to cover £215m of investor funds, which we now know from administrators’ reports was completely false.

The FCA’s Second Supervisory Notice in late 2018 belatedly confirmed this, at the same time the FCA sealed LCF’s fate by closing it to new investment. It could have done this at any time since 2014, when whistleblowers from the industry repeatedly tried to bring LCF to the FCA’s attention.

But the FCA did nothing. Not because there wasn’t a general minibond advertising ban in place. But because of the FCA’s belief that unsophisticated investors putting £230m they almost certainly can’t afford to lose in high-risk schemes doesn’t matter, on the grounds that it’s only £230m.

£1.4 billion still at risk

The FCA revealed that retail investors have £1.4 billion invested in “speculative illiquid securities”, a catch-all term for minibonds, bonds “listed” on backwater exchanges with almost no trading, and similar products. This is presumably even after £1 billion was lost from such schemes in 2019 alone.

The FCA acknowledged in December 2018 that its original temporary ban would result in some unregulated schemes collapsing due to new investment drying up.

To quote the Texas Chainsaw Masscare, who will survive and what will be left of them?

Meet the new boss

In other regulatory news, the Chancellor at last appointed a new permanent head of the FCA this week to replace the hapless Sir Andrew Bailey, appointing former civil servant and LSE head Nikhil Rathi.

Rathi is a lifelong mandarin, having been a private secretary to Tony Blair and then Gordon Brown from 2005 to 2008, then spending five years at the Treasury. He then spent 5 years at the London Stock Exchange, nominally a private company but in reality, being the gatekeeper between the private sector and retail investors, part of the UK financial regulatory skyline.

In his statement, Rathi listed his priorities as “vulnerable consumers, embracing new technology, playing our part in tackling climate change, enforcing high standards and ensuring the UK is a thought leader in international regulatory discussions”. Which, the nod to “vulnerable consumers” aside, is not what anyone hoping for a more active FCA to stem the tide of consumer losses and Financial Services Compensation Scheme levies wanted to hear.

Rathi’s belief that the priority of a country which makes up 3% of world GDP should be to become a “thought leader in international regulatory discussions” suggests we are in for more conferences about excellent sheep.

Earlier this year Hong Kong Securities and Futures Commission chairman Ashley Alder was being widely linked with the job, but either he decided to stay in Hong Kong, or the UK Government decided that someone with a reputation for an activist and interventionist approach would scare the horses.

So the signs are that Rathi isn’t going to be picking up the six-shooters that Martin Wheatley left behind in 2015 any time soon.

After being denied compensation from the Financial Services Compensation Scheme (other than a tiny handful of exceptions,) London Capital & Finance investors have raised money via crowdfunding to launch a judicial review.

As at 23rd April the campaign had already raised £7,833, exceeding its initial £7,000 target. Technically the campaign is to fund the judicial challenges of only the four LCF investors on the creditors’ committee, but if their challenges succeed, this will surely set a precedent for the rest.

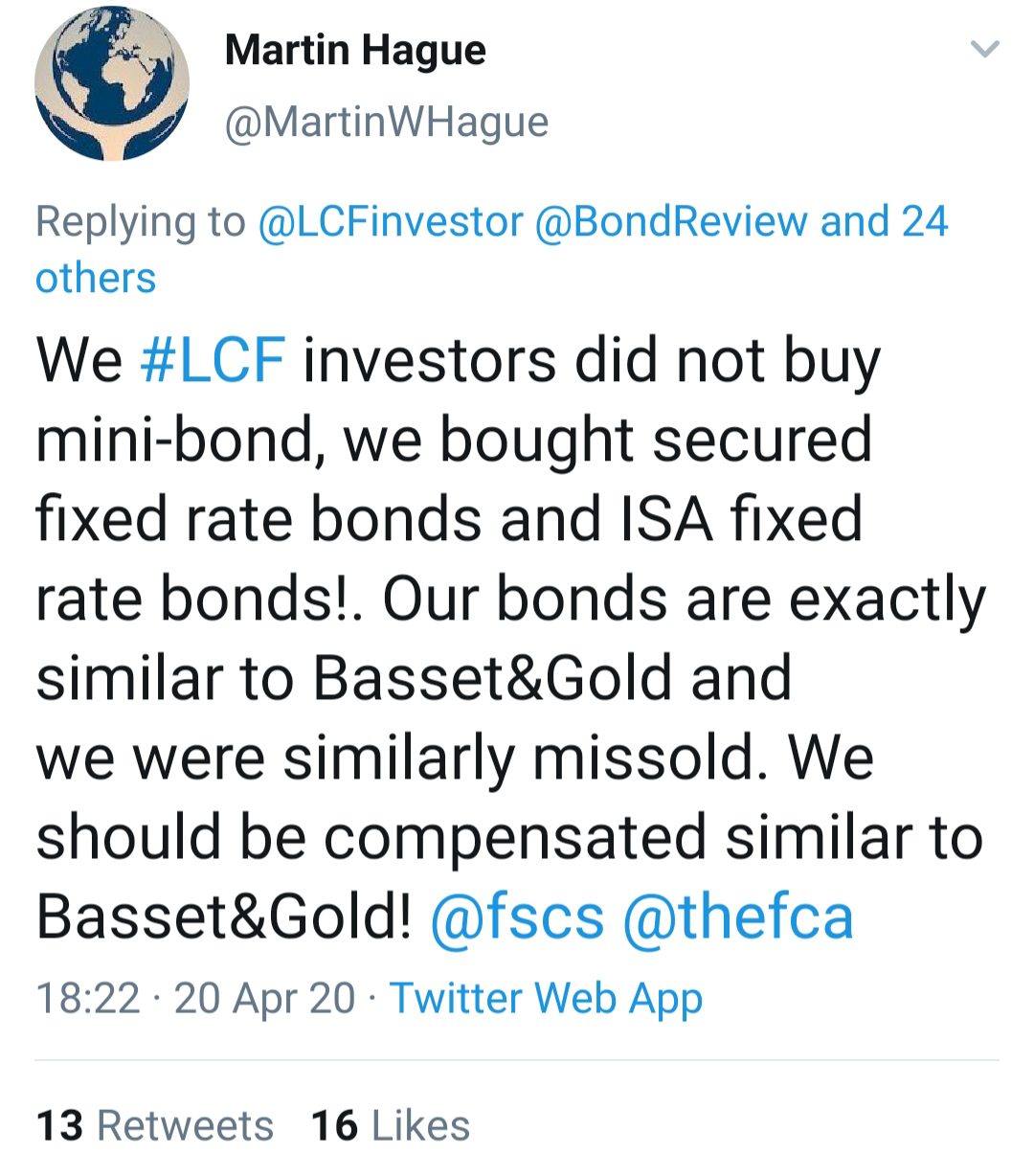

London Capital & Finance investors have been both emboldened and enraged by the FSCS’ early indications that it will bail out investors in fellow collapsed minibond scheme Basset & Gold, which went into administration on 1 April.

We have concluded there will be some customers who were given misleading advice by LCF and so have valid claims for compensation. However, we expect that many customers will not be eligible for compensation on this basis.- Jan 2020 FSCS announcement

By contrast, Basset and Gold investors have been given a far more positive indication by the FCA that compensation will be payable on the grounds of misselling.

The FSCS has determined that many investors have a good prospect of claiming compensation.– Apr 2020 FCA announcement

The distinction between LCF and Basset & Gold is that LCF had one FCA-regulated company, which both issued the investment and the investment literature, while Basset & Gold had two separate companies, one of which was not FCA-regulated and issued the minibonds, the other of which was FCA-regulated and issued the investment literature.

Which is of course entirely meaningless from the perspective of an ordinary retail investor. Nothing was stopping LCF from setting up two different companies instead of one, and keeping the misselling separate from the bonds themselves, except that they didn’t think of it (or care).

It is therefore not a surprise that the Basset & Gold collapse has given LCF investors fresh hope for compensation.

Commentary

My own money would be on the regulator and the Government as a whole eventually figuring out a Barlow Clowes / Equitable Life solution – i.e. compensation paid, not in line with arcane FSCS rules that even they don’t seem to understand, but on a one-off basis in recognition of regulatory failures which allowed LCF to run longer than necessary and lose more ordinary savers’ money than was necessary. This is what happened in recognition of regulatory failures over Barlow Clowes (in the 80s) and Equitable Life (in the 90s).

The litany of regulatory failures by the FCA is not seriously disputed. The FCA gave London Capital & Finance the “CAT standard” of FCA registration and ignored the systematic misselling of its investments for a further 3 years afterwards despite numerous attempts by outsiders to blow the whistle. As the FCA CEO in charge at the time has now been kicked upstairs to the Bank of England, the FCA is now free to issue regular mea culpas and lessons will be learneds.

Whether the FSCS or the Treasury pays compensation makes little difference as the general public pays either way; nearly everyone pays taxes and nearly everyone pays FSCS levies via use of financial services.

The main obstacle in the way of compensating LCF investors is moral hazard; the fear that if LCF investors are compensated, it will encourage others to invest in schemes paying unrealistically high returns for supposedly safe investments on the assumption that they’ll get their money back if it goes wrong.

The obvious counterpoint to the moral hazard argument is that the exact same argument applied to compensation for Barlow Clowes, the exact same argument applied to Equitable Life, and the exact same argument applies to Basset & Gold. In the first two cases the moral hazard argument was beaten by the argument that such a monumental failure of regulation and Government should result in compensation, and improvements to the regulatory system to ensure it doesn’t happen again.

There is a better way than whataboutery for LCF investors to counter the moral hazard argument; campaign not just for compensation but for the UK to bring the UK’s securities laws out of the 1920s and require all investment securities offered to the public to be regulated by the FCA, as is the case in the US.

If it becomes more difficult to open unregulated investment schemes and promote them to the public, this would counteract the moral hazard incentive to open and invest in them. It offers the taxpayer’s purse a quid pro quo – a one-off compensation payment (trivial in the grand scheme, especially now) in exchange for less economic damage in the future.

Or we could just do nothing and wait for the next wave of unregulated investment scandals, some of which, like Basset & Gold or investments recommended by dodgy FCA-regulated advisers, will inevitably fall onto the public purse. As my old ma always said, if you keep doing what you’ve always done, you’ll keep getting what you’ve always got.