Since early 2018, investors in MJS Capital (now Colarb Capital) have experienced issues with having interest paid on time and receiving their capital back when due.

Numerous comments have been left on this blog from frustrated and often frightened investors trying to find out what action they can take.

An investor action group has been set up on Facebook at https://www.facebook.com/groups/mjscapital/ to help investors come together, share information, and find a way forward. The group is “closed”, which means that anything posted in the group will only be visible to those who have been allowed to join.

I thought long and hard before forming this group, given that I am essentially an uninvolved observer. However, numerous MJS Capital investors have commented on or emailed my blog looking for answers, and for every person who commented, there will be many more who have read my posts without speaking out. For the last nine months MJS Capital investors have been scattered across myriad blog posts and websites shouting into the void. I see no point in 2019 being more of the same.

It is highly likely that MJS Capital investors will be targeted by unscrupulous individuals seeking to exploit them a second time, and whether or not they join the action group, I recommend they read Action Fraud’s advice on fraud recovery fraud and beware throwing good money after bad.

Tempus Magazine was a luxury lifestyle magazine first published in 2012. If you liked yachts, luxury holidays and pictures of watches (lots of pictures of watches), Tempus was the magazine for you.

Update 6.12.18: Since Issue 47 (April 2017), every issue of Tempus has included the text “(C) Tempus Media Limited” on its contents page. However, the director of Tempus Media Limited (a former MJS Capital director) has contacted us to say that in actual fact, “Tempus Media Limited does not run and never has run Tempus Magazine.”

The company which actually runs Tempus Magazine is, according to the director of Tempus Media Limited, Tempus Media (London) Limited. Tempus Media (London) currently has one director, MJS Capital CEO Shaun Prince, who took over in October 2018 after the previous directors left. The company has been owned by Shaun Prince’s girlfriend since September 2018.

Still with us? Good. What is not in dispute is that Tempus Magazine was controlled by MJS Capital since a “sponsorship” arrangement was announced in a November 2016. This arrangement was referred to by Tempus as “sponsorship”, but having the same CEO as your “sponsor”, substantial influence on editorial output (see below), and having an MJS Capital director eventually appointed as director of the publishing company goes well beyond sponsorship.

I believe Tempus Magazine is now defunct, originally for three reasons: Tempus’ website (tempusmagazine.co.uk) is now down and has been for some days; the magazine has not published an issue for three months, despite being two-monthly; and the third was the recent application to strike Tempus Media (not London) Limited off the Companies House register. Apparently the third event actually has nothing to do with the magazine ceasing to publish, but the first two seem grounds enough to believe that Tempus is no more. It is also noticeable that a month after the last issue was published, Tempus Media (London) Limited’s two directors both left, and were replaced by Prince.

With Tempus Magazine apparently no more, let’s take a moment to reminisce about its history under its new owners.

November 2016:Issue 42 announces MJS Capital’s “sponsorship” of Tempus magazine.

In an interview, former MJS Capital director Martin Westney claims that MJS Capital’s bonds are “very low risk”.

Tempus: So there must be an element of risk somewhere?

Westney: Our investment products carry a very low risk. Not only are our bonds insured but the method by which we create capital growth is that of arbitrage.

No iceberg jokes please.

March 2017:Issue 46 is the first issue to name Shaun Prince as the new CEO of Tempus Magazine. Prince even gets his hands dirty – and perhaps frost-bitten – by writing at least a couple of articles. In one he takes a luxury trip to Antarctica, in another he reviews a luxury hotel in Berkshire. (There may be more articles by Prince, but I didn’t read the issue cover-to-cover, as there’s only so many pictures of watches I can handle.)

An advert for MJS Capital stretching from page 106 to 108 claims that its bonds are “low risk, high return”.

September 2017: Tempus’ website publishes an article by Lucy Allen headlined “The simplicity of arbitrage: Investors bruised by recession could find these investments to be a safe haven”.

“These investments”, of course, refers to MJS Capital’s bonds.

MJS Capital is one such company setting new standards in security structuring and taking advantage of pure arbitrage. This means that it’s able to offer its clients an above average return. The firm is aligned with multiple security and commodity traders who work within the banking sector. Using large credit lines, MJS generates profits by pre-selling the assets that it purchases.

It’s a low risk strategy that’s been very well received in the square mile of London due to its simplicity, and it’s one that potential investors should explore for themselves. The rewards are there for those willing to approach arbitrage with an open mind.

Nowhere in the article is there an “advertorial” declaration or disclosure of MJS Capital’s effective ownership of Tempus magazine. The article goes well beyond merely discussing the existence of MJS Capital’s investments, and clearly induces investors to invest, making it a financial promotion. Neither Tempus Magazine nor MJS Capital has ever been authorised to issue financial promotions by the FCA.

Note that I am not just picking on Tempus with the benefit of hindsight. Describing MJS Capital’s bonds as “low risk” or a “safe haven” was blatantly misleading with the benefit of plain old sight. “Low risk” is universally recognised to mean an FSCS-protected cash account, diversified regulated stockmarket funds are considered “medium risk” to “high risk” depending on their volatility, and unregulated corporate loan notes with a material risk of total loss are quite clearly well beyond high risk.

October 2017: Issue 53 is devoted to “The disruptors of the new wealth landscape”. The cover image is a colourful photo of London’s skyline which some MJS Capital investors will recognise from MJS investment literature.

One of the first articles is devoted to Shaun Prince’s attempt to launch a fund which would combine investment with access to private jets, yachts and other luxury vehicles. The fund would invest collectively in luxury vehicles and would allow investors to rent them for a period. Timeshare for private jets, essentially.

Tempus: What inspired you to launch the MJS Capital luxury fund?

Shaun Prince: MJS Capital has been quietly generating good profits for nearly three years,

[Brev: So quietly its own accountants didn’t notice. MJS Capital’s September 2017 accounts show a net loss of £800,000 on turnover of £6.5 million from April 2016 to September 2017, and a loss of £75,200 from incorporation in March 2015 to March 2016.]

…so after lots of hard work I felt it was time to enjoy some well-earned rest. My initial idea was to buy a yacht, but the thought of buying one outright seemed too much, especially as they are such an expense to run full-time. My second option was to charter but I couldn’t bring myself to pay the inflated chartering costs. This is where I spotted an opportunity to combine my finance background with luxury living and create a new solution for people facing a similar dilemma. This is how the ‘luxury fund’ was born.

Prince had his eye on the yacht Sarastar, which is still up for sale for those with 50 million euros burning a hole in their pocket. Prince has recently claimed to the Evening Standard that MJS Capital has raised £20 million from investors. His aim to raise enough money from investors in the new ‘luxury fund’ to buy Sarastar among other yachts, plus 3-5 private jets, plus a pool of supercars valued at over £200,000 a piece, therefore seems highly ambitious.

It’s very simple to understand. Funds raised into the fund are split 50/50 – 50% is used as a deposit to purchase the luxury assets and the remaining 50% is taken out in the form of a loan. This leaves us with 50% to be invested into one of our arbitrage trades.

…During the period of investment they can use the fund’s luxury items on a points-based system.

Despite Prince’s claim that investor demand for the fund was “staggering” and that the launch of the fund had been brought forward as a result, as far as I can tell the fund didn’t take off. Interested investors are directed to the main mjs.capital website (now replaced by colarb.capital), but there has been no sign of the luxury fund on either domain for a while.

This issue also features a story which “lifts the rope” on MJS Capital’s private dinner at the Tower of London.

The evening began with a champagne reception inside the Fusiliers Museum, followed by a three-course dinner during which time-honoured traditions such as the passing of the port and toasts to the Queen were carried out.

A massive weapon, pictured here with a gold-plated AK47.

Among the tasteful attractions of the evening was a display of artworks by Bran Symondson, including a gold plated AK47.

Those with a ‘golden ticket’ were chauffeur driven through London to the Wellesley, Knightbridge, where the cigar terrace was turned into an opulent setting for after dinner digestifs. Cigar and cognac connoisseur Giuseppe Ruo hosted a masterclass on pairings that guests could sample – Hennessy XO Cognac paired with Dipolatico Cigar Excelencia and Rum Zacapa Xo paired with San Louis del Rey Marquez – before mingling into the small hours.

September 2018: What appears to be Tempus’ final issue, #59, is published – although there is no mention of the magazine’s closing in the editorial. The cover proclaims it to be a “Wealth Edition”.

Despite its ongoing banking issues, MJS runs another double-page advert in the magazine, featuring the familiar sunset shot of London but no text.

An article on alternative investments suggests six novel asset classes for investors to consider: cryptocurrency, cannabis, collectibles, classic cars, film/television and “supertoys” (supercars and luxury yachts). The article is contributed by Graham Rowan of Elite Investor Club.

Under “supertoys”, the writer plugs a company launching a “bond” which buys a portfolio of supercars, luxury yachts and private jets. The bond uses part of investors’ money as a deposit and takes out a loan to cover the rest of the funds needed. The remainder is invested “in a specialised bond that produces strong returns from arbitrage in the foreign exchange markets”. Investors are awarded points which they can use to trade for time with their chosen supertoy.

Sounds rather familiar, doesn’t it? Yet this bond is apparently nothing to do with MJS Capital; the company offering the bond is P1 International. But there are remarkable similarities not just in the general concept, but the structure of using part of investors’ funds as a deposit and taking out a loan to buy the “supertoys”, investing the rest in arbitrage to pay the loan interest, and giving points to investors to allow them to borrow the fund’s yachts / cars / planes.

P1 International is a car club which has been around for quite a while. It was originally founded in 2000 by Formula 1 Champion Damon Hill, Michael Breen and a number of other directors as P1 International Limited. Damon Hill was bought out by Breen in 2006.

In 2009 P1 International Limited went bust (no shame in that, all the cool kids in the alternative assets world were going bust in 2009). It was reincarnated by Breen as P1 World LLP, which bought the assets of P1 International Limited from the administrators, sans £1.5 million worth of cars which were mortgaged to Lombard North Capital and Barclays Asset Finance.

Has P1 International nicked Shaun Prince’s idea? Probably not, as it seems unlikely that Tempus – still owned by MJS Capital and helmed by Shaun Prince – would promote P1 International if they hadn’t picked up the baton with Prince’s blessing.

In any case, despite the Tempus article directing readers to p1international.com for more information, I was unable to find anything about a bond issue.

End of the line

Is this the end of Tempus Magazine’s six year history? The magazine has changed hands more than once in the past, so it wouldn’t be a surprise if it eventually resurfaced under new ownership. Judging by the number of luxury brands who advertise in it, there is clearly value in its readership.

Hopefully if there is a new owner, they will be more cautious about their choice of investments to promote.

The article focuses on the worries of a handful of investors who loaned money to MJS Capital via its bonds, have not received interest on time, and have attempted to redeem their bonds. Some have succeeded in redeeming their bonds after a long delay, others are still waiting to receive their money.

CEO Shaun Prince claims that some of these investors are lying about being MJS Capital investors. The investors in question provided documentation to the Evening Standard proving they are in fact investors.

When confronted by his customers’ complaints, Prince said some investors would “lie through their teeth” when it came to getting their money back and asked: “How do you know they’re real investors?” The investors deny they’re lying, and some sent the Evening Standard supporting documentation to their case.

Prince also claims that investors are being unreasonable for wanting to redeem their bonds early. The Evening Standard notes that MJS’ own literature says that early withdrawals are allowed subject to 30 days’ notice and a penalty. In at least some cases, even this shouldn’t be necessary, because MJS Capital’s original investment terms & conditions makes it clear that if a “Default Event” occurs, which includes the late payment of interest, the bonds become “immediately repayable at par”. No penalty, no notice period.

This distinction is largely moot because Prince has admitted to the Evening Standard that MJS Capital is not currently able to repay the bonds anyway.

Prince said that was subject to the company being able to repay it.

Nonetheless, I fail to see how investors are being unreasonable by wanting to stick to the terms under which they handed their money over.

Banking issues continue

MJS Capital is sticking to the story that the failure to pay interest and redemptions on time is a result of MJS falling foul of their banks’ anti-money-laundering rules, which in turn is due to the former presence of Liberal Democrat peer Lord Razzall on their board, plus “a payment from a wealthy client with a Middle East bank account”.

It is now eight months after Lord Razzall resigned from the board in an attempt to resolve these issues.

Prince has blamed the investors for their situation, saying that if they weren’t sophisticated investors they shouldn’t have invested in the bonds in the first place.

He blamed brokers for introducing naive investors into the scheme, saying it was made clear in the documentation that the bonds were only for sophisticated investors. “Why are investors self-certificating as sophisticated investors?” he asked. “That’s the real question here.”

A firm which wishes to rely on any of the self-certified sophisticated investor exemptions (see Part II of the Schedule to the Promotion of Collective Investment Schemes Order, Part II of Schedule 5 to the Financial Promotions Order and COBS 4.12.8 R) should have regard to its duties under the Principles and the client’s best interests rule. In particular, the firm should consider whether the promotion of the non-mainstream pooled investment is in the interests of the client and whether it is fair to make the promotion to that client on the basis of self-certification.

For example, it is unlikely to be appropriate for a firm to make a promotion under any of the self-certified sophisticated investor exemption without first taking reasonable steps to satisfy itself that the investor does in fact have the requisite experience, knowledge or expertise to understand the risks of the non-mainstream pooled investment in question.

Whether this particular buck can be passed to MJS Capital’s brokers depends on whether leaving it to unregulated introducers (such as Direct Property Investments, who previously promoted MJS Capital’s bonds, and are quoted in the article) can be considered “reasonable steps” in the regulatory sense.

Prince’s last quote in the article is “As far as I am aware all of our investors are fine”. Which given what has gone before is dangerously close to Comical Ali territory.

This follows at least one (possibly two) other MJS Capital shell company/ies being put into administration / liquidation earlier this year, as covered here a couple of weeks ago.

MJS Cap Ltd director Martin Westney filed the application earlier this month. According to its (unaudited) March 2018 accounts, MJS Cap Ltd was at that point the shelliest of shell companies with no assets other than 4 pounds in share capital. (Although MJS Capital‘s September 2017 accounts said that MJS Cap Ltd held £26,871 in cash on MJS Capital’s behalf – but this was six months earlier.) Its dissolution would therefore seem a formality.

Apparently this particular attempt to resolve MJS Capital’s problems with its banks hasn’t worked.

Shaun Prince claims Bond Review is run by a boiler room in Bournemouth

Neither Shaun Prince nor MJS Capital has attempted to contact this journal directly (nor vice versa), but apparently he is not unaware of our coverage. The Evening Standard’s Jim Armitage tells me that Shaun Prince has got it into his head that Bond Review is run by a boiler room outfit based in Bournemouth.

(For those unfamiliar with these terms, a “boiler room” cold-calls prospective investors to sell them worthless investments. Anyway, back to MJS Capital.)

I think the ludicrousness of this allegation can mostly speak for itself. But for the record, if I was going to run a boiler room outfit, it wouldn’t be in Bournemouth.

A shell company connected to troubled unregulated bond issuer MJS Capital has gone into administration.

MJSC Marketing Limited (it will not be lost on our readers that MJSC has the same initials as MJS Capital) was incorporated in October 2017 by Nigel Anthony Peck.

Nigel Peck was listed in MJS Capital’s investment literature as a member of the Advisory Board. His exact role was not specified.

On 25 October MJSC Marketing Limited was put into administration. Paul Cooper and Asher Miller of David Rubin & Partners have been appointed as administrators.

What role MJSC Marketing played in MJS Capital’s dealings is not clear. The company did not even survive long enough to file annual accounts. Even its SIC code is “82990 – Other business support service activities not elsewhere classified“.

Another business with a remarkably similar name has gone into liquidation. MJSC Investments Limited was incorporated in May 2015 as MJSC Retail Limited (a couple of months after the main MJS / Colarb company) and changed its name to MJSC Investments Limited on November 2016.

In July 2018, one of MJSC Investments’ creditors (logistics giant Kuehne + Nagel) petitioned the courts to liquidate the company, which was granted. Nobody turned up in court to represent MJSC Investments Limited. The company is currently in liquidation, with Dentons UK and Middle East LLP appointed as liquidators.

Despite the remarkable coincidence of the name, I have been unable to verify that MJSC Investments Limited is an MJS Capital company. The director and 90% shareholder at time of incorporation was Frenchman Philippe Vladimir Davso. In July 2016 Davso’ shareholding and directorship was transferred to Israeli Eliyahou Arama, who was 19 at the time.

I have been unable to connect either Davso or thrusting young business tyro Arama to MJS Capital in any other way, which is why I can’t verify that MJSC Investments Limited is an MJS Capital company. Still, quite a coincidence that it should share the MJSC badge and go bust at around the same time as MJSC Marketing.

MJSC Investments Limited’s last accounts (made up to May 2016) contain virtually no information other than it owed £1,543 to short term creditors.

For the sake of balance, I will emphasise that MJS Capital’s main business entity – i.e. Colarb Capital plc (MJS Capital plc before October 2018) remains an actively trading company according to Companies House.

MJS Capital disclosed in its 2017 accounts that it has used a shell company, MJS Cap Ltd, to “support banking requirements” , in reference to its “issues relating to freezing of accounts or difficulties opening bank accounts”. Neither MJSC Marketing nor MJSC Investments were mentioned in these accounts as far as I can see.

Both MJSC Investments and MJSC Marketing have been added to our watchlist and we’ll cover it here if the administrators release any further details.

The mjs.capital website has now been restored, with a pop-up explaining the reason for the name change and a redirect to the new website, colarb.capital.

MJS Capital Plc is a UK company setup in March 2015 the decision to call our company MJS Capital was not our original choice instead we chose Fidelity One Capital however regulators at the time felt this was to similar to that of another well know finance firm and we would have to choose another. [Sic. Honestly. -Brev]

MJS / Colarb has never been a regulated investment firm. I assume by “regulators” they mean it was Companies House who objected to their choice of “Fidelity One”.

How MJS’ directors managed to work in finance without hearing of Fidelity International, one of the world’s biggest investment firms with over $400 billion under management, is beyond me. I also find it difficult to imagine that they thought that naming an investment firm “Fidelity One” wouldn’t be considered too close to Fidelity.

Since the company was incorporated a number of changes have come into place and our board has changed too with this in mind we have felt the old name does not reflect our company’s new direction.

Our new strategy now involves collaborating with various company’s [sic – Brev] and assisting their endeavours by utilising our existing arbitrage strategy and so our new company name will now be known as ColArb Capital.

Collaboration + Arbitrage = ColArb

The new colarb.capital website largely repeats some high-level details about MJS / Colarb Capital’s bonds. It also claims that the strategy currently used by Colarb Capital is “almost riskless”.

Our Strategy

There are a number of Arbitrage strategies, but pure Arbitrage is considered by many as a riskless form.

Investopedia defines Arbitrage as: “occur[ring] when a security is purchased in one market and simultaneously sold in another market at a higher price, thus considered to be risk-free profit for the trader”. […]

The Algorithm

Colarb Capital Plc has recently developed an exclusive contract with a team of coders, made up of 15 highly skilled and qualified members who have helped create a series of algorithms that have taken Colarb Capital Plc’s existing strategy and enhanced its ability to find price differences in the markets thousands of times over.

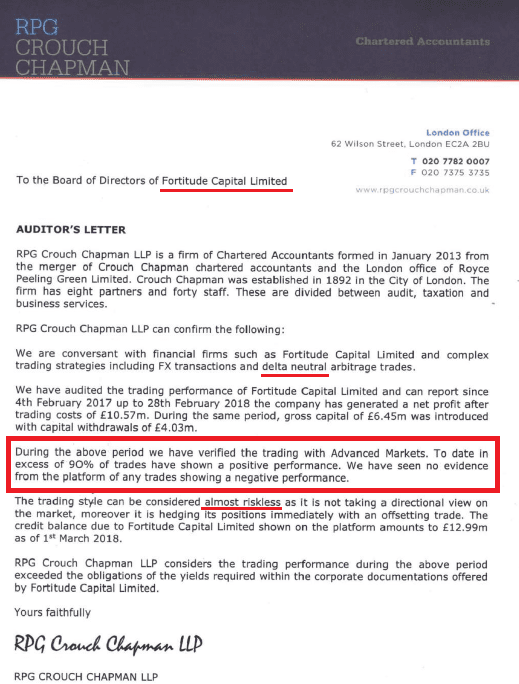

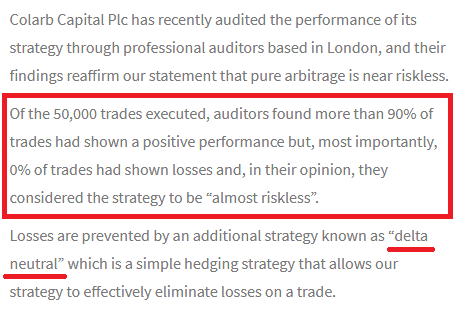

Colarb Capital Plc has recently audited the performance of its strategy through professional auditors based in London, and their findings reaffirm our statement that pure arbitrage is near riskless.

Of the 50,000 trades executed, auditors found more than 90% of trades had shown a positive performance but, most importantly, 0% of trades had shown losses and, in their opinion, they considered the strategy to be “almost riskless”.

MJS / Colarb’s website is technically correct that an arbitrage strategy can be “almost riskless”. (If I can buy on one exchange at $1.30 and sell on another at $1.40, this is almost riskless as long as I can move quickly enough to take advantage.) However, it does not address the fact that raising money through a loan note paying, say, 9.85% per year, and then using the money to invest in arbitrage, is most definitely not almost riskless, because I have to find enough arbitrage opportunities to generate sufficient money to pay my bondholders 9.85% per year.

Needless to say this is not easy, and if I fail to make sufficient returns from arbitrage to pay bondholders 9.85% per year and meet my own costs, there is a risk of default.

90% positive trades?

This mention of a firm of professional auditors finding that more than 90% of Colarb Capital’s trades were positive and 0% were negative sounds eerily familiar:

Letter from RPG Crouch Chapman LLP provided to us by an introducer promoting Fortitude’s bonds. Note that Fortitude is (according to its director Ajaz Shah) completely separate to and uninvolved with MJS / Colarb.Colarb Capital “about us” page.

Bearing in mind that the director of Fortitude Capital, former MJS-director-for-a-day Ajaz Shah, has recently confirmed that Fortitude is completely separate from and has no dealings with MJS / Colarb, it seems a remarkable coincidence that both Fortitude and MJS / Colarb have had exactly the same success rate confirmed by their accountants, using the same “delta neutral” strategy.

And, of course, the million-dollar-question is – if Colarb’s strategy is almost riskless and has been doing so well, why have some investors not been repaid on time?

According to a filing with Companies House, MJS Capital plc has changed its name to Colarb Capital plc.

Over the past year, a number of investors have complained via comments on this blog and other online forums about MJS Capital failing to repay their bonds when they fell due. A common theme is MJS Capital negotiating a payment plan for the repayment of matured investments, which MJS then also fails to meet.

In June 2018 MJS / Colarb disclosed in its September 2017 accounts that it had experienced banking issues, with banks either freezing its accounts or refusing to allow it to open new ones.

Non-executive director Lord Razzall CBE resigned from the company in March 2018, saying in his resignation letter that he hoped his removal from the board would resolve MJS Capital’s banking problems.

MJS also disclosed in their accounts that they used a company set up by a former director (Martin Westney), imaginatively named MJS Cap Limited, in another attempt at resolving its banking issues.

From the ongoing complaints by investors, it does not appear that either measure has achieved much.

In June and July 2018 there was a brief flurry of promotional activity by MJS on Medium and Twitter but the company has since appeared to fall silent.

MJS / Colarb Capital managing director and owner Shaun Prince previously incorporated a company under the name Colarb Holdings Limited in December 2017. Exactly what Colarb is supposed to mean is unclear, although “arb” may relate to MJS’ underlying investment in arbitrage, while “col” could refer to “collective” or “collateral”.

At time of writing MJS Capital’s previous website (mjs.capital) is down. A search on Google for an official Colarb-branded website produced no results.

MJS Capital plc offered unregulated bonds paying up to 14% per annum (via certain introducers).

A number of onlineposts over the past couple of months suggest the company is unable to is being slow to repay a few investors whose bonds have fallen due. MJS Capital has blamed “banking issues”.

We have asked Mr Hidderley whether he is still awaiting repayment of capital but have not received a reply at time of going to press.

Update 07.06.18: Jo has confirmed that he has since received his capital back with interest.

In March 2018 MJS Capital’s chairman and House of Lords member Lord Razzall resigned from the company, saying in his resignation notice that he hoped his resignation would resolve MJS Capital’s banking issues. With the company still unable to repay investors two months later, it doesn’t seem to have had the desired effect.

The company is currently two months overdue with filing annual accounts to Companies House, and almost certainly as a result, has been served with notice to strike off the company.

If MJS Capital continues to fail to submit accounts, and no valid objection is received by Companies House, the company will be dissolved in two months, and any remaining assets will be forfeited to the UK Government.

Investors can object to the striking off by contacting Companies House.

There was little sign of MJS Capital’s approaching troubles in September 2017, when members of the company appear to have enjoyed a highly agreeable dinner at the Tower of London, according to a video posted on Facebook by JetSmarter (a private jet hire company).

Update 7 June 2018: The strike-off has been suspended as according to Companies House, “cause has been shown why the above company should not be struck off the register”. As MJS Capital remains over two months overdue with its accounts, the most likely cause is an objection from a creditor.

If MJS Capital continues to fail to file accounts, the strike-off action may be resumed and the directors may be liable to prosecution.

A filing on Companies House reveals that Lord Timothy Razzall has stepped down as director of MJS Capital plc. MJS Capital plc offers unregulated bonds paying up to 9.85% per annum to fund investment in financial arbitrage.

Popularly known as “Lord Razzall of Dazzle”, Lord Razzall served as a director of MJS Capital from 19 May 2015 to 12 March 2018. He is described as non-executive Chairman in MJS Capital’s investment literature, and “responsible for scrutinising the performance of management in meeting agreed goals and objectives, in particular adherence to the investment policy and overseeing the correct and proper operation of the Security Fund”.

Lord Razzall remains a director of Barton Brown Limited, who wrote MJS Capital’s investment literature.

Under the heading and sub-heading “How the investment in the Bonds is protected”, MJS Capital’s literature states that the involvement of Barton Brown Limited and Lord Razzall in drafting the Information Memorandum means “Investment in the Bonds is directly protected” – in the sense that the involvement of Barton Brown Limited and Lord Razzall, along with their collective experience in corporate law, means investors can rely on the statements in the literature.

We reached out to Lord Razzall’s parliamentary office on Thursday for a comment on his reasons for leaving MJS Capital, but at time of writing have received no response.

Update 27 March 2018: By way of response, Lord Razzall has now provided us with a copy of his resignation letter to Shaun Prince, MJS Capital’s owner, which states:

The background to this is my concern about the effect I have as a politically exposed person on the company’s banking relationships.

This is a significant problem nowadays particularly for a company like MJS which is dependent on its banking relationships.

As you know I am happy to remain involved with the company as a consultant and advisor, but hope that my resignation as a Director will help with the banks.”

While Politically Exposed Persons are subject to a higher level of scrutiny when dealing with financial institutions, in itself it is difficult to see why having a PEP as director would cause problems for MJS Capital – particularly when you consider Lord Razzall was a non-executive chairman and did not exercise day-to-day control.

The FCA expects that a firm will not decline or close a business relationship with a person merely because that person meets the definition of a PEP (or of a family member or known close associate of a PEP). A firm may, after collecting appropriate information and completing its assessment, conclude the risks posed by a customer are higher than they can effectively mitigate; only in such cases will it be appropriate to decline or close that relationship. (FCA guidance FG17/6)

As Lord Razzall says, hopefully whatever problems MJS Capital is experiencing with its banking relationships will be resolved shortly.

Update 10-Oct-18: On 5 October 2018, MJS Capital plc renamed to Colarb Capital plc. This article was published on 19 January 2018 when Colarb / MJS was known by its old name.

Below is the original article published on 19 January 2018.

— end updates —

MJS Capital offers unregulated corporate loan notes paying 5.85% interest for a one year term, 6.85% for two years, 7.85% for three years, 8.85% for four years and 9.85% for five years. Interest is paid out quarterly, or can be rolled up (which slightly increases the annual return).

The bonds can be redeemed early, subject to a penalty and provided that MJS Capital “determines in its discretion that it has sufficient liquidity to satisfy the request in whole or in part.” The penalty is 5% plus the difference between any interest paid out and the interest the investor would have received had they chosen that term originally. For example, someone who invested in an 8.85% four year bond and redeemed it two years early would have to pay [8.85 – 5.85 + 7.85 – 6.85] = 4%, plus 5%.

Status

The investment is not openly promoted on MJS Capital’s website, but is currently being promoted by unregulated introducers. I easily obtained details of the offering without being asked to provide any proof that I qualified as a sophisticated or high-net worth investor.

Who are MJS Capital?

Shaun Prince, MJS Capital CEO and owner

MJS Capital’s website gives no details as to who is behind the company. The Information Memorandum and Companies House show that the directors of the company are Shaun Prince, Lord Timothy Razzall (Chairman) and Martin Westney. (Ajaz Shah is also listed as a Director in MJS’ Information Memorandum, but not on Companies House – he was appointed as a director on 15 May 2017 and removed as a director the same day.)

MJS is effectively 100% owned by Shaun Prince who holds 12,500 of the company’s 12,501 shares. The single other share is owned by a Stephen Prince, presumably related.

How secure is the investment?

These investments are unregulated corporate loans and if MJS Capital defaults you risk losing up to 100% of your money.

Investors’ money is used to invest in arbitrage trading in financial instruments.

Arbitrage is a perfectly valid way of making money, but the returns available are limited as any opportunity to take advantage of different prices on different markets will quickly be seized upon by other investors until the opportunity disappears.

If MJS Capital fails to make sufficient arbitrage profits to pay its bond holders up to 14% per annum, MJS Capital will default and investors risk losing up to 100% of their money.

The literature says that profits generated from the Company’s investments will be held in a designated Security Fund, which will be administered by a Security Trustee. However, the profits generated from the Company’s investments are being used to pay investors their interest and capital, so this offers no protection against the possibility that MJS Capital fails to make sufficient returns from arbitrage to maintain interest and capital payments to investors.

The literature says that Bonds are backed by a charge over the Security Fund, the Company’s cash balances, its trading contracts which utilise the proceeds of issue of the Bonds, and book debts arising from deploying the proceeds of issue of the Bonds.

The Security Fund we have already covered. If MJS Capital defaults, it will be because the Security Fund has already run out of money, i.e. profits generated from the company’s investments were insufficient to meet its obligations.

The company’s cash balance was £194 acccording to the latest accounts filed with Companies House (March 2016). (194 pounds, not thousands or millions).

Regarding the final two, given that MJS Capital’s business is to buy investments on one exchange and almost immediately sell them on another to generate profits from arbitrage, it is not clear what there will be to sell in the event that MJS Capital has insufficient resources to pay investors.

The company has an insurance policy of £10 million against the event that MJS Capital executes a trade not in accordance with its client instructions, and £20 million against operational risks such as fraud and computer viruses. Neither of these insurance contracts have anything to do with the possibility that MJS Capital fails to generate sufficient returns from arbitrage to meet its promises to investors.

Should I invest with MJS Capital?

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 14% per annum yields should be considered very high risk (i.e. higher risk than a diversified portfolio of stockmarket funds).

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for a “secure investment”, you should not invest in unregulated products with a risk of 100% capital loss.

Footnote

Shaun Prince, the owner of MJS Capital, took part in this thread on Moneysavingexpert.com as a verified representative of his company.

During this thread Prince made the frankly astonishing statement “The saying “if it looks too good to be true it almost certainly is” is no doubt a saying created within the regulated market to encourage investors away from investments offering higher than average yields.”

In linguistic terms, Prince is objectively wrong. The phrase “too good to be true” is attested as early as 1580, long before there was such thing as a regulated market.

Less pedantically, investors will have to make up their own mind whether the phrase “too good to be true” is a conspiracy to scare them away from high-risk loan notes.

In any case, this investment is clearly not “too good to be true”. It is a high risk investment with a risk of 100% capital loss, and the high coupon paid by the bonds reflects that.

In that thread, Prince claimed that MJS Capital would be listing on the London Stock Exchange in April 2017. However, as at January 2018 a search for MJS Capital on the LSE returns no results.

Popularly known as

Popularly known as