Amicus Invest offers three unregulated offshore investment products:

- Amicus Bonus Cash Account: Pays 4% per year interest (3% on balances calculated daily and a further 1% “bonus” on balances calculated quarterly). Funds can be added and withdrawn at any time.

- Amicus Regular Savings Plan: Pays interest on monthly investments as follows: 6% for a 1 year term, 7% for a 2 year term, 8% for 3 years, 9% for 5 years and 10% for 10 years. Early withdrawals are permitted but forfeit all interest accrued.

- Amicus Single Investment Plan: Fixed term investments paying interest as follows:

- 3 months – 4% per annum

- 6 months – 5%pa

- 1 year – 6.25%pa

- 2 years and 3 years: “Guaranteed Total Return of 15.00% (equal to 7.25% pa.) and 26.00% (equal to 8.09% pa.)”

- 5 years and 10 years: “Guaranteed Total Return of 45.00% (equal to 8.75% pa.) and 100.00% (equal to 9.50% pa.)” – these numbers don’t add up, as a 45% return over 5 years is 7.7% compounded, and a 100% return over 10 years is 7.1% compounded.

The discrepancy between the rates available on 5 and 10 years is not explained, nor is it explained why investors would want to receive a lower rate of return for locking their money away for longer.

Who are Amicus Invest?

No information is provided on the Amicus website as to who owns or controls the business.

Despite displaying an Austrian address on its website, Amicus Investment Ltd is registered in the Marshall Islands (a small country in the Pacific Ocean with a population of just over 50,000).

Pictures on the website which supposedly show Amicus Investment “advisors” are in reality stock photos.

The company was incorporated in 2011, redomiciled from the Bahamas to the Marshall Islands in 2013, and the amicusinvest.com website was registered in May 2013.

How safe is the investment?

These investments are unregulated corporate loans and if Amicus Investment defaults you risk losing up to 100% of your money.

Amicus claims that investors’ funds are invested into “a range of interest bearing instruments like consumer loan portfolios and corporate bond funds. The rest of our assets are invested into equities globally.”

Should Amicus fail to make sufficient returns from its consumer loans and other assets (e.g. due to a fall in the markets or defaults by its borrowers), there is a risk it may be unable to return investors’ money.

The use of terms like “Guaranteed” and “Cash Account” to describe loans with a risk of 100% capital loss is highly misleading from a regulatory perspective, and would not be permitted if Amicus was regulated in the EU or most other developed markets.

Should I invest with Amicus Investment?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 8% per annum yields should be considered high risk. As an individual security with a risk of total and permanent loss, Amicus’ investments are higher risk than a mainstream diversified stockmarket fund.

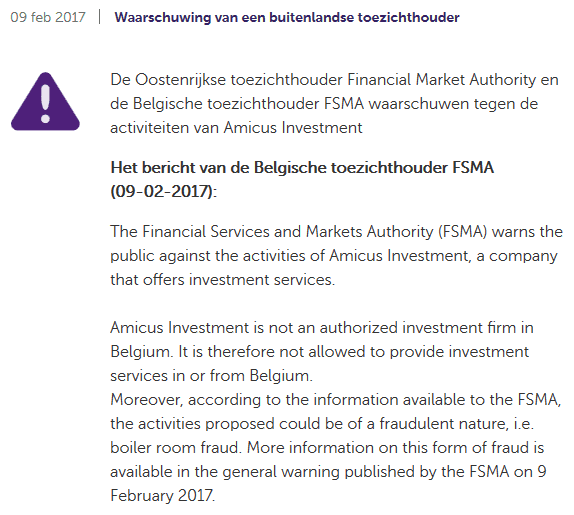

Amicus has already been subject to warnings from regulatory authorities in Austria and Belgium.

Under Amicus’ “Frequently Asked Question” section, one FAQ is as follows: “I read that the financial regulatory authority of a country has issued a warning about Amicus Investment. What does it mean?” Amicus rather brazenly replies: “Amicus Investment Ltd. is registered in the Marshall Islands. We offer our financial services to clients from all over the world, following the legislation of the Marshall Islands. Therefore, we are not bound by other countries’ financial authorities and such warnings have no effects on our business.”

The fact that Amicus is, according to its own website, “frequently asked questions” about these regulatory warnings should be enough to give investors pause.