Buy 2 Let Cars Limited offers the opportunity to invest in lease cars over a term of three years as follows:

- Level 1: invest £7,000-£10,000 and receive a return of 7% per year

- Level 2: invest £14,000 to fund “one unit” and receive a return of 9% per year

- Level 3: invest to fund “two to six new units” (presumably £28,000 – £84,000) and receive a return of 10% per year

- Level 4: invest to fund “7 or more units” (£98,000 or more) and receive a return of 11% per year

Investors’ funds are used to purchase a lease car (or multiple cars) which is then leased out to a borrower. The borrower’s lease payments are used to generate the promised return.

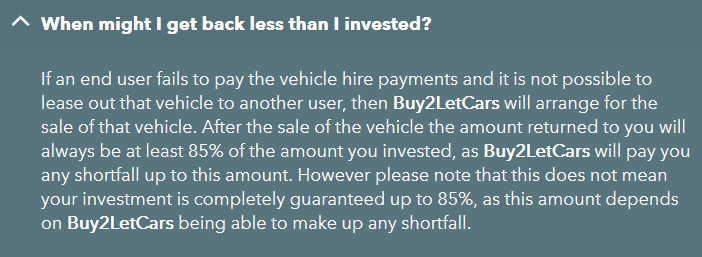

If the borrower defaults on their payments, and Buy 2 Let Cars is unable to find another borrower, Buy 2 Let Cars will attempt to sell the car to return investor’s capital. If the amount realised is less than the investor invested, Buy 2 Let Cars promises to make up any shortfall up to a maximum of 85% of the amount invested.

Buy 2 Let Cars consists of three companies: Buy 2 Let Cars Ltd, Rent 2 Own Cars Ltd (trading as Wheels 4 Sure) and the parent company Raedex Consortium Limited. For the remainder of this article, Buy 2 Let Cars (which is the name the group uses most often) refers to the whole group or investment, unless otherwise specified.

Raedex Consortium Limited is regulated by the FCA for its car leasing activities, but the investment opportunity is unregulated.

Who is Buy 2 Let Cars?

Buy 2 Let Cars was incorporated in 2012.

The parent company, Raedex Consortium Limited, is 90% owned by the founder and CEO Reginald Larry-Cole. The remaining 10% is owned by Operations Director Scott Martin.

How safe is the investment?

This is an unregulated investment into lease cars (and, in terms of the promise to return at least 85% of your capital, Buy 2 Let Cars itself) and you risk losing up to 100% of your money if Buy 2 Let Cars:

- fails to generate sufficient returns from its car leasing agreements to sustain returns of 7-11% per annum,

- and runs out of money to compensate investors up to the promised 85%.

As investors are relying on Buy 2 Let Cars to make up any shortfall if the lease payments are insufficient to pay returns of 7-11% per annum, this is not just an investment into a car, but into Buy 2 Let Cars as a company.

Buy 2 Let Cars Limited’ last accounts (up to December 2016) show net assets of £1.3m, comprising roughly £19.5m in debtors, £1.5m of cash in the bank, and £19.7m of creditors (predominantly investors’ money). Note that these accounts are unaudited (due to Buy 2 Let Cars Limited’ small size) and are from a year and a half ago.

Buy 2 Let Cars Limited did not file a profit and loss account (again due to its small size), but note 1.2 in the accounts under “Going Concern” shows that the company was loss-making at the time.

As a result of the delay and in anticipation of lower volumes and margins than planned in respect of used car activities, the earlier projections of positive Earnings Before Interest Tax Depreciation and Amortisation (EBITDA) throughout 2017 and profitability achieved from activities in the last quarter of the year will not be realised.

The Directors have therefore conducted a further review of the underlying private customer leasing business model which culminated in a new marketing strategy and rebranding of the businesses at the end of the first quarter of 2017…

…The directors are confident that the business will yield positive EBITDA in the final quarter of 2017 and become profitable at a pre-tax level from the beginning of 2019.

Investors should ensure they do full due diligence on Buy 2 Let Cars, including obtaining details from the company of its up to date funding position, before investing.

Potential collective investment

Under the Financial Services and Markets Act, it is illegal to run a collective investment scheme without authorisation from the Financial Conduct Authority. Raedex Consortium Limited is an FCA authorised company, but is not authorised to run a collective investment scheme (its authorisations relate to the vehicle leasing side).

Buy 2 Let Cars represents to investors that they are investing in individual cars. Investment in individual assets (such as shares, flats, hotel rooms, store pods, etc etc) is in itself not a regulated activity, whereas a collective investment is. (We don’t make the rules.)

So if Buy 2 Let Cars investors were purely investing in individual cars, with each investor receiving only the returns attributable to their individual car, Buy 2 Let Cars’ investment scheme would not be considered collective and they would not require authorisation to run the investment.

However, Buy 2 Let Cars promises that all investors will receive at least 85% of their capital back, even if the car they invest in is completely written off.

Under UK legislation, there are three prongs to the definition of a collective investment scheme: a) the investor must not exercise day-to-day control of the investment, and either b) “the contributions of the participants and the profits or income out of which payments are to be made to them are pooled” or c) the property is managed as a whole by or on behalf of the operator of the scheme.

A) is quite clearly the case with Buy 2 Let Cars; Buy 2 Let Cars openly promotes the fact that its investment is “hands-free”.

There is a risk that Buy 2 Let Cars’ promise to return at least 85% of investors’ capital to investors may be deemed by the FCA to represent B), pooling of contributions and profits.

This is however not a certainty, as Buy 2 Let Cars could argue that the funds it uses to fulfill its 85% promise come from elsewhere.

Whether or not Buy 2 Let Cars is deemed by the FCA to be running a collective investment scheme without authorisation, investing with a company that is not authorised to operate collective investments represents a regulatory risk. Investors will need to ensure they are happy with this regulatory risk before they proceed.

Should I invest with Buy 2 Let Cars?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual investment security, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 11% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Buy 2 Let Cars is higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

- How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

- Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

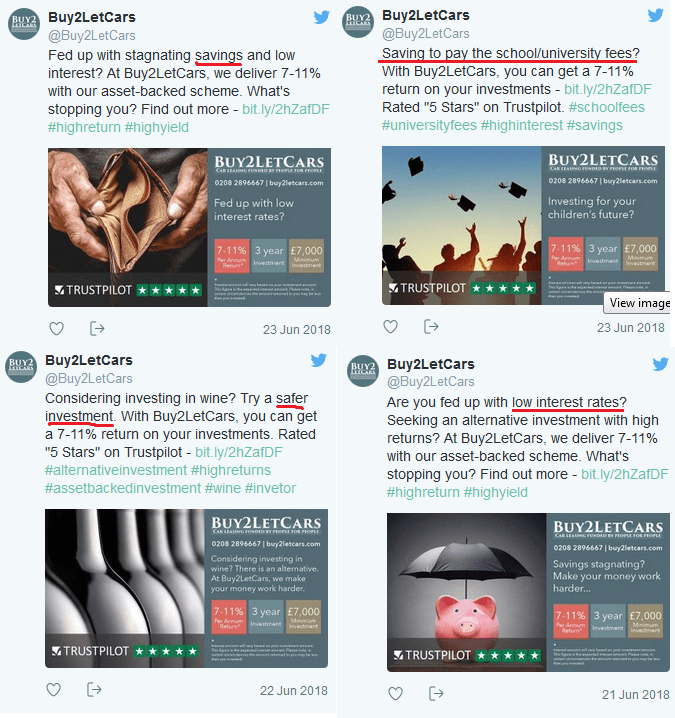

Buy 2 Let Cars runs adverts on Sky and on Twitter that urge potential investors to consider Buy 2 Let Cars as an alternative to a savings account, and refer to their product as a “safer investment”.

Novice investors who have previously only invested in deposit accounts, are unhappy with the returns, and want to start taking some risk, should first consider a regulated diversified portfolio of conventional stockmarket investments. While these will go up and down in the short term, a diversified portfolio of regulated investments has minimal risk of loss in the long term provided the investor doesn’t panic and cash it in.

This investment by contrast is unregulated and has a risk of permanent and total loss due to the risk that Buy 2 Let Cars does not generate sufficient returns from your car, and runs out of money to meet its promise to pay investors up to 85% of their investment.

If you are looking for a “safer investment”, you should not invest in unregulated investments with a risk of total and permanent loss.

They refer to their product as a ‘safer investment’ than wine. This is true given that wine is valued subjectively, not objectively and (unlike personal transport) cannot in any way be deemed a necessary asset. Also wine ‘investment’ is dependent on a speculative belief the wine will go up in value, whereas car leasing is structured around the inevitability that the car itself will depreciate at a predictable rate, which is more than offset by the car driver’s structured lease hire payments.

They do not and have not referred to their product as being safer than a savings account, so it is disingenuous aka wrong of you to claim otherwise.

And bathtub gin is a safer drink than a four-door hatchback. Category error ahoy. On this I suspect we agree.

It is disingenuous of you to claim I said any such thing.

In fact, cars and wine are valued in pretty much the same way. At the mass-market end they are commodified and easy to value by reference to a large market for common items (Beyerskloof Pinotage and Ford Fiestas, to betray my own preferences).

Once you get to rare vintages, cars do economically behave like so-called “fine wines”. I’d challenge commentator “Craig” to demonstrate the objective valuation criteria of a DB5, E-Type or F40.

I under the reasons to be cautious and one should most certainly be with any investment. I am a cautious and hesitant person and don’t invest into 99% of investment opportunities I do due diligence on.

One has to take some (very meticulously researched and calculated) risks in investment, otherwise leaving money in an FSCS-protected bank savings account is likely to give a return far lower than inflation so is losing its value by the day.

I have been investing with Buy2LetCars for quite a while now. This is a very slick and professional operation.

Always receive my monthly payments on time.

All round excellent customer service. Scott, Reginald and the entire team have been truly warm, amicable and helpful to me time after time.

I was naturally cautious to start with, but did a lot of research and discovered this was a successful and efficiently run outfit.

I am making a very healthy return month-in month-out and am glad I took the plunge to invest with Buy2LetCars.

Adam

You’ll forgive the inevitable scepticism that you face by referring to the subjects by their first names. But it’s not about getting your monthly returns; tell me this works when you get your principal back.

By investing in cars, you’re putting your money into wasting assets. What do your meticulous researches and calculations tell you about their fleet management strategy?

Adam (the 10th September one!), as part of your detailed due diligence have you reviewed the accounts for 31/12/18, as recently published at companies house? If so, you will quickly realise that you need to look beyond Buy2Let cars.

Incidentally, as an ‘investor’, or lender more like (I presume you haven’t been buying shares in the company) are you happy that a company that has on the face of it now taken in significant funds from punters such as yourself still does not see the need to produce audited accounts?

Anyway, the financial statements for Buy2Let look pretty good as a stand alone entity- good growth in business, good retained earnings, £1.2m cash in the bank…all looks fine. However, drill deeper and you will see that its signifiant asset is not actually cars being leased out, but an inter company claim of around £30m. The accounts don’t say who has borrowed this money, but a quick bit of research suggests the bulk of this debt might be owed by another group company, Rent2Own Cars. This company has accumulated losses of around £8m and associated negative net worth of that magnitude,

But the puzzle doesn’t stop there, for the principal asset of Rent2Own is yet another intercompany loan, this time of circa £20m; this amount might possibly (again,it’s not clear from the notes to the accounts) be owed by yet another group company, Raedex Consortium. Which itself has significant accumulated losses and a negative net worth (even including the somewhat dubious revaluation reserve) of £9.5m. And underlying external assets of only around £8m.

It’s interesting that you allude negatively to keeping cash in the bank, at very low risk and below inflation returns. I accept I may have got this wrong, and might have misunderstood their business model, but on the face of it this is a group with very significant losses and I fear that if/when new funds dry up, you could face a material loss of capital. Caveat emptor: my money is staying in the bank!

@Ian – great analysis. Normally Brev brings out the hidden details, but this time she didn’t! What’s that about?

I’ve seen the ads on SKy (although not seen them for a while now) and never understood why they were permitted to promote an NMPI to unsophisticated/low net worth investors.

When is the FCA actually going to do its job?

As for happy investors, thinking they’ve struck gold …. I bet they all think that – even LC&F investors – until it goes wrong, then they all get seriously miffed and shout for compensation …. this cycle will never end. It’s the human condition. My money is safely in NS&I bonds where it is staying and I now sleep soundly at night.

Does anyone know how Paygo Cars Ltd fits into the Raedex corporate structure, if it does at all? According to its companies house filing, Reginald Larry-Cole is stated as being Paygo’s sole shareholder.

Certainly, Paygo doesn’t feature as an investment holding in Raedex’s accounts, at least as at 31/12/18, so there is nothing to suggest that the ownership position had changed by that date. On the other hand, at 31/3/19 Paygo owed £1m to ‘group undertakings’, and it is not at all clear as to whom those undertakings might be or indeed, given Larry-Cole appears to be its sole shareholder, to what corporate grouping Paygo forms part (Paygo doesn’t appear to have any subsidiaries of its own).

If one were to look at the intercompany activity between Raedex, Buy2Let and Rent2Own as set out in their respective 31/12/18 accounts,there appears to be an unexplained difference of around £1.7m in the numbers, so this Paygo intercompany figure might -or indeed might not- be connected with the Raedex group, and would go some significant way towards explaining some of this difference, although given Paygo doesn’t appear to be part of the Raedex corporate grouping, just in common ownership, I should have thought it would be better described as a connected party transaction rather than ‘group’ debt.

@ Ian Bancroft: All very sensible observations and questions. I think the learning point for all readers is that you should not regard unaudited accounts as a reliable source of information, and definitely not rely on them as part of your due diligence for prospective investments.

Buy2Let cars are now running investment seminars at hotels to attract new punters.

I was quite tempted to have a punt on this scheme before reading these comments. Thank you for the info.

Have been looking at this investment for over a year. Went on the most recent webinar hosted by Reginal Larry-cole and had decided to invest. These post have made me have a re-think and I now will not be. I asked my investment contact, in a telephone conversation today if any new investors money was ever used to repay a previous investors final return of capital. His response, “highly likely”. Is this close to the definition of a ponzi scheme? I think the Paygo company seems to have the potential to retain a percentage of commission on the sale of ex-lease cars and seems to be for the sole purpose of lining Mr Coles pockets.

New article: Breaking: Buy2letcars closed to new investment by FCA, assets frozen