Byrne told his clients that the funds were low-risk when they were anything but, and Jersey prosecutors successfully convinced the judge that this went beyond misselling into outright fraud. Byrne also failed to tell investors that his firm, Lumiere Wealth, was owned by Providence; a blatant conflict of interest.

Des Jeffrey, who “reluctantly” became a Lumiere director after Providence collapsed, told the court that most of the investors whom Lumiere convinced to invest in Providence were far from sophisticated.

Once he began meeting the clients who had been affected, he realised most were not seasoned investors.

Among those who lost substantial sums, the court was told, were a 79-year-old partially sighted woman and a father of four who was a first-time investor.

‘Once I had actually met them I could see quite a few were not what I would call sophisticated investors,’ Mr Jeffrey said. ‘From a professional perspective, it was a high percentage of a person’s wealth that would have gone to Providence.’

Correction 26.10.18: The initial version of this review speculated that one of Fortitude Capital’s investors was MJS Capital plc. This was based on a note in MJS Capital plc’s last accounts stating that it had a forex investment with a UK limited company run by a former director of MJS. Ajaz Shah, the director of Fortitude, has emailed us to say that he is not the former director of MJS running a UK forex company in question, and that Fortitude has never managed funds for MJS.

I can clearly state that my company Fortitude Capital Ltd has never managed funds for MJS Capital Plc. From my knowledge through the one day that I was a Director for MJS (May 2017), I was aware that MJS had access to multiple traders. I was not involved with the MJS latest account filings and had no involvement with the way these were compiled.

I am happy to set the record straight.

The previous version of the review also noted that Ajaz Shah was a director of MJS Capital for a single day, and that he was listed as a director in MJS Capital’s literature. Shah has told us that MJS Capital’s literature was “completely incorrect” and emphasised that he was only a director for a single day.

For an updated review of Fortitude Capital’s bonds, read on.

Fortitude Capital is offering unregulated one year bonds paying interest of 8% per year. A Fortitude representative has told me that they also offer unregulated five year bonds paying 10% per year, although I’ve only seen the literature for the one year bonds.

Selected introducers are offering enhanced terms whereby the interest rate is increased to 12% per annum for investments above £50,000, 11% for investments between £25,000 and £50,000, and 10% for investments between £10,000 and £25,000.

Fortitude Capital intends to use its investors’ money for “algorithmic trading” in the foreign exchange (forex) market.

Who is Fortitude Capital?

Ajaz Shah, Managing Director and owner of Fortitude Capital

The Managing Director of Fortitude is Ajaz Hussein Shah. As mentioned in the above correction, Shah was previously a director for a single day of MJS Capital plc, an issuer of similar unregulated bonds. Companies House shows that Shah was appointed as a director of MJS Capital plc on 15 May 2017 but removed the same day. Shah has emphasised that he was a director of MJS for a single day only, and described MJS literature which listed him as a director “completely incorrect”.

Fortitude’s other director is non-executive director Heinz-Jorg Jansen.

According to its latest confirmation statements, Fortitude Capital is 100% owned by Ajaz Shah.

Fortitude Capital was incorporated in March 2013, but its accounts show that it was largely dormant until the 2016/17 accounting period. The latest accounts show net assets of £742,000 as at March 2017, compared to a nominal £100 for March 2016. The accounts were unaudited due to the company’s small size.

Update 26.10.18: Shah has drawn our attention to Fortitude’s latest accounts, dated 31 March 2018, which now show net assets of £7 million (predominantly £12 million in investments and £5 million in creditors). Investors should note that these accounts were not audited by an accountant due to Fortitude’s small size. For the same reason they did not include a profit and loss account. If investors plan to rely on these accounts when deciding whether to invest, they should obtain professionally audited accounts from Fortitude as part of their due diligence.

Dependence on a single investor

Shah has stated in an email to us that he holds over 75% of Fortitude’s assets under management.

Therefore, my own investment on to my platform is more than 3 times the amount that has been raised through bonds.

Any investment firm where a single investor holds 75%+ of the assets under management has a risk of being over-reliant on that investor. Even if that investor is a director, they have the same right as any other investor to withdraw their investment to spend or reinvest elsewhere.

As part of their due diligence investors should ask Fortitude what contingency plans they have if Shah decided to withdraw his investment.

How safe is the investment?

These investments are unregulated corporate loans and if Fortitude defaults you risk losing up to 100% of your money.

The purpose of the bonds is to allow Fortitude to speculate on forex using algorithmic trading strategies.

If Foresight fails to make sufficient returns from its forex trading, or for any other reason Foresight runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

According to one of Fortitude’s introducers, “the algorithm has been designed around the principle of Capital Preservation, so that the majority of trading risk is offset by sophisticated use of arbitrage and hedging techniques”. Nonetheless, no matter what efforts Fortitude makes to reduce risk, there remains a risk that it does not make sufficient returns to pay up to 12% per year to bondholders, on top of its other costs, and return their capital when it falls due.

Fortitude’s information memorandum is clear in this regard, with pages 2-3 including the risk warning:

Investment in the Bonds carries substantial risk. There can be no assurance that the Company’s investment objective will be achieved and investment results of the Company may vary substantially over time. This may affect the Company’s ability to pay interest on the Bonds and to redeem them at maturity, and investors therefore may suffer a partial or complete loss of their investment in the Bonds.

and making clear that the company will only accept investments from professional, high net worth or self-certified sophisticated investors, or high net worth companies.

Shah has stated in his email to us that

Our platform is consistently positive, with no losses at all. Our equity curve has always and still in a positive direction. [sic]

While I have no reason to doubt Fortitude’s successful returns to date, there is a wealth of academic literature showing that very few investment managers will consistently beat the market over time, and the inherent risk of Fortitude Capital failing to make sufficient returns to pay out 8-12% over a year remains.

Should I invest in Fortitude Capital bonds?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of up to 12% in a year should be considered very high risk. As an individual security with a risk of total and permanent loss, Fortitude’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If your priority is “capital preservation”, you should not invest in unregulated investments with a risk of 100% capital loss.

The investment may be suitable for high net worth and sophisticated investors who will already be well aware of all of the above risks, are looking to invest a small part of their assets in corporate lending, and feel that the return on offer (up to 12% over one year) is sufficient for the risks involved in lending to a small unlisted start-up company.

Readers will recall that one of Privilege’s main underlying investments was the loan book of a company called Rosebud which extended payday loans to the Sioux Indian Tribe of South Dakota. Since the administrators’ initial report, the administrators have succeeded in recovering $87,000 from a Rosebud escrow account (£63,000).

Some further small sums recovered from various parties bring the total funds recovered from Privilege to £91,000. The administrators are due 30% of all recoveries, and this plus legal and other costs take the net amount recovered to £51,000. With Privilege’s Wealth’s debts identified as £4.2 million, clearly this will not go far among the creditors.

The administrators are still trying to gain control of the Rosebud loan book itself. However, while the administrators believe that Privilege has obtained the legal right to the loan book, the data as to who Rosebud loaned money to is in the hands of another creditor, Oliphant Group, whom the administrators believe may be collecting money from the Sioux Indians.

Readers will also recall that another company, Helix, is seeking to enforce its own claims against Privilege Wealth’s assets. At the time of the initial proposals to creditors, Helix and the Privilege Wealth administrators had agreed in principle to co-operate, but the most recent update confirms that “a satisfactory agreement has not been reached to date”. A definitive and satisfactory response has also not yet been provided over the current position regarding Helix enforcing their alleged security.

According to the administrators, it appears that Helix is controlled and/or directed by one of Privilege’s former directors, Peter Stokes, who resigned as a Privilege director in May 2017.

In addition to Rosebud, Privilege made further investments into distressed credit card and bank debt through its US subsidiary, Privilege Direct Corp. Helix is also claiming security over this asset, and has already commenced legal proceedings in Florida.

The prospect of any significant recoveries for Privilege Investors would appear to rest on whether

a) Privilege can gain control of the Rosebud and Privilege Direct loan books and

b) whether the loan books, which consist of payday loan and “distressed” (i.e. sub-prime) debt, are worth much of anything in the first place.

An insurance claim has also been made by Peter Stokes on behalf of both Helix and Privilege in respect of an insurance policy against “capital shortfall” from an insurer, Independent Risk Solutions Limited, in the small Atlantic island of Bermuda. The administrators appear uncertain as to whether this insurance policy is likely to result in any funds for investors, noting only that further investigation is required.

The administrators have not repeated their finding in their original report that Privilege was “possibly operated as a Ponzi scheme” (on the basis that Privilege only invested $9m out of $40m investors’ money into actual assets). Which is to be expected. The administrators’ job is to maximise recoveries for creditors, not to solve the philosophical angels/pin question of how little an investment scheme can invest of its investors’ money before it crosses the line from poorly-run but perfectly legal failed investment scheme to illegal fraud.

The administrators do reveal that they have submitted a report on the conduct of Privilege’s directors to the Department for Business, Energy & Industrial Strategy, but this report is confidential and the contents are undisclosed.

One notable potential source of recoveries that the administrators have identified is the recovery of costs from Privilege Wealth’s successful libel action against David Marchant, editor of Offshore Alert, who publicly denounced Privilege as a fraud shortly before it collapsed.

Readers will recall that Marchant lost the case by default, by not turning up in the UK to defend himself, instead relying on the fact that a UK libel judgment couldn’t be enforced against him in the US. The courts awarded legal costs of £80,000 against David Marchant, which he remains due to pay to Privilege, at least in the eyes of the administrators and the UK libel courts.

The administrators are keeping the matter “under review” and say they will revisit the question of whether they can enforce this debt once recognition proceedings are finalised.

So the Privilege administrators, who have already described the company they are managing as a “possible Ponzi scheme”, are apparently considering whether to chase David Marchant for a legal debt he owes because he accused Privilege of being a Ponzi scheme.

Presumably if the case had to be re-run in front of a US court, Privilege’s administrators would have to argue that Marchant libelled Privilege by describing it as a fraud whereas it was really only a possible fraud.

Privilege’s administrators have a statutory duty to claim any money they can legally get their hands on for the benefit of Privilege’s stricken investors. So if it was feasible to collect 80 grand from Marchant, the administrators are duty-bound to give it a go. But I rather suspect that this is another receivable that will not come to anything.

The administrators will be due to file their next report in six months’ time.

Davenport Laroche offers an unregulated investment in shipping containers, which promises returns as follows:

“Conservative Lease” – fixed returns of 12% each year

“Higher Income Lease” – variable returns, described as “up to 24.13% ROI”. Later in Daveport Laroche’s promotions, this 24.13% figure is also described as the historic return for 2016.

In both cases, Davenport Laroche promises to buy the containers back after 5 years at cost price.

Who are Davenport Laroche?

Jacques Piccard, Managing Director of Davenport Laroche

Davenport Laroche is a company registered in Hong Kong. According to a news item on Davenport Laroche’s website, the company is headed by Jacques Piccard.

Piccard’s corporate biography is extremely sketchy. According to the company, he worked for the collapsed bank Bear Stearns until 1994, left to take up a private research position alongside “former apprentice master Pierre Durand” (what?) and moved back to Switzerland in 2003 to continue Durand’s work (presumably now as a master apprentice). After founding an unnamed school of economic instruction in Lausanne, Piccard was recruited to consult for a container leasing company, and from this went on to found Davenport Laroche.

By nature, neither Piccard’s position at a long-collapsed bank or his subsequent work in private research and teaching is verifiable. It is quite possible that Jacques Piccard does not exist, with the actual controllers of Davenport Laroche being unknown individuals from Hong Kong or elsewhere in Asia.

Marketing literature from the company (e.g. this quite obviously self-published article on moneyinc.com) claims the company was founded “in the wake of” the 2008 financial crisis. However, whois.com shows that davenportlaroche.com was only registered in 2013 and archive.org only began retrieving content from that domain in 2015.

The Hong Kong company was founded in 2011, but was only known as Davenport Laroche after a name change in January 2014. It is very possible that the people behind the company acquired an already-existing Hong Kong company and renamed it.

Either way, the founding of the company was quite clearly considerably more recent than 2008.

How safe is the investment?

This is an unregulated investment into shipping containers (and, in terms of the “Conservative Lease”, Davenport Laroche itself) and you risk losing up to 100% of your money if Davenport Laroche fails to generate sufficient returns from its shipping contains to pay the promised returns, and/or buy your container back.

With the Conservative Lease, investors are effectively investing into Davenport Laroche itself. The returns from their shipping container are only indirectly relevant. It does not matter if the shipping container makes less than 12%, as Davenport Laroche should be obliged to pay the difference. Likewise if the shipping container makes more than 12%, the extra goes to Davenport Laroche.

This means that your 12% per annum, and the ability to get your money back by selling the container after five years, is dependent on the financial strength of Davenport Laroche. Investors should focus their due diligence on Davenport Laroche’s finances, not the shippingcontainer.

Investors in the Higher Income Lease, on the other hand, are entirely reliant on Davenport Laroche continuing to find renters for its containers.

Given that Davenport Laroche claim to have historically paid out 24% per annum, investors are very dependent on the ability of Davenport Laroche to find clients willing to pay over the odds for shipping containers, instead of renting from one of its rivals that does not offer 24% per annum returns to investors.

Marketing literature from Davenport Laroche claims “They [the containers] will not lose their value either, as they hold material and functional value.”

This is directly contradicted only a couple of paragraphs above, where it states “All containers are built to full ISO-standards, meaning they have an expected lifespan of 20 years.”

In other words, the shipping containers would be expected to lose 5% of your initial investment each year on a straight-line depreciation basis, and become worthless after twenty years.

This means investors are even more reliant on the financial strength of Davenport Laroche. If the value of a new shipping container remains constant, no-one else is going to buy a 5-year-old shipping container from you at cost price, given that on a straight-line depreciation basis, it will have lost 25% of its value.

In the worst case scenario, you risk losing up to 100% of your money if Davenport Laroche fails to make enough money from its shipping containers to pay the promised returns, and a buyer cannot be found for your shipping container, or the shipping container depreciates to the point of worthlessness.

Illegal financial promotions

Davenport Laroche is being promoted to UK investors via ads on Google. One testimonial on Davenport Laroche’s own website is from a “Michael Frost, United Kingdom”.

It is illegal for companies to issue financial promotions in the UK unless they are regulated by the Financial Conduct Authority or are “passporting-in” from another EEA regulator. A search for Davenport Laroche on the FCA register produced no results, and Davenport Laroche does not claim authorisation from any regulatory body in its literature.

The promotion of this investment to UK investors is illegal without FCA authorisation.

Should I invest with Davenport Laroche?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual unregulated investment, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 24% per annum yields is extremely high risk. As an individual security with a risk of total and permanent loss, Davenport Laroche is much higher risk than a mainstream diversified stockmarket fund.

Davenport Laroche’s repeated description of this investment as “low risk” is highly misleading.

Multipleinvestors have alleged that Davenport Laroche is in reality the same company as Pacific Tycoon, a very similar Hong Kong based investment in shipping containers. Pacific Tycoon has a long string of complaints from investors who have already failed to receive promised returns, going back to 2016. Several investors have reported that on calling Davenport Laroche, the phone was answered as Pacific Tycoon.

Given these allegations, the inconsistencies in Davenport Laroche’s literature and the misleading statements about the risk profile of the investment, investors should not proceed unless they are happy to risk 100% loss.

Previously on this blog I have preferred to review individual investments. But there is currently a plethora of firms offering investment in a myriad of hotel rooms, and as it’s impractical to review each hotel room individually, I decided to write a general guide.

This article is about investments which work as follows:

A larger property is divided up into individual units, and the units are sold to investors. For example, a hotel is divided into hotel rooms, and the hotel rooms sold to investors. Or a car park may be divided into parking spaces and the spaces sold to investors, or a self-storage facility may sell off its storage pods. The promoter of the scheme still owns the hotel, the car park or the storage facility.

Unlike a buy-to-let flat or similar property investment, the investor does not manage the investment and is not responsible for generating the return. This responsibility remains with, or is “leased back” to, the promoter of the scheme to which the investors gave their money.

Unlike a buy-to-let flat, the investor does not receive a variable rent, but is promised a fixed return by the scheme promoter. Promised returns of 8% – 12% are common, although it can be more or less.

(In some investments it may be optional to “lease back” the investment for a fixed return. But in practice, the vast majority of those who buy the investment will. It is after all unlikely that they will do better by managing the investment themselves than the 8 – 12% the promoter is offering.)

For brevity I have referred to “hotel rooms” for the rest of the article, but if you are considering investing in, say, a parking space offering a fixed return of 8% per annum, you can simply insert “parking space” for “hotel room”. Same goes for any investment which matches the bullet-points description above.

These investments are investments in a company, not in a property

If you buy a flat from a seller and the seller walks away with their money and no further involvement, you’re investing in a flat.

If you buy a room in the Great Northern Hotel from Acme Investments Ltd on the promise of a “fixed return” or “guaranteed return” of 8%, you are no longer investing in a property. You are investing in Acme Investments Ltd, as your return depends on their ability to pay your 8%.

This is a lovely photo of a hotel, but it’s totally irrelevant to your investment.

How much money Acme makes from the guests in the hotel room is only of tangential interest to you. It doesn’t matter if the hotel room makes more than 8% – you won’t get it. It doesn’t matter if it makes less than 8% – they should be obliged to still pay you 8%, if they’ve got the money from their other hotel rooms or other sources.

In addition, with these investments, the promoter of the scheme also frequently offers to buy the investment back from you at a fixed future date, e.g. 5 years or 10 years. (See “Buy back options” below.) They often offer to do so at the original price or a multiple of it (e.g. 125% of what you paid). This makes your returns even more dependent on the financial strength of Acme Investments, and whether they will have enough money to honour their “buy back” option in 5 or 10 years’ time.

The return of your investment depends on the financial strength of Acme Investments Ltd, and before investing into Acme Investments you should do full due diligence on the company (see “Due Diligence and what it means” below).

How much is a hotel room worth?

In theory, of course, if Acme Investments goes bust you still have the hotel room.

However, the value of a hotel room in a hotel I don’t own depends entirely on what I can get from putting guests in it – and what if the hotel doesn’t want to let my guests in? They own the front door.

When buying a property, either for your own use or as an investment, you don’t simply pay what the estate agent asks for it. The estate agent works for the seller. You hire a valuer who works for you to check that the house is worth what they are asking. Similarly, if someone offers you a hotel room for a fixed price, you shouldn’t proceed without hiring a valuer who works for you, instead of the scheme who is selling it to you, to check that the price is reasonable.

This is also a lovely picture of a hotel, but again it’s irrelevant to an investment offering a fixed return.

There is typically very little secondary market for investments in individual hotel rooms independent of the promoter of the scheme. Why would anyone buy a second-hand hotel room from an investor with no guarantee of returns, when they could get one directly from the investor’s scheme offering a fixed return of 8-12%?

Buy back options

Because there’s a very limited secondary market for hotel room investments, the promoter has to come up with a way for investors to exit their investment. (If there was no way to exit the investment, the investor’s payments of 8-12% per year would just be their own money being paid back to them.)

Typically these investments offer a “buy back” option where after a fixed period (e.g. 5 or 10 years), the investor can sell the investment back to the promoter, in exchange for either their original capital back or a multiple of it (e.g. 125%).

Like the 8-12% yearly returns, the “buy back” option depends on the financial strength of the company offering the investment scheme.

Which of these three hotels is more likely to return 10% per annum? Answer: Nobody knows. The finances are what matter.

The small print of the investment terms may say that the buy back option is at the promoter’s discretion. Even if it is not discretionary, the buy back option is of little use if, when the five year or ten year period expires, the promoter says they do not have the funds to honour it.

Due diligence

The term “due diligence” is much abused in the investment business. The following are not, in isolation, due diligence:

Reading investment literature provided by the scheme

Talking to the scheme’s management

Looking at the property they own

Due diligence would at a minimum consist of the following:

Checking the debt cover ratio (Acme Investments’ profit, divided by the amount it needs each year to pay its debts) and other key financial indicators

Reviewing its accounts (not just published annual accounts, but the monthly management accounts as well)

Reviewing its business plan and financial projections, and determining whether its modelling makes sense and the assumptions behind them are reasonable

Ensuring that the figures are consistent and have been audited by a reputable firm of accountants

All of the above should be second nature to anyone considering investment into an individual company.

The average yield on regional hotel properties is currently 4.25% per year according to Savills. Investors who are being offered 8-12% a year from a hotel investment need to ask what makes their hotel so much more lucrative than other hotels, and whether this is sustainable for however many years their money will be locked up before they can exit (e.g. via a buy back option).

These are investments into early-stage, micro-cap companies

The smallest company on the UK’s smaller companies index (FTSE AIM) is £186 million in size (market cap) at the time of writing (Amerisur Resources). The companies that offer hotel room investments are typically much much smaller than this, and many launched less than five years ago.

As these companies are unlisted (they are privately owned and not traded on an exchange like FTSE AIM), their size can be found by looking them up on endole.co.uk (other Companies House aggregators are available) and looking for the “Net Assets” figure.

So we are not talking about investment into smaller companies. Fevertree Drinks (market cap £4 billion) is a small company. Amerisur (£186 million) is a very small company. A company with £2 million in net assets offering investment in hotel rooms is a really-really-really-tiny microcap startup company.

This picture isn’t even relevant to the article, let alone returns of 8-12% per annum.

Investment into any individual company, no matter how big, is extra-high-risk with the potential to lose up to 100% of your money (see Carillion, BHS, Enron, etc). Other things equal, the risk is much higher for smaller companies than it is for FTSE-100 listed “blue chips”.

At this point some might say “but it’s an investment in a hotel room not a company”. If so, go back and read “These investments are investments in a company, not in a property” again. If necessary, read it again, go to bed and then resume reading this article tomorrow. If a company offers you a fixed return of 8-12% per annum then you are investing in the company and it is the company’s finances that matter. The hotel room is irrelevant unless the company stops paying the 8-12% per annum, which you presumably hope it won’t.

Investors who are not experienced investors in micro-cap startups should ask what it is about these particular startups that they find attractive. They should bear in mind that the Government offers tax incentives for investing into startup companies, such as Venture Capital Trusts or Enterprise Investment Schemes. These tax incentives are not available to hotel room investments.

They should also ask whether a fixed return of 8-12% per annum is a decent return for investing in a micro-cap startup company.

Regulatory status

All these investments are unregulated in the UK. The Financial Conduct Authority takes little interest in these schemes. If an investment goes wrong the investor will not be able to seek redress from the Financial Ombudsman Service or the Financial Services Compensation Scheme, unless an FCA-authorised adviser advised them to invest.

For contrast, in the United States of America, investment schemes such as these (where an investment is sub-divided and the parts sold to individual investors, and the investors pass responsibility for generating a yield back to the promoter of the scheme), are still required to register with the Securities Exchange Commission.

The idea that the investors are each managing their own investments (like buy-to-let investors) and therefore the organiser does not need to apply for SEC registration was demolished back in 1946, in the case of SEC v. W J Howey Co. The Howey case involved orange groves which were subdivided and the parts sold off to investors. The investors’ plots were than “leased back” to the Howey company who were responsible for generating a return for investors; the Howey company advertised potential returns of 10% per annum.

The Howey scheme was identical in structure to the hotel room investments being offered today, only with orange groves in place of hotels.

The Howey company claimed that their investment wasn’t subject to regulation as the investors were investing in individual orange grove plots. The Supreme Court ruled that the scheme was in reality a security and required SEC registration. The “Howey test” is still applied today and works on the lines of “if it looks like a duck, and quacks like a duck…”

The Howey test is not applied in the United Kingdom. In the US, the Securities Act requires that any investment security must be registered with the SEC, unless it qualifies for specific exemptions. The UK’s Financial Services and Markets Act is more specific and only requires that collective investments are registered with the FCA.

This allows a much greater variety of unregulated investments to be run in the UK compared with the US. Hence the proliferation of hotel room and similar investments, which would not be allowed in the US without SEC registration as they would fail the Howey test. Investors should bear in mind that the reason these hotel room investments exist is that the UK’s looser securities laws allow such investments to be promoted to the public without FCA registration.

Should I invest in a hotel room (or airport parking space, or care home room, or any other individual unit in a wider property offering a fixed rate of return)?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

Unregulated investments of this nature are only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of 8-12% per annum or more should be considered very high risk. As an individual security with a risk of total and permanent loss, investment in hotel rooms, parking spaces, care home rooms, student accommodation rooms, and similar investments is higher risk than a mainstream stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the promoter of the scheme ran out of money to pay fixed returns or buy my investment back, I was unable to generate any yield for my investments, there was no secondary market and I lost up to 100% of my money?

Do I have a sufficiently large and well-diversified portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for a “guaranteed” or “assured” investment, you should not invest in unregulated investments with a risk of 100% capital loss.

Solidus Technologies Limited is offering unregulated 3 year bonds paying interest as follows:

Three-year Fixed Term Bond: 10% annual interest in year 1, 3% per quarter (12% per year) in years 2 and 3, plus 10,000 alternative cryptocurrency coins for every £10,000 invested.

High Net Worth Fixed Term Bond: for investments above £100,000, the terms are as above but the quarterly interest is 3.62% instead of 3% in years 2 and 3.

Three-year Compounded Bond: interest of 37.9% paid at the end of the three year term (11.3% compound interest), plus 10,000 alternative cryptocurrency coins for every £10,000 invested.

High Net Worth Compounded Bond: for investments above £100,000, as above but the interest is 44.21% (13.0% per year) instead of 37.9%.

The FAQ in the Information Memorandum states that investors can ask for their holdings to be redeemed early at the anniversary of their investment. This is at the discretion of Solidus Technologies’ director, and their ability to do so will depend on whether Solidus has enough liquid funds available.

Despite the similarities to the Viderium bond reviewed last week (both are soliciting investment to fund cryptocurrency mining, both have an insurance policy with Assicurazioni Generali S.p.A. brokered by Willis Towers Watson, both employ Bluewater Capital Ltd as a Security Trustee, both companies were founded in December 2017) the two companies are unrelated as far as I can tell. The two companies have different directors, and Solidus aims to invest in a data centre in Romania whereas Viderium’s facilities are in Hampshire and Rotterdam.

Who is Solidus Technologies?

Scott Cannon, Solidus Technologies CEO and owner

No details of who runs or controls Solidus Technologies is provided on Solidus’ website, although the Information Memorandum does disclose that the company’s sole director (and shareholder) is Chief Executive Officer Scott Cannon.

Solidus Technologies Limited was incorporated in December 2017 and due to its young age is yet to file accounts with Companies House.

How safe is the investment?

These investments are unregulated corporate loans and if Solidus defaults you risk losing up to 100% of your money.

The purpose of the bonds is to allow Solidus Technologies, in partnership with a Romanian company (Soft Galaxy International & Block Chain Development), to build a new data centre in Bucharest, Romania, which will mine cryptocurrency.

If Solidus fails to make sufficient returns from its cryptocurrency mining, or for any other reason Solidus runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Solidus’ literature is very clear in this regard, with page 2 of the literature stating “Investing in the Company is speculative and involves a significant degree of risk to invested capital”, and a comprehensive list of risk factors included later in the literature.

According to the literature, Solidus plans to raise £10 million, of which £1 million will be used to build the data centre and £6 million used to buy computer equipment (graphics cards). The other £3 million will be used to cover the costs of marketing this investment to investors.

30% of £10 million = £3 million

Asset-backed security

Investors have a first legal charge over the company’s assets, with Bluewater Capital Limited appointed to act as Security Trustee.

Investors should not assume that because their loans are secured on these assets, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed bonds have been known to lose 100% of their money (e.g. Providence Bonds and Secured Energy Bonds) when it turned out that the company’s assets were insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Solidus, only illustrating the risk that is inherent in any corporate loan note even when it is asset-backed.

If investors plan to rely on this security, it is essential that they undertake professional due diligence to ensure that in the event of a default, Solidus would have enough valuable and liquid assets to raise sufficient money to compensate all investors, as well as any other creditors that Solidus has borrowed money from.

Solidus’ literature states “In the absence of a negative pledge clause, the Company is entitled to issue further series of Bonds and other loan arrangements. This could negatively affect bondholders claim [sic] on company assets.”

“Insured” bonds

Solidus has an insurance policy with Assicurazioni Generali S.p.A. which covers it against “any Actual or Alleged act, Error, Misstatement, Misleading Statement, Omission, Neglect or Breach of Duty or loss.”

Investors should note that, as Solidus says in its literature, “This policy is not a Performance or Financial guarantee, it does NOT provide an indemnity if the Company’s performance, strategy or business activities are unsuccessful and it is unable to meet the obligations to bondholders.” (bolding is as per the original)

Cryptocurrency bonus

At the end of the term, investors receive a bonus of 10,000 “alternative crypto coins” for every £10,000 invested. Exactly which cryptocurrency investors will receive is not specified. Later in the literature Solidus’ states that “these coins/tokens will be chosen by the company that they believe have the potential to have maximum growth potential.”

It is interesting that part of the return is paid in a fixed number of coins in an unspecified cryptocurrency. Imagine if I said that I was going to pay part of your return in 10,000 conventional currency units, but I didn’t specify whether I was going to pay you 10,000 pounds sterling or 10,000 Turkish lira.

Given that Solidus’ has promised to buy a specified number of coins (10,000 for every £10,000 invested) by the end of the term, their choice of coins will be restricted by the amount of money (conventional or crypto) that they have left over to purchase alternative coins, after they have paid out investors’ fixed returns each year.

Hypothetically speaking, Solidus could identify a cryptocurrency with really terrific growth potential, but be unable to buy it because it already trades significantly above £1 per coin, meaning that Solidus couldn’t realistically afford to buy 10,000 for every £10,000 invested. Investors would rather have 1,000 of a high-growth-potential cryptocurrency than 10,000 of a lesser-growth-potential cryptocurrency, but Solidus’ arbitrary promise to deliver 10,000 units of an unspecified cryptocurrency would tie their hands.

Given that investors cannot have any idea how much their 10,000 bonus cryptocurrency tokens will be worth at the end of the term, it is safest to disregard the “bonus” part of the offer and assess the bond purely on the conventional currency returns (i.e. the 10% in year 1 and 12% in year 2 and 3 for the first version of the bond).

Regardless of how skilled Solidus management are at identifying cryptocurrencies that will rise in value, there is still a risk that the coins they allocate to investors will be worthless or untradeable at the end of the term.

Should I invest with Solidus?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering yields of up to 13% each year should be considered very high risk. As an individual security with a risk of total and permanent loss, Solidus’ bonds are higher risk than a mainstream diversified stockmarket fund.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for an investment that is fully insured against the risk of capital loss, you should be looking at deposit accounts protected by the Financial Services Compensation Scheme, rather than unregulated bonds with a risk of total and permanent loss.

Buy 2 Let Cars Limited offers the opportunity to invest in lease cars over a term of three years as follows:

Level 1: invest £7,000-£10,000 and receive a return of 7% per year

Level 2: invest £14,000 to fund “one unit” and receive a return of 9% per year

Level 3: invest to fund “two to six new units” (presumably £28,000 – £84,000) and receive a return of 10% per year

Level 4: invest to fund “7 or more units” (£98,000 or more) and receive a return of 11% per year

Investors’ funds are used to purchase a lease car (or multiple cars) which is then leased out to a borrower. The borrower’s lease payments are used to generate the promised return.

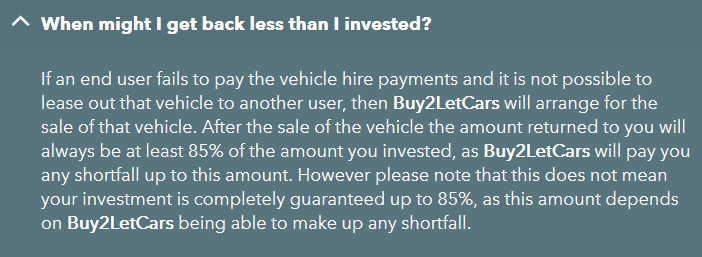

If the borrower defaults on their payments, and Buy 2 Let Cars is unable to find another borrower, Buy 2 Let Cars will attempt to sell the car to return investor’s capital. If the amount realised is less than the investor invested, Buy 2 Let Cars promises to make up any shortfall up to a maximum of 85% of the amount invested.

Buy 2 Let Cars consists of three companies: Buy 2 Let Cars Ltd, Rent 2 Own Cars Ltd (trading as Wheels 4 Sure) and the parent company Raedex Consortium Limited. For the remainder of this article, Buy 2 Let Cars (which is the name the group uses most often) refers to the whole group or investment, unless otherwise specified.

Raedex Consortium Limited is regulated by the FCA for its car leasing activities, but the investment opportunity is unregulated.

Who is Buy 2 Let Cars?

L: CEO Reginald Larry-Cole. R: Operations Director Scott Martin.

Buy 2 Let Cars was incorporated in 2012.

The parent company, Raedex Consortium Limited, is 90% owned by the founder and CEO Reginald Larry-Cole. The remaining 10% is owned by Operations Director Scott Martin.

How safe is the investment?

This is an unregulated investment into lease cars (and, in terms of the promise to return at least 85% of your capital, Buy 2 Let Cars itself) and you risk losing up to 100% of your money if Buy 2 Let Cars:

fails to generate sufficient returns from its car leasing agreements to sustain returns of 7-11% per annum,

and runs out of money to compensate investors up to the promised 85%.

As investors are relying on Buy 2 Let Cars to make up any shortfall if the lease payments are insufficient to pay returns of 7-11% per annum, this is not just an investment into a car, but into Buy 2 Let Cars as a company.

Buy 2 Let Cars Limited’ last accounts (up to December 2016) show net assets of £1.3m, comprising roughly £19.5m in debtors, £1.5m of cash in the bank, and £19.7m of creditors (predominantly investors’ money). Note that these accounts are unaudited (due to Buy 2 Let Cars Limited’ small size) and are from a year and a half ago.

Buy 2 Let Cars Limited did not file a profit and loss account (again due to its small size), but note 1.2 in the accounts under “Going Concern” shows that the company was loss-making at the time.

As a result of the delay and in anticipation of lower volumes and margins than planned in respect of used car activities, the earlier projections of positive Earnings Before Interest Tax Depreciation and Amortisation (EBITDA) throughout 2017 and profitability achieved from activities in the last quarter of the year will not be realised.

The Directors have therefore conducted a further review of the underlying private customer leasing business model which culminated in a new marketing strategy and rebranding of the businesses at the end of the first quarter of 2017…

…The directors are confident that the business will yield positive EBITDA in the final quarter of 2017 and become profitable at a pre-tax level from the beginning of 2019.

Investors should ensure they do full due diligence on Buy 2 Let Cars, including obtaining details from the company of its up to date funding position, before investing.

Potential collective investment

Under the Financial Services and Markets Act, it is illegal to run a collective investment scheme without authorisation from the Financial Conduct Authority. Raedex Consortium Limited is an FCA authorised company, but is not authorised to run a collective investment scheme (its authorisations relate to the vehicle leasing side).

Buy 2 Let Cars represents to investors that they are investing in individual cars. Investment in individualassets (such as shares, flats, hotel rooms, store pods, etc etc) is in itself not a regulated activity, whereas a collective investment is. (We don’t make the rules.)

So if Buy 2 Let Cars investors were purely investing in individual cars, with each investor receiving only the returns attributable to their individual car, Buy 2 Let Cars’ investment scheme would not be considered collective and they would not require authorisation to run the investment.

However, Buy 2 Let Cars promises that all investors will receive at least 85% of their capital back, even if the car they invest in is completely written off.

Under UK legislation, there are three prongs to the definition of a collective investment scheme: a) the investor must not exercise day-to-day control of the investment, and either b) “the contributions of the participants and the profits or income out of which payments are to be made to them are pooled” or c) the property is managed as a whole by or on behalf of the operator of the scheme.

A) is quite clearly the case with Buy 2 Let Cars; Buy 2 Let Cars openly promotes the fact that its investment is “hands-free”.

There is a risk that Buy 2 Let Cars’ promise to return at least 85% of investors’ capital to investors may be deemed by the FCA to represent B), pooling of contributions and profits.

This is however not a certainty, as Buy 2 Let Cars could argue that the funds it uses to fulfill its 85% promise come from elsewhere.

Whether or not Buy 2 Let Cars is deemed by the FCA to be running a collective investment scheme without authorisation, investing with a company that is not authorised to operate collective investments represents a regulatory risk. Investors will need to ensure they are happy with this regulatory risk before they proceed.

Should I invest with Buy 2 Let Cars?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual investment security, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 11% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Buy 2 Let Cars is higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

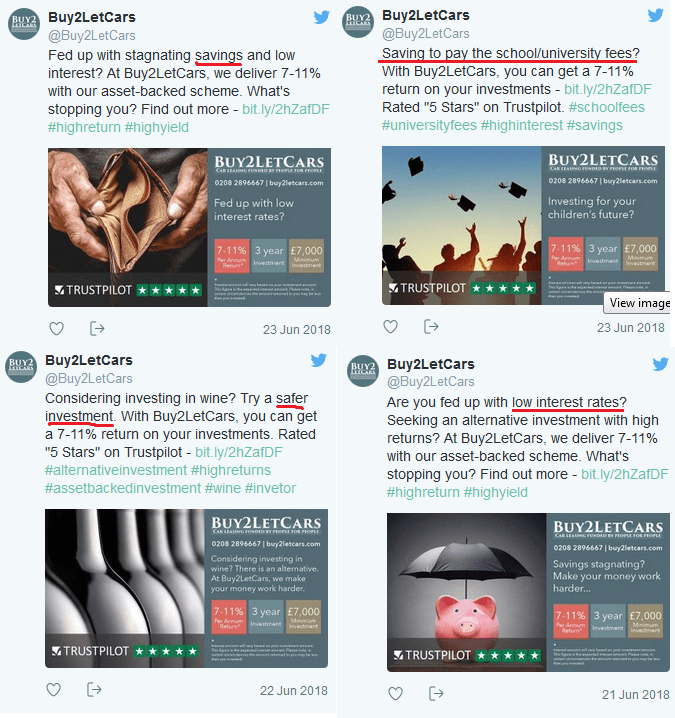

Buy 2 Let Cars runs adverts on Sky and on Twitter that urge potential investors to consider Buy 2 Let Cars as an alternative to a savings account, and refer to their product as a “safer investment”.

Novice investors who have previously only invested in deposit accounts, are unhappy with the returns, and want to start taking some risk, should first consider a regulated diversified portfolio of conventional stockmarket investments. While these will go up and down in the short term, a diversified portfolio of regulated investments has minimal risk of loss in the long term provided the investor doesn’t panic and cash it in.

This investment by contrast is unregulated and has a risk of permanent and total loss due to the risk that Buy 2 Let Cars does not generate sufficient returns from your car, and runs out of money to meet its promise to pay investors up to 85% of their investment.

If you are looking for a “safer investment”, you should not invest in unregulated investments with a risk of total and permanent loss.

Viderium Limited is offering a 3 year bond paying 9.8% interest per year, paid out quarterly.

The bond is promoted as offering “A Rated Indemnity Insurance”.

Who is Viderium?

L: Ross Archer, Viderium CEO. R: Alexander Johnson, Viderium chairman and 95% shareholder.

Viderium was incorporated in December 2017 and is controlled by Ross Archer (Chief Executive Officer) and Alexander Johnson (non-Executive Chairman).

Interestingly, when it originally incorporated in December 2017, Archer held 95 of Viderium’s 100 shares and Johnson 5. However, a few days later, 1800 new shares were allocated to Johnson, so the ownership ratio swapped around to give Johnson the 95% shareholding.

Due to the company’s young age, it is yet to file accounts with Companies House.

How safe is the investment?

These investments are unregulated corporate loans and if Viderium defaults you risk losing up to 100% of your money.

The purpose of the bonds is to allow Viderium to expand its data centre operations in order to mine cryptocurrency.

If Viderium fails to make sufficient returns from its cryptocurrency mining, or for any other reason Viderium runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Viderium’s literature is very clear in this regard, with the front page stating “reliance on this promotion for the purpose of engaging in any investment activity may expose an individual to a significant risk of losing all the property or other assets invested.”

Asset-backed security

Investors have a first legal charge over the company’s assets, with Bluewater Capital Limited appointed to act as Security Trustee.

Investors should not assume that because their loans are secured on these assets, they are guaranteed to get at least some of their money back through sale of the collateral if the issuer defaults. Investors in asset-backed bonds have been known to lose 100% of their money (e.g. Providence Bonds and Secured Energy Bonds) when it turned out that the company’s assets were insufficient to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Viderium, only illustrating the risk that is inherent in any corporate loan note even when it is asset-backed.

If investors plan to rely on this security, it is essential that they undertake professional due diligence to ensure that in the event of a default, Viderium would have enough valuable and liquid assets to raise sufficient money to compensate all investors, as well as any other creditors that Viderium has borrowed money from.

“Insured” bonds

Viderium has an insurance policy with Assicurazioni Generali S.p.A. which covers it against “any Actual or Alleged act, Error, Misstatement, Misleading Statement, Omission, Neglect or Breach of Duty or loss.”

This policy is promoted heavily as an attraction of the investment; the cover page of Viderium’s Information Memorandum includes the sub-title “With A Rated Bond Indemnity Insurance”.

Investors should note that, as Viderium says in its literature, “this policy is not a Performance or Financial guarantee”. In other words, the insurance policy has nothing to do with the risk that Viderium fails to make enough from its cryptocurrency mining operations and cannot pay investors their interest and capital. If Viderium defaults in this event, the insurance policy does not cover investors.

Should I invest with Viderium?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering up to 9.8% per annum yields should be considered very high risk. As an individual security with a risk of total and permanent loss, Viderium’s bonds are higher risk than a mainstream diversified stockmarket fund.

This particular bond is described as asset-backed. Before relying on the security backing the bond, investors should undertake professional due diligence to ensure that in the event of default, the security could be easily sold and would raise enough money to compensate all the investors, after the adminstrator deducts their fees.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for an investment that is fully insured against the risk of capital loss, you should be looking at deposit accounts protected by the Financial Services Compensation Scheme, rather than unregulated bonds with a risk of total and permanent loss.

Hanover Merchant Capital is offering the opportunity to invest in lease-back contracts for the delivery of mineral water from an aquifer in New Zealand, which pay “annuity type” income of “5.29% guaranteed” each year. After two years, the contract is sold for which Hanover Merchant Capital projects “up to 30% aggregate capital return”, with the caveat that this is “subject to market prices”.

In email promotions, the investment is promoted as offering “NO Capital Depreciation” and “Secure Underwritten Investment”.

Who is Hanover Merchant Capital?

No details are provided on hanovermerchantcapital.co.uk as to who is behind the business.

Hanover Merchant Capital was incorporated in Switzerland in 2016 as Hanover Merchant Capital AG. The Swiss company registry shows that the two “registered persons” were chairman Tahar Keddech (who in May 2018 appears to have been removed as a registered person) and director Michael Gassner.

Hanover Merchant Capital was also incorporated in the UK in December 2015 as Hanover Merchant Capital Limited. The company is 100% owned by Bruce Rowan.

How safe is the investment?

These investments are unregulated commodity contracts and if for any reason Hanover Merchant Capital defaults on the promised payments of 5.29% each year, and Hanover Merchant Capital is unable to find a buyer for your water contract, and cannot make good on its “NO Capital Depreciation” promise, you risk losing up to 100% of your money.

The investment Hanover Merchant Capital is offering is a contract to deliver bottled mineral water from New Zealand. Hanover Merchant Capital says “we trade the water units on a matched bargain basis market trading with buyers and suppliers for physical delivery and transport”.

Commodities are in general an extremely volatile investment. Contracts to deliver bottled water are no exception.

As with any commodity, in 2 years’ time the contracts to deliver this water will only be worth what someone will pay for them. If Hanover Merchant Capital is unable to find a buyer for your water, you risk losing up to 100% of the money you handed over to buy the contract.

Hanover Merchant Capital’s promise of “no Capital Depreciation” is only as good as the company backing it, in this case presumably Hanover Merchant Capital. No details of Hanover Merchant Capital’s financial strength are provided in the investment literature.

Very little mention of these risks is made by Hanover Merchant Capital. The literature also states the investment offers “annuity type income”. Annuities, at least from a UK perspective, are insurance contracts which are guaranteed by regulated insurers who have to meet solvency requirements, and receive 100% protection from the Financial Services Compensation Scheme. Hanover’s water investments are unregulated and have no FSCS-protection.

Illegal financial promotions

Providing financial promotions in the UK requires the company to be regulated by the Financial Conduct Authority.

In their “About us” page, Hanover Merchant Capital claims

The origins of the company started over a decade ago (at the time regulated by the FSA now the FCA) dealing as a financial investment house for private equity clients based in the city of London and the Isle of Man but due to growth and expansion the company merged the private equity division with an International Fund Management company and de-merged the property group which today consists of HMC Holding AG (subsequent FSA regulation was transferred with the equity business separating from the property group). The company de-merged the commercial and residential property asset management portfolios in 2009.

I have read this ludicrous run-on sentence twice and I am still none the wiser on where the FCA/FSA regulation is supposed to have been transferred to – Hanover Merchant Capital in its present incarnation or the other unspecified business(es) which were de-merged from this incarnation.

The UK, Swiss and Liechtenstinian registries show that neither Hanover Merchant Capital Ltd, Hanover Merchant Capital AG nor HMC Holding AG (a company registered in Liechtenstein) existed prior to 2015/2016. Nominet shows that www.hanovermerchantcapital.co.uk was registered in August 2016. Hanover’s waffling on about mergers and de-mergers with unnamed companies does not change the fact that there is no concrete evidence that Hanover Merchant Capital existed prior to 2015, much less 2009.

Hanover Merchant Capital does not provide an FCA registration number on its website, nor does it disclose its regulatory status in emails. A search for both Hanover Merchant Capital and HMC Holding on the FCA register provided no results. The inescapable conclusion is that Hanover Merchant Capital is offering financial promotions despite being unauthorised to do so in the UK or any other country in which it operates.

Under the Financial Services and Markets Act, it is a criminal offence for an unregulated firm to offer financial promotions to the UK public.

Should I invest with Hanover Merchant Capital?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated investment into individual commodity contracts, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering 5.29% per annum yields plus a projected 30% return after 2 years (a total projected return of 19.3% per year) should be considered extremely high risk. As an individual security with a risk of total and permanent loss, Hanover’s water contracts are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if Hanover was unable to find a buyer for my water contracts, pay the promised 5.29% returns or back up its “NO Capital Depreciation guarantee”, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for an investment which guarantees “no capital depreciation”, you should not invest in unregulated investments with a risk of 100% loss.

Intergroup Mining Limited is an Australian gold mining company offering unregulated 12% convertible loan notes paying 12% per year over three years.

Who are Intergroup Mining?

According to Intergroup Mining’s website, the directors are Walter Doyle (CEO), Brian Stockridge (Non-Executive Chairman) and Stephen White (director).

Doyle and Stockridge are also CEO and Chairman respectively of NQ Mining, a listed Australian penny share mining company (listed on the NEX exchange at 10p a share at time of writing).

How safe is the investment?

These investments are unregulated corporate loans and if Intergroup Mining defaults you risk losing up to 100% of your money.

The purpose of the bonds is to allow Intergroup Mining to mine gold in the Brilliant Brumby mine.

If Intergroup Mining fails to make sufficient returns from its gold mine, or for any other reason Intergroup Mining runs out of money to service these bonds, there is a risk that they may default on payments of interest and capital to investors.

Intergroup Mining may well have struck gold in its gold mine, but its ability to repay the capital and interest will depend on whether it can extract and sell the gold profitably enough to pay its bondholders 12% each year, and have the mine profitably up and running within three years (when repayment becomes due).

The investor documents I have seen contain a lot of detail about the geological details of Intergroup’s mine but virtually no details on what Intergroup’s expected revenues and costs are, which is what matters to bond investors.

Convertible notes

The shares can be converted to equity shares at the current share price.

As Intergroup Mining is not listed on any stock exchange, it is likely to be very difficult to sell shares in Intergroup Mining for as long as that remains the case.

If investors convert their bonds to equity, they are still subject to a risk of total loss (as with any individual equity share) if they are unable to ever find a buyer for their shares.

Should I invest with Intergroup Mining?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any unregulated corporate bond, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering 12% per annum interest should be considered very high risk. As an individual security with a risk of total and permanent loss, Intergroup Mining’s bonds are higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted, the sale of the security failed to raise enough money to compensate all investors, and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If I plan to exercise the option to convert the bonds into equity shares, am I comfortable with the fact that my capital could be locked up indefinitely, as Intergroup Mining shares cannot be sold on any recognised exchange?