The administrators of collapsed unregulated property investment scheme Harewood Associates, Begbies Traynor, have released their first report.

Subsequent to the report, Harewood director Peter Kiely has signed a Statement of Affairs detailing how much of the company’s assets remain to be realised to investors.

An anonymised list of creditors shows that a total of £31.8 million was invested by 878 investors in its loan notes, an average of just over £36,000 per person. Amounts owed to creditors ranged from £5,000 to the largest investment of £788,481.

Currently unknown is the amount invested in shares issued by Harewood in Special Purpose Vehicles. At the moment administrators are deciding whether Harewood SPV investors should be considered creditors. Normally a shareholder of a company is not a creditor.

Back in 2016 Harewood claimed in a web promotion for their bonds:

If in the event that the Company did go into liquidation, the assets of the company would be sold off and the investors would be repaid. As we have substantial equity within each project, even at forced fire sale prices, there would be enough to repay the investors and deal with any staff, legal and accountancy commitments.

Turns out this was an aggressively overoptimistic statement.

According to the Statement of Affairs, Harewood loaned a total of £40.5 million to other related companies.

Of this, only £3.9 million is expected to be realised.

A £5,000 loan from a Paul Kiely, a £300,000 freehold property and £468 of cash in the bank brings the total estimated realisations to £4.2 million.

The administrators’ report lists a total of 9 related companies which owe money to Harewood. The administrators have written off 4 of these as not expected to provide any recovery. This includes the largest debts of £16.7 million owed to Harewood Venture Capital (which initially owned the liability of the investor creditors, but this was transferred to Harewood Associates in May 2018) and £19.2 million loaned to Sherwood Homes.

HVC is in liquidation (Begbies Traynor have taken over from the Official Receiver) while Sherwood Homes is still in existence, but has ceased to trade and holds no assets according to Peter Kiely.

As for the other five companies, the administrators are uncertain as to whether they will get anything from 3, and from the other 2 they anticipate getting something but cannot say how much.

The administrators have said that 84% losses before their costs is the current best case scenario. However this assumes that the five companies not already written off pay their debts back in full. Given the record of the other four, this would appear to be an optimistic assumption. In addition, the administrators’ fees (estimated at £276k as it stands) will come out before any payment is made to investors.

Equiscale

The administrators also refer to a company called Equiscale Limited which was acquired in March 2018 for £1.2 million. Equiscale owned a company called Geo. Noblett (Plant Hire), which in turn owned some land in Blackburn. The land was transferred to another Harewood company, Heron Homes, in April 2018 for £1.16 million. According to the administrators, Heron never paid Geo Noblett for the land.

Peter Kiely claims the shares in Equiscale were transferred to another company, Clifton Argyle Limited, in March 2018 and the proceeds deducted from money owed by Harewood to Clifton Argyle. The administrators say they “have not been provided with any evidence of this transaction and we are continuing with our investigations”.

So, in summary, Harewood used to own a company, but it doesn’t any more, and that company used to own some land, but it doesn’t any more, and it was never paid for that land, but as Harewood doesn’t own the company that wasn’t paid any more, that would seem to be moot from the investors’ perspective. In line with his statement to the administrators, Peter Kiely’s Statement of Affairs does not list the Equiscale investment.

How the bonds were sold

Harewood illegally promoted its loan notes and SPV shares directly to investors, claiming it was exempt from the Financial Services and Markets Act because it was a property company.

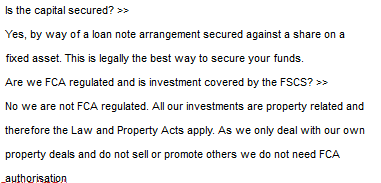

Are we FCA regulated and is investment covered by the FSCS?

No we are not FCA regulated. All our investments are property related and therefore the Law and Property Acts apply.

The reality is that loan notes and shares issued by a property company are subject to the FSMA just like any other loan note or equity security. Companies which promote securities to the public in the UK require authorisation from the FCA. Neither Harewood Associates nor its directors were authorised by the FCA.

As pseudolegal gibberish goes, Harewood’s argument is a bit like me encouraging the public to invest in bonds paying 12% per year in my kebab van, and saying I’m exempt from the Financial Services and Markets Act because I’m a kebab van and therefore the Food Safety Act applies.

Not only were investors investing in loans not property; it turns out that they weren’t even investing in loans to a property company. They were investing in loans to a company which made loans to other companies.

Despite Harewood claiming on the 2016 version of its website

Investments are secured by way of debentures on UK residential developments

and

All our investments are property related

a significant proportion of the underlying loans in Harewood Associates were, according to the administrators’ report, not secured on property. The administrators have written off four out of nine companies which owe Harewood Associates money. Which means that either these loans from Harewood Associates aren’t secured on anything, or if they are, the security is worthless according to the administrators.

These four debts account for £36.6 million of the £40.5 million owed to Harewood Associates – just over 90%.

What if anything will be realised from the other 10% is currently highly uncertain.

In a video promotion uploaded to YouTube in 2013, Harewood Associates claimed its bonds were “safe and secure” despite offering a “market beating rate of 12% per annum”.

So who are the Kielys?

For Harewood Associates director David Kiely, the experience of having his business collapse will be wearily familiar.

Back in 2005 David Kiely’s former business S-Mart Stores collapsed. A year later a pub company called Provence and another company called Do It Right UK, both owned by David’s brother Paul (the same one who loaned Harewood £5,000?) also collapsed.

The Morning Advertiser (a pub trade paper) reported back in 2006:

Paul Kiely’s brothers David and Shaun Kiely ran a firm, S-Mart Stores, that collapsed in identical fashion to Provence a year ago. Both firms sold hugely overvalued freehold properties to private investors on the promise of inflated rents.

[MP Jim] Dobbin tabled an Early Day Motion in the House of Commons in March 1998 which decried the activities of Provence founder Paul J Kiely and his brothers.

He described Kiely Developments as cowboy builders who “continually flouted builders regulations”. A year later the company, where Paul Kiely and brother Shaun Kiely served as directors, collapsed. This week Dobbin said: “I am not surprised to find that members of this family have been involved in a company which has again let down the people they claim to be working for. The Department of Trade needs to look seriously at their suitability for holding directorships. Maybe it is time for a fraud enquiry.”

As far as I can tell no fraud enquiry was ever launched, and you can’t blame one businessman for the failed businesses of their brother. There is therefore no suggestion that there was anything illegal about any of the Kielys’ businesses collapsing.

Nonetheless, it is difficult to see why any potential lender conducting basic corporate finance due diligence into Harewood Associates would not read about the collapse of David Kiely’s former business and the business history of the Kiely family as a whole, and ask serious questions about the history of the directors, and whether their investment opportunity was as secure as they claimed.

But it is easy to say such things with hindsight. Harewoods investors weren’t doing due diligence. They thought they were investing in property so none was needed.

The fundamental belief behind the Financial Services and Markets Act is that novice investors who do not know what due diligence is, are not skilled in carrying it out, and do not know when they should carry it out, should not have high risk unregulated securities promoted to them by unregulated companies.

But Harewoods believed that didn’t apply to them because something something property.

So here we are.

£32.8 million raised from investors on the basis of illegal and misleading financial promotions and nearly all of it has disappeared.

No action has been taken against Harewood or their directors by the FCA or any other government body that is currently in the public domain.

harewood also have according to companies house shares in a number of the spv’s but these are not shown anywhere in harewoods accounts also as a small enterprise according to PK how was it even possible for hm to make a 32.8 million yes million loss in less than one year ………

Absolutely astonishing nothing ever gets done to con men like these.

Having been approached over the last year by a stream of cold-call scammers, to one of whom, which was registered with the FCA, I fell victim and having studied cases of how the law dealt with scammers in the rare cases that they are caught, and noted the downright silly slaps on the risk which they are dealt, I can with all sincerity say that I would support the IMPOSITION OF THE DEATH PENALTY for serious financial fraud and the scum who are mentioned in this article would be prime candidates for it.

… and the scams just keep on coming …. bit like Brexit – never ending ….

Does anyone know who the administrator is for Sherwood Homes Limited is please?

I had invested more than a quarter of a million In Harewood’s and, if the administrators “best case scenario” 16p in the £ proves to be accurate, I get back £42,000 minus Begbies fee of £275,000, which is about £309 for each investor. That leaves me with a loss of more than £220,000. If I embarked on a career of backing horses and I lost this sum, then it would be more bearable as you are gambling on a sport that you have no control on the animals you have backed consenting to run their races, plus the fact that, the odds are stacked against the punter and are heavily in favour of the bookmaker – so you have some idea what you’re getting into. Investing in Harewood was promoted as a safe “assst-backed cast iron security”, but this was all a pack of lies, now I can look forward to losing much of my life savings. Victims of fraud and scams are referred to ACTION FRAUD, but it will soon become clear after submitting your report that ACTION FRAUD will simply not bother investigating your report and come back to you with the standard response: ” We have looked at your report and find there is no line of enquiry “. So what now? Just accept the loss? Hope you get lucky on the lottery? Or do what many investors did in 1929 during the Wall street crash, and commit suicide?. The Kiely fraudsters have defrauded nearly 900 investors out of £millions of £s, but no one in authority is interested.

All there assets should be seized

Houses etc and they should face a life sentance

Lakeside developement was completed and all property was sold, but there is no bank account with the monies raised from the sale of the properties. R.A.Jordan

I got my money back £11000on the lakeside development because I kept getting eccuses

I got my money back with know interest. How look was i

C. Crutchley

I hope that they both contract an incurable diseases soon but live to be waste old men.