About a year ago, when Bond Review’s traffic had started to tick up from “my nan” to “extremely obscure”, I started serving ads via WordPress to cover the costs of hosting the blog.

The revenue from these ads goes up and down (despite the growing readership) and in terms of ad revenue v hosting costs I’m somewhere around break-even.

Put it this way, I’d have to run 100 Bond Reviews before HMRC took an interest.

In terms of time cost I’m several thousand in the red, but that’s not an issue as Bond Review has always been a hobby and was never about money (despite being about money).

I began Bond Review with a simple philosophy: if an hour or two of my time prevents someone from losing a lifetime’s worth of savings, in a high risk investment that wasn’t suitable for them, then it’s a good trade. That still stands.

I was however acutely aware that some of the ads on my blog would be for dubious investments or outright scams – for the same reason these ads appear on Yahoo or the Daily Telegraph or most other places you go on the Internet.

These ads are not selected by me, but are served by a third party based on your browser history. If someone’s been looking at unregulated investments recently then chances are high that the ad platform will show them some more.

Unfortunately I don’t have the time or connections to source my own ads, and the only practical alternative was to fund the blog out of my own pocket, which felt like a step too far.

The larger Bond Review’s readership grows, however, the more I feel uncomfortable with god-knows-what that I can’t even see appearing under my articles.

Consequently I have decided that this is it – no more ads. From today Bond Review will be completely and permanently ad-free and move to a donation model.

(If you’re still seeing ads, try clearing your cache – failing that, you may need to check for your computer for spyware.)

Guardian-style begging ads incoming…

Bond Review is approaching its second birthday and I fully intend to continue bringing you news and reviews from the underscrutinised world of unregulated investments.

I have never taken money in return for coverage negative or positive, and never will.

I’m fortunate that I can afford to pay Bond Review’s costs so far out of my own pocket but can’t guarantee how long that will continue.

So far Bond Review has faced a total of eight separate legal threats or legal attacks aimed at shutting down my entirely factual coverage, plus one or two suspected hacking attempts. Thankfully none of them have so far imperilled my ability to keep the blog up and running.

There were however a few Hero’s Journey moments when I considered pulling the whole thing offline and taking up contract bridge instead. As you can see that didn’t happen.

Support from my readers would go a long way to putting the blog on a stable financial footing and helping it continue into the future.

I don’t expect readers who are here because they’ve lost their money to donate – they’ve spent enough on this sector. This is aimed at the investors and professional advisers who have found my coverage of the sector useful for research and general interest.

A modest one-off donation to Bond Review is a hell of a lot cheaper than a lost investment, and a hell of a lot cheaper than an FSCS levy.

If you have found my coverage valuable, you can now click here to make a one-off or regular donation.

…or not

There won’t be any annoying Guardian- or Wikipedia-style ads constantly popping up all over the place, although I will be adding a monthly reminder about the donate button to the rotation. This will include a word of thanks to anyone who has been kind enough to donate – if they consent to their name being included.

If I don’t get enough to cover the blog’s costs, the ads will not return. If Bond Review becomes unviable I will just shut it down.

But with your support I fully intend to continue for a third year and beyond – for as long as there are unregulated investments being sold to the public about which they need to know the facts.

Back in August 2018 REWS were anticipating bringing their waste recycling facility online by the end of 2018, allowing it to start generating the revenue it needed to repay the £2.8 million it had borrowed from investors.

Bad news is that hasn’t happened (or not as at June 2019 when the accounts were published).

Good news is that REWS has borrowed another £10 million. Well, good assuming it eventually gets its facility online, naturally. Otherwise good news becomes much worse news.

The directors describe 2018 as “exciting but challenging”. Due to “delays in the delivery of some key electrical components” the date for bringing its facility for turning waste into renewable energy was pushed back from the end of 2018 to “the latter part of quarter 2 in 2019”. This is also the month before the company’s first 2 year bonds became repayable.

As with the last fundraise, about a quarter of the money REWS raised via its bonds was paid out in issue costs, which would include the commission it paid to its introducers. The accounts show unamourtised issue costs grew to about £3.4 million against a total of £13.2 million outstanding to creditors.

REWS raised funds via 2 year bonds paying 8-12% per year and 4 year bonds paying 10-12% per year. A relatively small amount in bonds paying 20% per year (£159k) will mature in 2019.

Its published net assets now stand at minus £3.6 million and its auditors have noted the material uncertainty over whether the company will continue as a going concern, which will depend on whether it can belatedly get its rubbish power plant up and running, and generating returns of up to 12% per year after costs. (Including the cost of paying a quarter of funds raised out in issue costs.)

Quinshaw Finance is offering unregulated bonds paying returns as follows:

4.58% for a 1 year term

9.25% per year for a 3 year term

11.58% per year for a 5 year term

Via its Google search result and brochure, the company claims to offer “secure property high yield bonds” and that “investor protection is our number 1 priority”.

Funds raised are to be used to provide short-term bridging finance to property developers.

Who are Quinshaw?

No details of who is behind the business are provided by Quinshaw’s website.

Companies House shows that Quinshaw Group Limited is wholly owned by its sole director, Paul Hopeton Daye, who took over and renamed an existing company called Nobleleigh Limited in May 2019.

Partly due to the lack of information provided, I was unable to put together any kind of biography for Daye.

Quinshaw Finance filed its first accounts to June 2019 shortly after Daye took over the company, which show £3 million in net assets. These accounts were however unaudited. Moreover they appear to predate the offering of Quinshaw’s bonds, as they show almost no creditors.

How safe is the investment?

Despite Quinshaw’s claim that its bonds are “secure”, the reality is that these are loans to a small unlisted company and carry an inherent risk of 100% loss.

Secured lending on property is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Quinshaw, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not Quinshaw) to confirm that in the event of a default, the assets of Quinshaw would be valuable and liquid enough to compensate all investors. Investors should not simply rely on what Quinshaw tells them about their assets.

Note that while Quinshaw states that it takes security on properties when it lends out investors’ money to property developers, the assets that Quinshaw itself holds will consist of short term loans, not property.

If investors are relying on the assumption that Quinshaw’s loans are secured on property valuable enough to repay investors in the event that Quinshaw’s borrowers failed to repay it, they will need to undertake a full due diligence investigation into Quinshaw’s loan book and the value of the properties it is secured on.

Quinshaw claims in its brochure that it has a “100% Track Record of repaying bondholders all their capital”.

This claim is always meaningless – and especially meaningless for Quinshaw given they only started taking investments a few months ago.

No bondholders have been repaid all their capital yet because Quinshaw’s first investors won’t be due to be repaid their capital until the summer of 2020 at the absolute earliest. (Based on the company’s minimum investment being one year and the fact that the company’s accounts show it had raised little or nothing from investors as at 30 June 2019.)

Should I invest in Quinshaw Finance?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted startup company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of up to 11.58% per year is inherently very high risk. As an individual, illiquid security with a risk of total and permanent loss, Quinshaw’s loan notes are much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

Have I conducted due diligence to ensure the asset-backed security can be relied on?

If you are looking for a “secure” investment, you should not invest in corporate loans with a risk of 100% loss.

We believe this firm has been providing financial services or products in the UK without our authorisation. Find out why to be especially wary of dealing with this unauthorised firm and how to protect yourself from scammers.

Hanover Merchant Capital claimed to provide “annuity type income” returns of over 20% per year from investing in bottled water from New Zealand. I reviewed the investment in June 2018. In November 2018 the company did a runner, closing its website and ceasing to communicate with investors.

In March 2019 Hanover’s Swiss entity was dissolved after the Swiss liquidators found no assets. In the same month its UK entity was put into liquidation.

Liberty House Capital popped up a few months after, offering an almost identically nonsensical spiel with New Zealand bottled water replaced with Australian water.

The FCA’s warning over Hanover is clearly pointless, as it shut down almost a year ago, but appears to have been issued in tandem with a warning about its reboot scam, Liberty House Capital. Liberty House Capital’s website is still up at time of writing.

Since it ran off with everyone’s money, Hanover investors have been strung along by its director, Bruce Rowan (or someone claiming to be him), continually promising jam-tomorrow returns on an increasingly fluid future date.

No official news has emerged from the Official Receiver about the winding up of Hanover Merchant Capital’s UK entity since the court order was granted in March.

How do I get my money back from Hanover Merchant Capital or Liberty House Capital?

Your money has been stolen by scammers and the chance of recovery is minimal.

Investors who fell for this scam should change their contact details as they are likely to be targeted by – and fall for – similar scams in the future.

If anyone contacts you claiming they can recover your money, it is almost certain to be another scam. They will ask you for “legal fees” or similar which you will never see again.

If you were advised to invest in either company by an FCA-authorised adviser, you may have a claim against them which would be covered by the Financial Services Compensation Scheme. However it appears unlikely that even a corrupt FCA-authorised adviser would have recommended either.

The administrators of Mederco, which ran a number of unregulated investment schemes including one involving spaces in the Bury FC car park, have released a six-monthly progress report.

Since the initial proposals in March, a secured creditor has emerged, Capital Bridging Finance Solutions. CBFS loaned £333,000 to Mederco secured on a basement car park in Bradford. Mederco director and former Bury owner Stewart Day had told the administrators that this had been repaid. CBFS have now told the administrators this was inaccurate and that £152,291 remains outstanding.

Capital Bridging Finance Solutions has raised funds from investors via Capital Bridge ISA bonds paying 9% per year, reviewed here in October 2018. Hopefully the rest of their loans to “hand-picked property developers in the UK” are going a bit better. Capital Bridge states that it “takes significant security on all loans”. Whether the basement car park is sufficiently valuable to get its investors’ money back from Mederco remains to be seen.

(Thanks to reader Adam Smith for spotting the connection.)

CBFS’ outstanding loan is a secured one and ranks ahead of car park investors whose “guaranteed” payments were defaulted on, and anyone else who isn’t the administrators. Realisations are not anticipated to be enough to repay CBFS in full. As expected in the original proposals, total losses are therefore anticipated for unsecured creditors.

Bury FC

Substantial sums were invested by Mederco in Bury FC. The exact amount owed by Bury FC to Mederco could not be ascertained. Funds transferred from Mederco to Bury FC were treated as loans and subsequently converted to shares in the club. The administrators note that the share capital of Bury FC increased by approximately £5 million under Stewart Day’s tenure as at May 2017.

As anyone who takes an interest in English football knows, Bury FC is currently undergoing a Company Voluntary Arrangement. Had Mederco proved a “significant claim” against Bury FC, the administrators believe Bury FC would have been wiped out. The success of the Company Voluntary Arrangement is depedendent on football creditors being paid off by third parties, and Mederco enforcing whatever claim it has against Bury FC would have scuppered that, probably without any return to Mederco.

The administrators have therefore sold any claim Mederco may have to an unspecified “corporate entity”, with a personal guarantee, for a fixed sum of £70,000. (Who has provided the personal guarantee is also unspecified.) £20,000 has been paid as at the date of the report, with a further £50,000 due in monthly instalments up to January 2020.

The £20,000 initial payment is the only asset realised by the administration as at the date of the report.

Administrators to attempt to sell the remaining parking spaces

As described in our earlier article, Mederco developed a block of flats in Bradford known as Appleton Point. Mederco sold the flats to investors with a guaranteed yield of 9% per year.

Mederco sold the the freehold of Appleton Point in May 2015 to E & J Ground Rents No 1 LLP for £850,000, who subsequently leased the basement car park back to Mederco for 999 years at a peppercorn rent. Mederco then sold the car parking spaces to another batch of investors for £9,995 each, again for a guaranteed yield of 9% for five years with an uplifted buy-back after that.

Appleton Point failed a fire inspection earlier this year and residents were ordered to leave the property with 15 hours’ notice. The property management company is attempting to obtain the necessary funds from the long leaseholders to make the property safe.

The administrators state in the report that once the fire safety works have been completed, “we will look to market the six remaining under-leases for sale at the previously achieved price of £9,995 per space”.

Um, good luck with that.

Nobody is going to buy a car parking space in Bradford for £9,995 if it doesn’t come with a supposed guarantee to pay 9% a year. If Mederco could have sold the parking spaces for £9,995 a pop without offering to pay investors £900 a year and more than £9,995 to take it back five years later, they would have.

The problem with buying a car parking space as an investment, unlike a leasehold flat, is that whoever owns the car park has no incentive to put cars in your space before they fill up their own.

This is a problem with all vertical landbanking investment schemes whether the asset is a car parking space, hotel room or care home suite. It is not a problem with investing in, say, a buy-to-let flat where the leaseholder remains responsible for finding somebody to pay them to live in it.

Invariably this problem is solved by the operator of the investment scheme offering to lease the asset back from the investor in return for a “guaranteed” “assured” or “fixed” yield. This works until the operator runs out of money to meet the guarantee and stops paying the investor.

The administrators are, thankfully, not going to be telling investors to buy car parking spaces for £9,995 in the expectation of 9% per year returns plus an uplifted buyback from an already bankrupt company.

Who they are going to find to buy the parking spaces without any guarantees attached remains to be seen.

But that is largely moot to investors in the car parking spaces that were sold, as no returns are anticipated for them from the administration.

Administrators to pay accountancy fees to the other Day

One company that is going to get a return from the administration is Younique Accountancy.

Younique Accountancy (no relation to the makeup multi-level marketing scheme) were Mederco’s previous accountants and have been retained by the administrators “due to their historical knowledge of the Company and the cost efficiency in retaining them to assist the Joint Administrators”.

Younique are to be paid on a time cost basis. Accountancy fees are estimated at £5,000 by the administrators.

Younique’s sole director and owner is Neil Day. Any relation to Stewart Day? Their exact relationship is not public, but what is public knowledge is that Neil Day was a former director of other Stewart Day companies including Swish Property Limited (dissolved in 2013) and Rainbow Homes Limited (Neil resigned in 2013), which suggests it’s more than a coincidence.

It’s a sad fact that often the only beneficiary of an administration is the administrators whose fees always stand first in the queue.

When one of the recipients of those fees is the (brother? cousin? namesake and longstanding former business partner?) of the guy who ran the collapsed investment scheme, it’s an extra kick in the teeth for investors.

Verto Homes is offering unregulated bonds paying 10% per year for a 5 year term.

The bonds offer the opportunity to exit after 12 months, however this will naturally depend on Verto Homes having enough cash available to pay back investors who wish to do so.

Funds raised are to be used to build zero carbon smart homes.

Who are Verto Homes?

Verto Homes founders Tom Carr and Richard Pearce

Verto Homes Limited was incorporated in December 2010.

Its last accounts show net assets of £2 million, and a profit in the year to March 2018 of £491k, up from a £762k loss in 2017.

Investors should however bear in mind that the accounts were unaudited.

Thanks to its history of selling shares in itself via CrowdCube, Verto has a long list of shareholders, but the people in charge are those with the A shares, co-founders Thomas Carr and Richard Pearce. The other shareholders have no voting rights.

Verto Homes has previously raised money on CrowdCube, with the most recent raise coming in October 2016, when it raised £1.39 million.

How safe is the investment?

Third-party promoters claim that Verto Homes bonds are a “low risk, secure, fixed return investment opportunity”.

The reality is that these are loans to a small unlisted company and carry an inherent risk of 100% loss. The claims by third parties that Verto Homes’ bonds are low risk and secure are highly misleading.

Secured lending on property is not risk-free as there is a risk that if the underlying borrower defaults, the security cannot be sold for enough to cover the loan.

Investors in asset-backed loans have been known to lose 100% of their money when it turned out that there were not enough assets left to pay investors after paying the insolvency administrator (who always stands first in the queue).

We are not in any sense implying that the same will happen to investors in Verto Homes, only illustrating the risk that is inherent in any loan note even when it is a secured loan.

If investors plan to rely on this security, it is essential that they hire professional due diligence specialists (working for themselves, not Verto Homes) to confirm that in the event of a default, the assets of Verto Homes would be valuable and liquid enough to compensate all investors. Investors should not simply rely on what Verto tells them about their assets.

Verto Homes Limited’s last accounts show that it owns no residential property as at March 2018. Its only tangible assets are £18k worth of machinery and £94k of motor vehicles. £6.1 million of its gross assets consisted of “investments” (mostly not elaborated on in the accounts, although there is a list of amounts loaned to various related companies, which tot up to £1.02 million net). Another £3.9 million consisted of trade and other debtors plus cash in the bank.

As it appears that Verto Homes’ houses and land under construction are owned by other related companies, it is even more essential that investors verify that the assets backing their loan to Verto Homes would be sufficient to enable them to be repaid in the event that Verto Homes defaulted.

How Verto’s third party introducers can claim with a straight face that 10% per year bonds from a company which until recently raised money via CrowdCube, a platform for high-risk startup investment, is “low risk”, is beyond me.

But Verto Homes has for whatever reason decided that the best way to access capital is now via the unregulated bond market and the people who sell them on its behalf, so here we are.

Should I invest in Verto Homes?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any individual loan note to an unlisted micro-cap company, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of up to 11.5% per year is inherently very high risk. As an individual, illiquid security with a risk of total and permanent loss, Verto Homes’ loan notes are much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if the investment defaulted and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for a “low risk” investment, you should not invest in corporate loans with a risk of 100% loss.

The administrators of collapsed unregulated property investment scheme Harewood Associates, Begbies Traynor, have released their first report.

Subsequent to the report, Harewood director Peter Kiely has signed a Statement of Affairs detailing how much of the company’s assets remain to be realised to investors.

An anonymised list of creditors shows that a total of £31.8 million was invested by 878 investors in its loan notes, an average of just over £36,000 per person. Amounts owed to creditors ranged from £5,000 to the largest investment of £788,481.

Currently unknown is the amount invested in shares issued by Harewood in Special Purpose Vehicles. At the moment administrators are deciding whether Harewood SPV investors should be considered creditors. Normally a shareholder of a company is not a creditor.

Back in 2016 Harewood claimed in a web promotion for their bonds:

If in the event that the Company did go into liquidation, the assets of the company would be sold off and the investors would be repaid. As we have substantial equity within each project, even at forced fire sale prices, there would be enough to repay the investors and deal with any staff, legal and accountancy commitments.

Turns out this was an aggressively overoptimistic statement.

According to the Statement of Affairs, Harewood loaned a total of £40.5 million to other related companies.

Of this, only £3.9 million is expected to be realised.

A £5,000 loan from a Paul Kiely, a £300,000 freehold property and £468 of cash in the bank brings the total estimated realisations to £4.2 million.

The administrators’ report lists a total of 9 related companies which owe money to Harewood. The administrators have written off 4 of these as not expected to provide any recovery. This includes the largest debts of £16.7 million owed to Harewood Venture Capital (which initially owned the liability of the investor creditors, but this was transferred to Harewood Associates in May 2018) and £19.2 million loaned to Sherwood Homes.

HVC is in liquidation (Begbies Traynor have taken over from the Official Receiver) while Sherwood Homes is still in existence, but has ceased to trade and holds no assets according to Peter Kiely.

As for the other five companies, the administrators are uncertain as to whether they will get anything from 3, and from the other 2 they anticipate getting something but cannot say how much.

The administrators have said that 84% losses before their costs is the current best case scenario. However this assumes that the five companies not already written off pay their debts back in full. Given the record of the other four, this would appear to be an optimistic assumption. In addition, the administrators’ fees (estimated at £276k as it stands) will come out before any payment is made to investors.

Equiscale

The administrators also refer to a company called Equiscale Limited which was acquired in March 2018 for £1.2 million. Equiscale owned a company called Geo. Noblett (Plant Hire), which in turn owned some land in Blackburn. The land was transferred to another Harewood company, Heron Homes, in April 2018 for £1.16 million. According to the administrators, Heron never paid Geo Noblett for the land.

Peter Kiely claims the shares in Equiscale were transferred to another company, Clifton Argyle Limited, in March 2018 and the proceeds deducted from money owed by Harewood to Clifton Argyle. The administrators say they “have not been provided with any evidence of this transaction and we are continuing with our investigations”.

So, in summary, Harewood used to own a company, but it doesn’t any more, and that company used to own some land, but it doesn’t any more, and it was never paid for that land, but as Harewood doesn’t own the company that wasn’t paid any more, that would seem to be moot from the investors’ perspective. In line with his statement to the administrators, Peter Kiely’s Statement of Affairs does not list the Equiscale investment.

How the bonds were sold

Harewood illegally promoted its loan notes and SPV shares directly to investors, claiming it was exempt from the Financial Services and Markets Act because it was a property company.

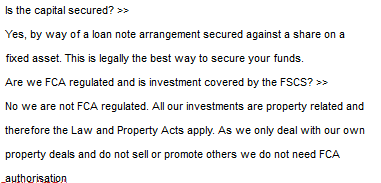

Are we FCA regulated and is investment covered by the FSCS?

No we are not FCA regulated. All our investments are property related and therefore the Law and Property Acts apply.

The reality is that loan notes and shares issued by a property company are subject to the FSMA just like any other loan note or equity security. Companies which promote securities to the public in the UK require authorisation from the FCA. Neither Harewood Associates nor its directors were authorised by the FCA.

Advert for Harewood’s bonds on their website, September 2016.

Kebab vans are a proven safe and secure investment because drunk people always want sheep testicles and if it goes tits up the Security Trustee will step in and sell the van. Invest now.

As pseudolegal gibberish goes, Harewood’s argument is a bit like me encouraging the public to invest in bonds paying 12% per year in my kebab van, and saying I’m exempt from the Financial Services and Markets Act because I’m a kebab van and therefore the Food Safety Act applies.

Not only were investors investing in loans not property; it turns out that they weren’t even investing in loans to a property company. They were investing in loans to a company which made loans to other companies.

Despite Harewood claiming on the 2016 version of its website

Investments are secured by way of debentures on UK residential developments

and

All our investments are property related

Extract from Harewood Associates website in 2016.

a significant proportion of the underlying loans in Harewood Associates were, according to the administrators’ report, not secured on property. The administrators have written off four out of nine companies which owe Harewood Associates money. Which means that either these loans from Harewood Associates aren’t secured on anything, or if they are, the security is worthless according to the administrators.

These four debts account for £36.6 million of the £40.5 million owed to Harewood Associates – just over 90%.

What if anything will be realised from the other 10% is currently highly uncertain.

The Morning Advertiser (a pub trade paper) reported back in 2006:

Paul Kiely’s brothers David and Shaun Kiely ran a firm, S-Mart Stores, that collapsed in identical fashion to Provence a year ago. Both firms sold hugely overvalued freehold properties to private investors on the promise of inflated rents.

[MP Jim] Dobbin tabled an Early Day Motion in the House of Commons in March 1998 which decried the activities of Provence founder Paul J Kiely and his brothers.

He described Kiely Developments as cowboy builders who “continually flouted builders regulations”. A year later the company, where Paul Kiely and brother Shaun Kiely served as directors, collapsed. This week Dobbin said: “I am not surprised to find that members of this family have been involved in a company which has again let down the people they claim to be working for. The Department of Trade needs to look seriously at their suitability for holding directorships. Maybe it is time for a fraud enquiry.”

As far as I can tell no fraud enquiry was ever launched, and you can’t blame one businessman for the failed businesses of their brother. There is therefore no suggestion that there was anything illegal about any of the Kielys’ businesses collapsing.

Nonetheless, it is difficult to see why any potential lender conducting basic corporate finance due diligence into Harewood Associates would not read about the collapse of David Kiely’s former business and the business history of the Kiely family as a whole, and ask serious questions about the history of the directors, and whether their investment opportunity was as secure as they claimed.

But it is easy to say such things with hindsight. Harewoods investors weren’t doing due diligence. They thought they were investing in property so none was needed.

The fundamental belief behind the Financial Services and Markets Act is that novice investors who do not know what due diligence is, are not skilled in carrying it out, and do not know when they should carry it out, should not have high risk unregulated securities promoted to them by unregulated companies.

But Harewoods believed that didn’t apply to them because something something property.

So here we are.

£32.8 million raised from investors on the basis of illegal and misleading financial promotions and nearly all of it has disappeared.

No action has been taken against Harewood or their directors by the FCA or any other government body that is currently in the public domain.

The accounts show that the company raised only £944,000 in its bonds as at March 2019, having said in its investment literature that it was targeting a raise of £10 million.

If the muted interest in its bonds disappointed the company, that hasn’t stopped it plowing ahead with its plans to generate returns by mining cryptocurrency.

According to a June 2019 press release, Solidus has been mining cryptocurrency (mostly Ethereum) in a temporary facility, having been unable to start construction of its planned Romanian data centre due to cold weather. The press release says construction has now started.

Adrian Stoica, CEO of Soft Galaxy

Solidus is operating in partnership with a Romanian firm, Soft Galaxy. Judging by its press release, Soft Galaxy CEO Adrian Stoica (also Head of Mining Operations at Solidus) is doing most of the talking for it.

According to the March 2019 accounts, Solidus owes £1.8 million to joint ventures in addition to the £944,000 plus interest owed to bondholders.

The company owns £2.8 million in assets of which £1 million is recorded as software licenses – “a unique application provided by our Joint Venturer – Soft Galaxy”.

Bearing in mind that Ethereum mining software can be downloaded for free, Soft Galaxy’s application must be pretty stellar to merit spending over a million – a third of Solidus Technology’s gross assets, and slightly more than it raised via its bonds – on licensing it.

Solidus’ other assets consisted of £1.4 million in tangible assets (mostly assets under construction and plant and machinery, presumably the Romanian data centre) and £380k in current assets. Net assets came out as a marginally negative £31k.

Solidus stated in its Information Memorandum that 25 – 30% of funds raised would be used to pay for the cost of fundraising.

Allansons LLP ran a litigation funding scheme offering returns of up to 50% over a 6-18 month term, which third-party introducers claimed was “low risk” and “100% secure”. By September 2018 investors were complaining about the lack of any returns, and in May 2019 the SRA shut Allansons down.

The fraudster, who uses the name “John / Jonathan Holt”, claims to represent the SRA and that investors will get their money back if they hand over 5% of the total invested. Naturally if they hand over their 5% they will never see it again. The individual may be using other aliases.

How “John Holt” obtained the contact details of Allansons investors is unknown.

Needless to say any approach from someone claiming that you can recover your investment X if you first pay them Y is fraudulent. If it was genuine they would just pay you X minus Y.

Reputable solicitors who actually would charge fees for taking action against a collapsed investment do not cold call, and do not claim to guarantee results.

Whisky Cask Company offers investment in casks of Scotch whisky.

Whisky Cask Company describes its role as “facilitating the sale”. The actual filling of the casks is done by the Malt Whisky Company.

Casks are matured for a minimum of three years, after which they can be sold on the market. Whisky Cask Company projects returns of 8 – 12% per year. It claims the investment is “A Sure-Fire Investment for The Future” and that investing in whisky “gives increased financial security — products cannot go bust in the way a company can”.

Who are Whisky Cask Company?

R: Whisky Cask Company founder Alexander Johnson. L: Head of Operations Ross Archer.

Whisky Cask Company was incorporated in June 2019 and due to its young age is yet to file accounts.

Founder and CEO Alexander Johnson owns 100% of Whisky Cask Company, according to its incorporation document.

Johnson’s bio states that he is “CEO and Chairman of Annandale Group, an investment company with interests in finance, real estate, media and food and beverages.”

Neither Annandale Group nor its interests seem to actually exist. Its website, annandale.group, gives its full name as “Annandale Investment Group Limited”. No company of that name exists on Companies House or anywhere else in the world according to Google and OpenCorporates. Annandale Group’s website provides no corporate registration number.

Viderium CEO Ross Archer has also joined Whisky Cask Company as Head of Operations. Both continue in their roles at Viderium.

How Viderium is doing financially is currently unknown, but the company is due to file its first accounts (to December 2018) within the next few weeks.

In an October 2018 press release, Viderium stated that it was considering listing on the stockmarket in 2019. Or to use their exact words, “Directors have hinted at a possible future IPO”. Press-release writing tip to Viderium CEO Ross Archer (who is the only Viderium director, and listed as the author of the press release): you can’t use the word “hint” while talking about yourself in the third person. Either you are planning an IPO or you aren’t. Anyway, with only five months of 2019 left, a 2019 IPO probably isn’t going to happen.

How safe is the investment?

Despite Whisky Cask Company’s claims that investing in whisky provides “increased financial security”, the reality is that investment in commodities (which includes whisky) is inherently high risk.

Whisky is a commodity and the price of all commodities fluctuates considerably.

The fact that whisky will mature as it ages is already known by both Whisky Cask Company and the Malt Whisky Company and is priced into the price they offer investors.

Unless investors are already professionally experienced whisky dealers, they should employ a professional whisky valuer working for and paid by them (not by Whisky Cask Company) to confirm that WWC’s whisky casks are as valuable as they say they are.

You would not buy a house as an investment and simply assume the seller’s estate agent’s valuation was accurate – you would hire your own valuer. The same applies here, unless you are willing to take a total gamble.

The worst case scenario is that investors hand money to Whisky Cask Company and they are unable to fulfil their contract to supply the whisky – which not a criticism of WCC, but an inherent risk when dealing with any small company. In this case investors would be looking at up to 100% loss.

Verifying that Whisky Cask Company are able to supply whisky as promised also requires professional due diligence into the firm. Note that speaking to Whisky Cask Company representatives or visiting their premises is not due diligence. Due diligence means independent verification of their claims.

Should I invest in Whisky Cask Company?

This blog does not give financial advice. The following are statements of publicly available facts or widely accepted investment principles, not a personalised recommendation. Investors should consult a regulated independent financial adviser if they are in any doubt.

As with any commodity investment, this investment is only suitable for sophisticated and/or high net worth investors who have a substantial existing portfolio and are prepared to risk 100% loss of their money.

Any investment offering returns of 8-12% per year is inherently high risk. As an investment in a commodity contract arranged by a newly formed company with a risk of total and permanent loss, Whisky Cask Company is much higher risk than a mainstream diversified stockmarket fund.

Before investing investors should ask themselves:

How would I feel if Whisky Cask Company defaulted on the contract and I lost 100% of my money?

Do I have a sufficiently large portfolio that the loss of 100% of my investment would not damage me financially?

If you are looking for an investment to provide “increased financial security”, you should not invest in a commodity supplied by a small company with a risk of 100% loss.